Darling Ingredients has been on fire lately. In the past six months alone, the company’s stock price has rocketed 46.4%, reaching $52.65 per share. This run-up might have investors contemplating their next move.

Is now the time to buy Darling Ingredients, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Darling Ingredients Not Exciting?

Despite the momentum, we’re sitting this one out for now. Here are three reasons why DAR doesn’t excite us, plus one stock we’d rather own.

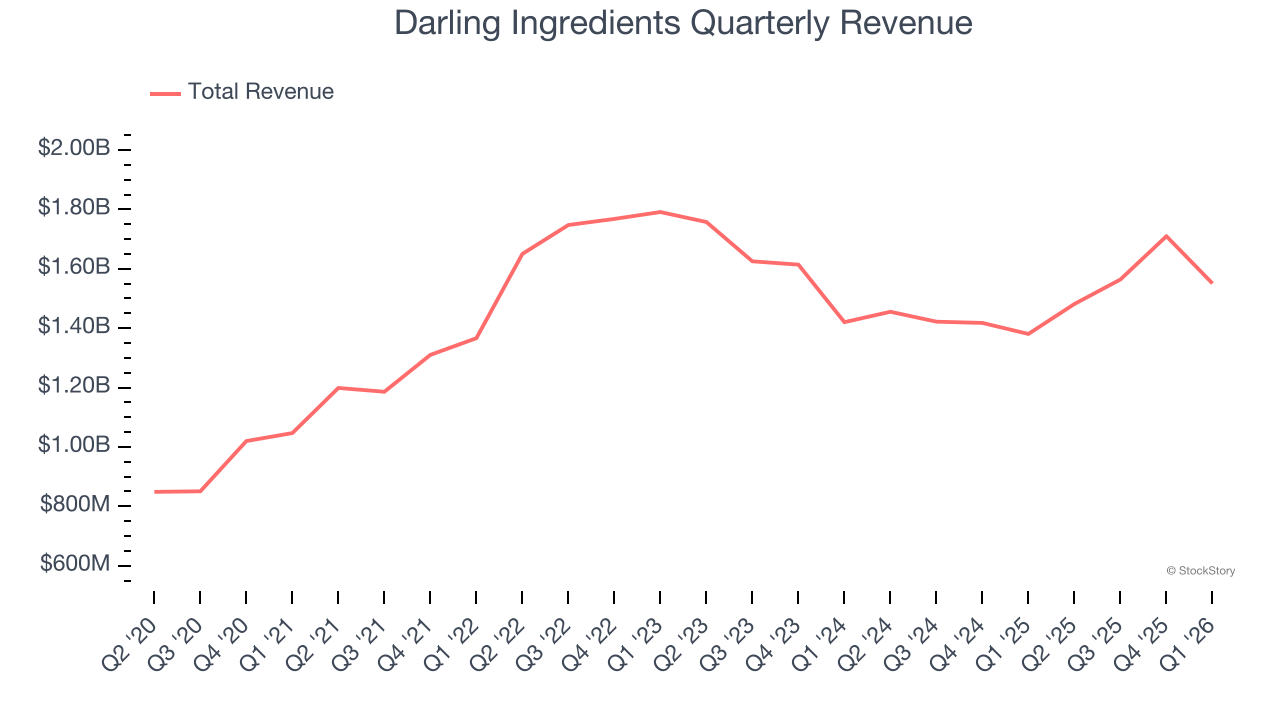

1. Revenue Spiraling Downwards

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Darling Ingredients’s demand was weak and its revenue declined by 3.2% per year. This was below our standards and signals it’s a lower quality business.

