Walker & Dunlop’s stock price has taken a beating over the past six months, shedding 20.3% of its value and falling to $50.23 per share. This might have investors contemplating their next move.

Is now the time to buy Walker & Dunlop, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Walker & Dunlop Will Underperform?

Even with the cheaper entry price, we’re swiping left on Walker & Dunlop for now. Here are three reasons we avoid WD, plus one stock we’d rather own.

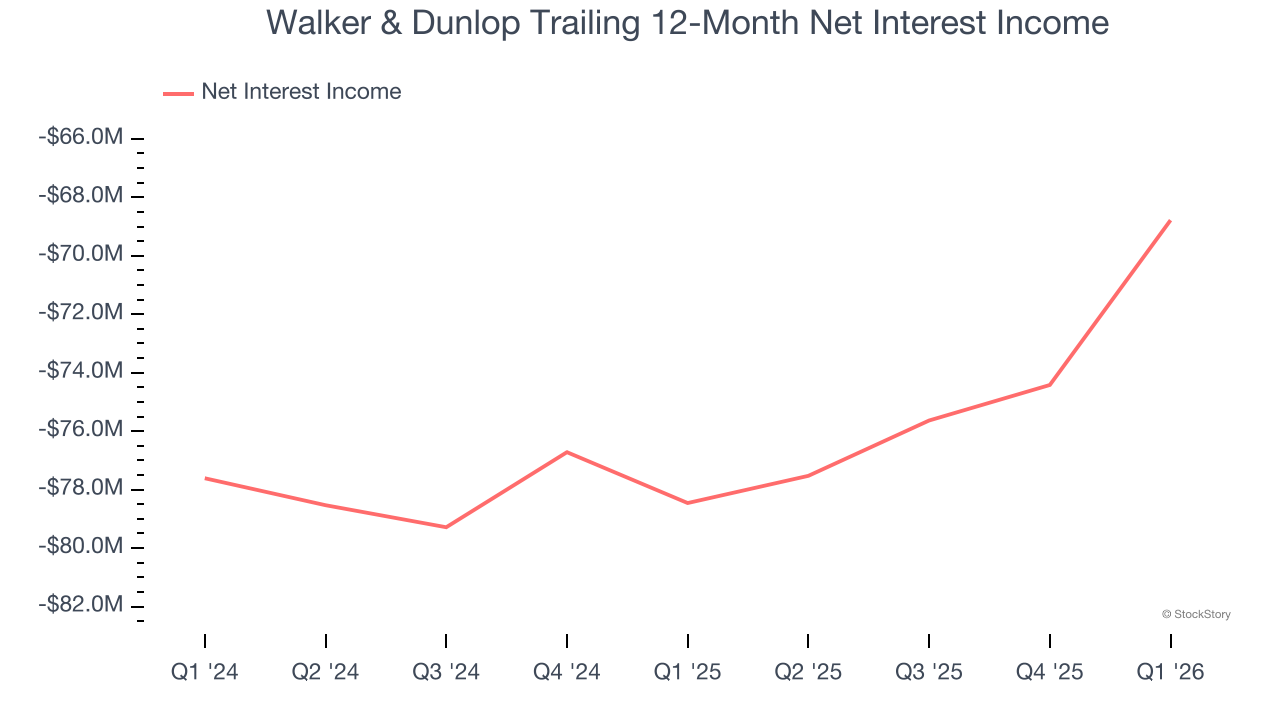

1. Declining Net Interest Income Reflects Weakness

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Walker & Dunlop’s net interest income has declined by 37.8% annually over the last five years, much worse than the broader banking industry. This shows that lending underperformed its other business lines.

