Over the past six months, Genesis Energy’s shares (currently trading at $14.60) have posted a disappointing 14% loss, well below the S&P 500’s 8.2% gain. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Genesis Energy, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Genesis Energy Will Underperform?

Even though the stock has become cheaper, we’re swiping left on Genesis Energy for now. Here are three reasons why there are better opportunities than GEL, plus one stock we’d rather own.

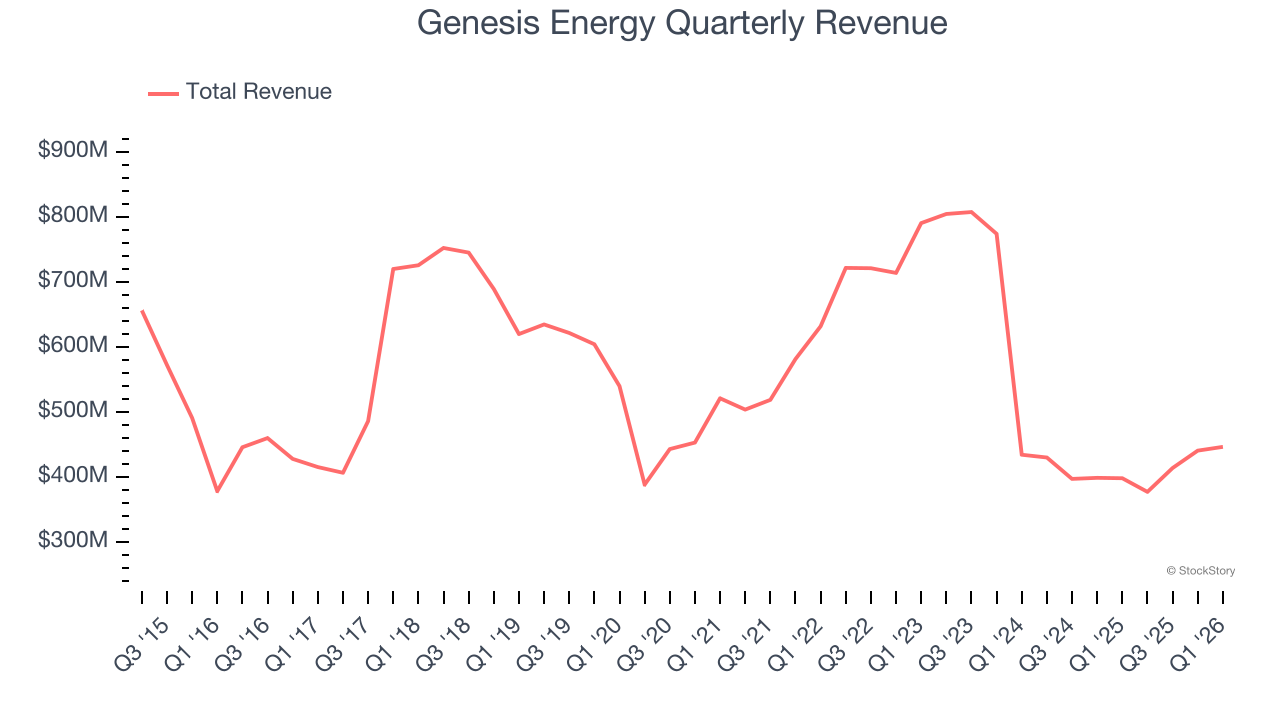

1. Revenue Spiraling Downwards

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Genesis Energy’s demand was weak over the last five years as its sales fell at a 1.5% annual rate. This wasn’t a great result and signals it’s a low quality business.