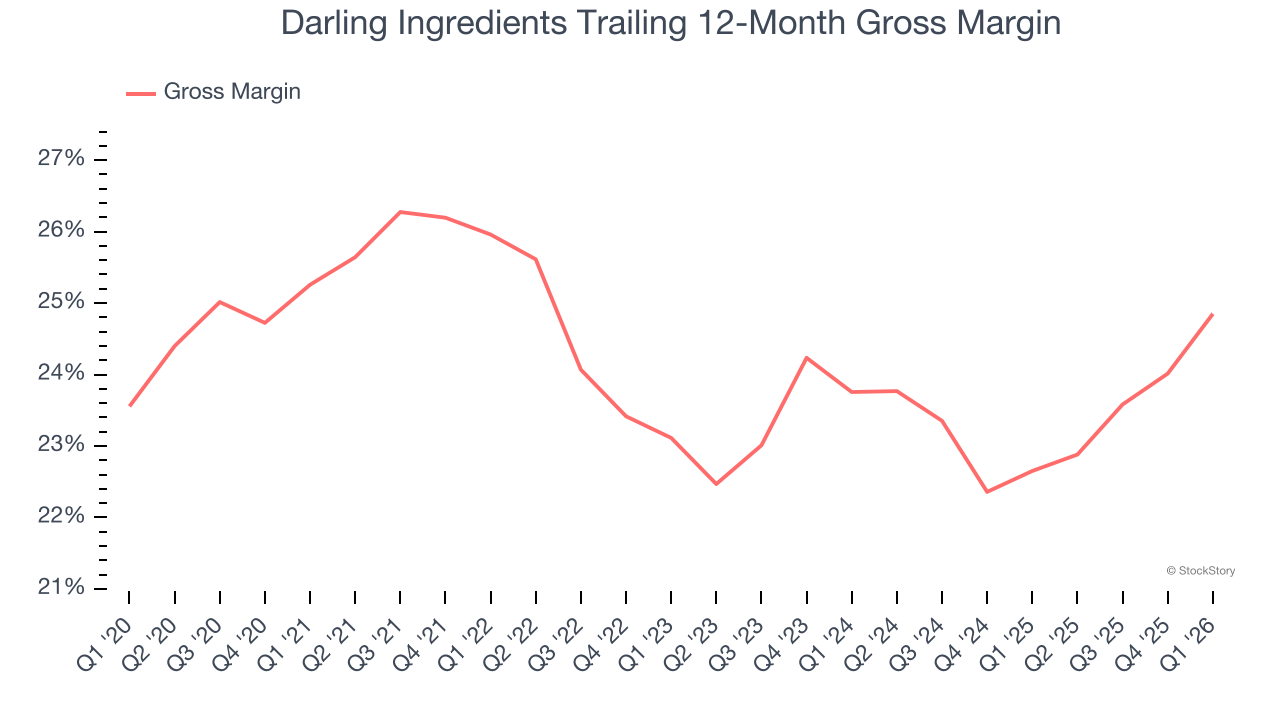

2. Low Gross Margin Reveals Weak Structural Profitability

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Darling Ingredients has bad unit economics for a consumer staples company, giving it less room to reinvest and develop new products. As you can see below, it averaged a 23.8% gross margin over the last two years. That means Darling Ingredients paid its suppliers a lot of money ($76.19 for every $100 in revenue) to run its business.

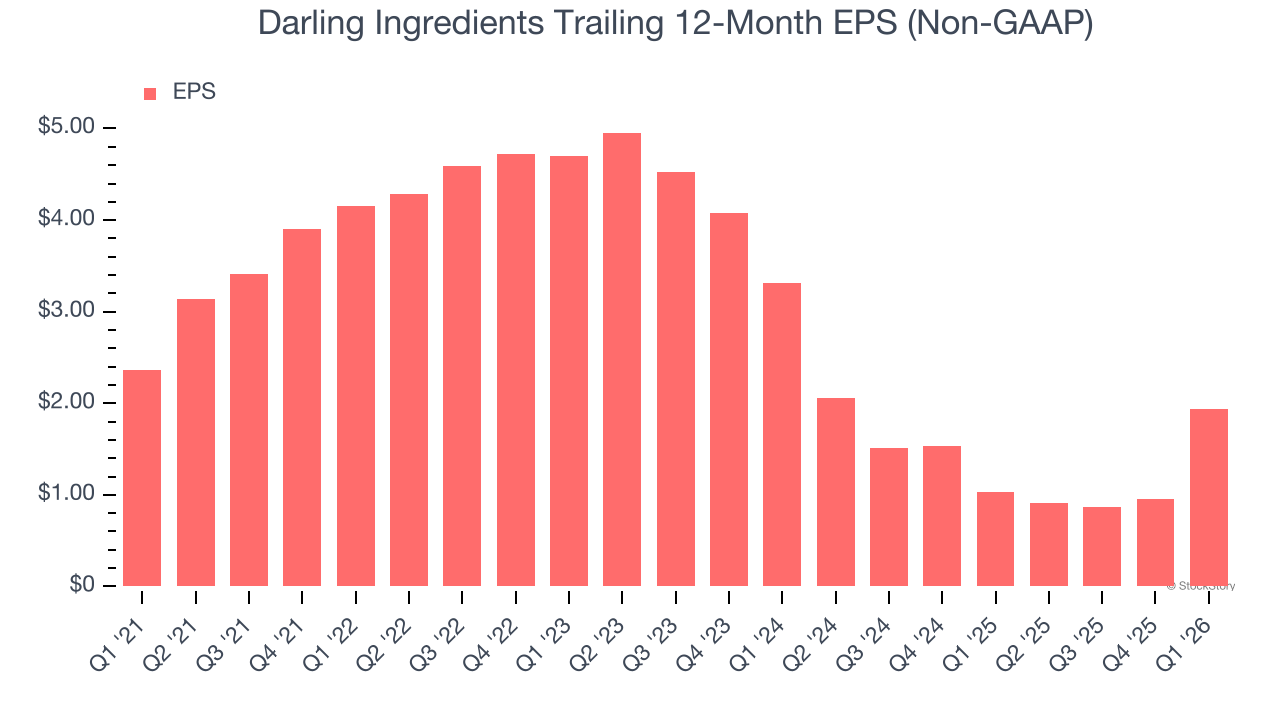

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Darling Ingredients, its EPS declined by 25.6% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Final Judgment

Darling Ingredients isn’t a terrible business, but it doesn’t pass our bar. After the recent surge, the stock trades at 10.3× forward P/E (or $52.65 per share). This valuation multiple is fair, but we don’t have much faith in the company. We’re fairly confident there are better stocks to buy right now. Let us point you toward the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of Darling Ingredients

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.