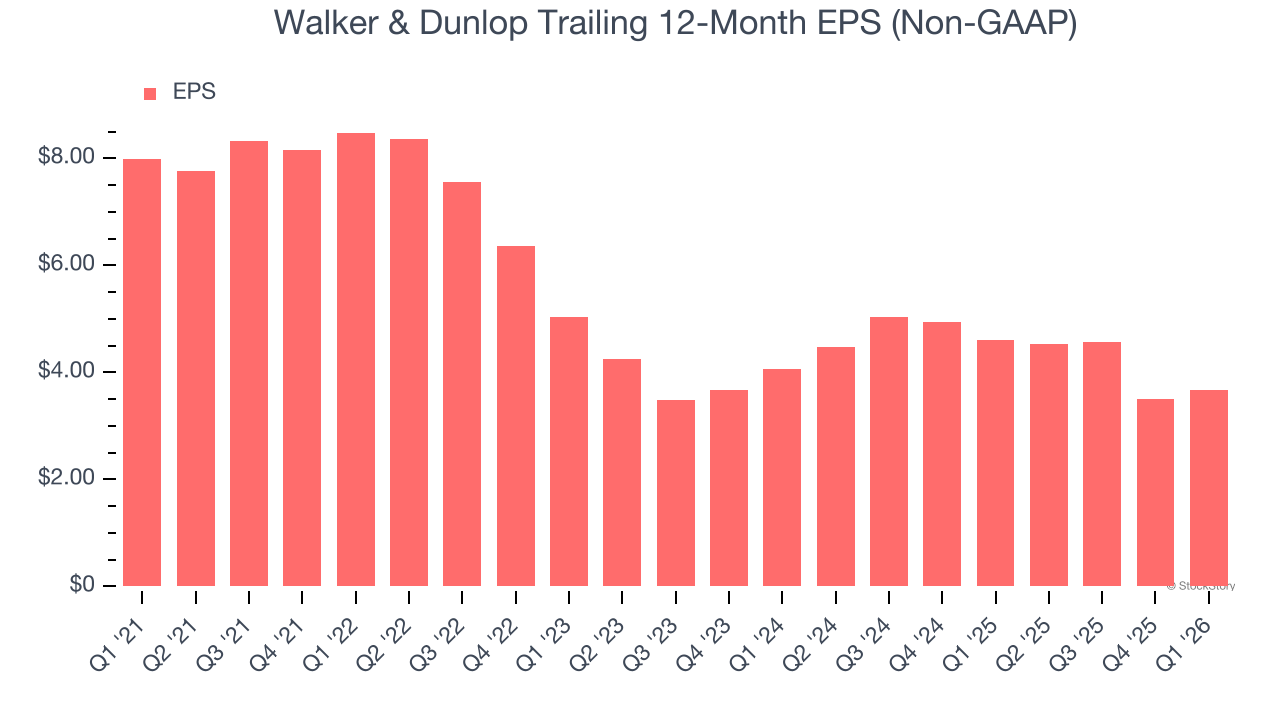

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Walker & Dunlop, its EPS declined by 14.4% annually over the last five years while its revenue grew by 3.9%. This tells us the company became less profitable on a per-share basis as it expanded.

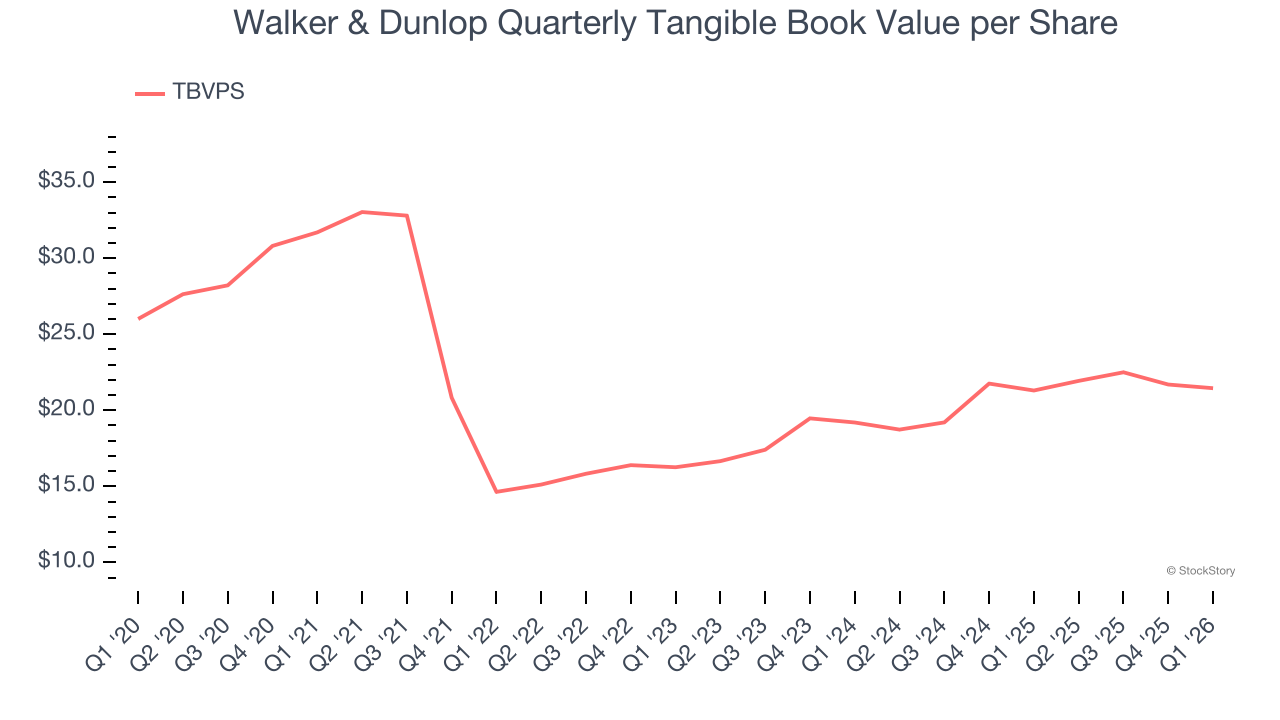

3. Substandard TBVPS Growth Indicates Limited Asset Expansion

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

To the detriment of investors, Walker & Dunlop’s TBVPS grew at a sluggish 5.7% annual clip over the last two years.

Final Judgment

Walker & Dunlop falls short of our quality standards. Following the recent decline, the stock trades at 0.9× forward P/B (or $50.23 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at a dominant aerospace business that has perfected its M&A strategy.

Stocks We Like More Than Walker & Dunlop

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren’t just high-quality businesses. Something is happening with them right now. Elite fundamentals meet near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week’s Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.