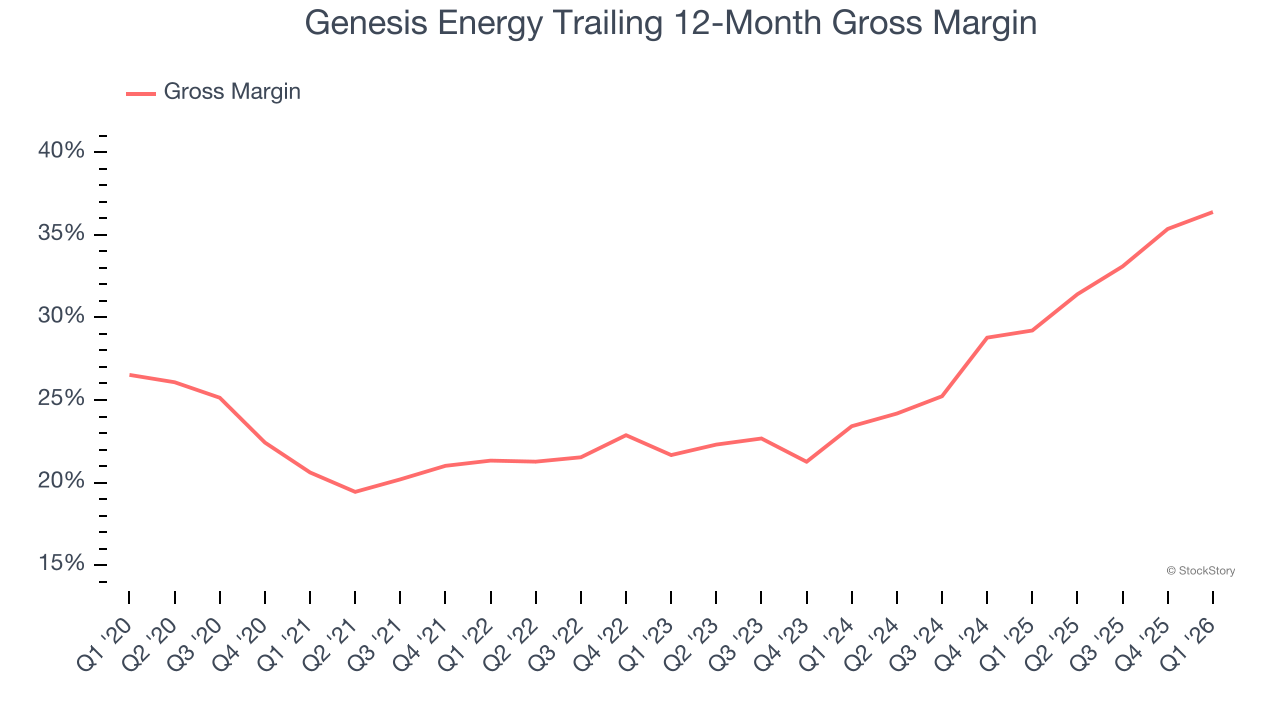

2. Low Gross Margin Reveals Weak Structural Profitability

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Genesis Energy, which averaged 25.3% gross margin over the last five years, exhibited bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

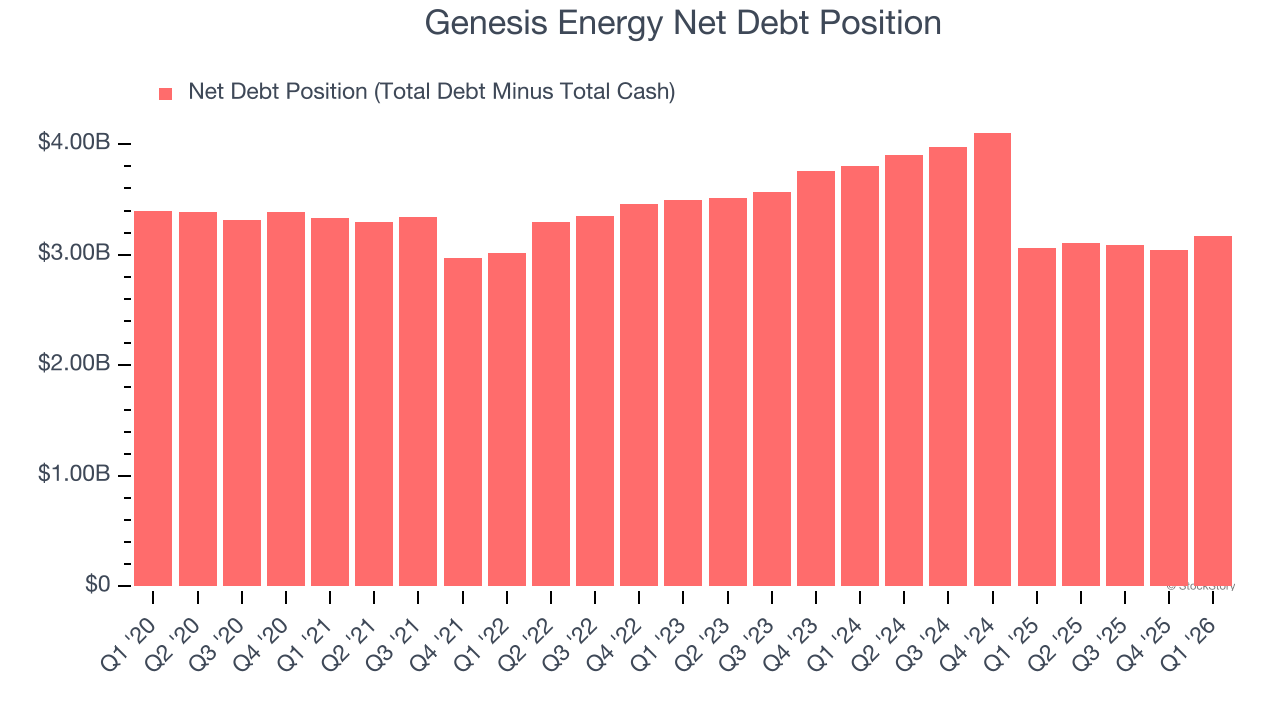

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Genesis Energy’s $3.18 billion of debt exceeds the $4.21 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $553.5 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Genesis Energy could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Genesis Energy can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

Genesis Energy doesn’t pass our quality test. Following the recent decline, the stock trades at 8.3× forward EV-to-EBITDA (or $14.60 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. We’d suggest looking at a dominant aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Genesis Energy

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,460% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+214% between June 2020 and June 2025). Find your next big winner with StockStory today.