What a brutal six months it’s been for Sixth Street Specialty Lending. The stock has dropped 23.4% and now trades at a new 52-week low of $16.62, rattling many shareholders. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in Sixth Street Specialty Lending, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Do We Think Sixth Street Specialty Lending Will Underperform?

Even though the stock has become cheaper, we don’t have much confidence in Sixth Street Specialty Lending. Here are two reasons you should be careful with TSLX, plus one stock we’d rather own.

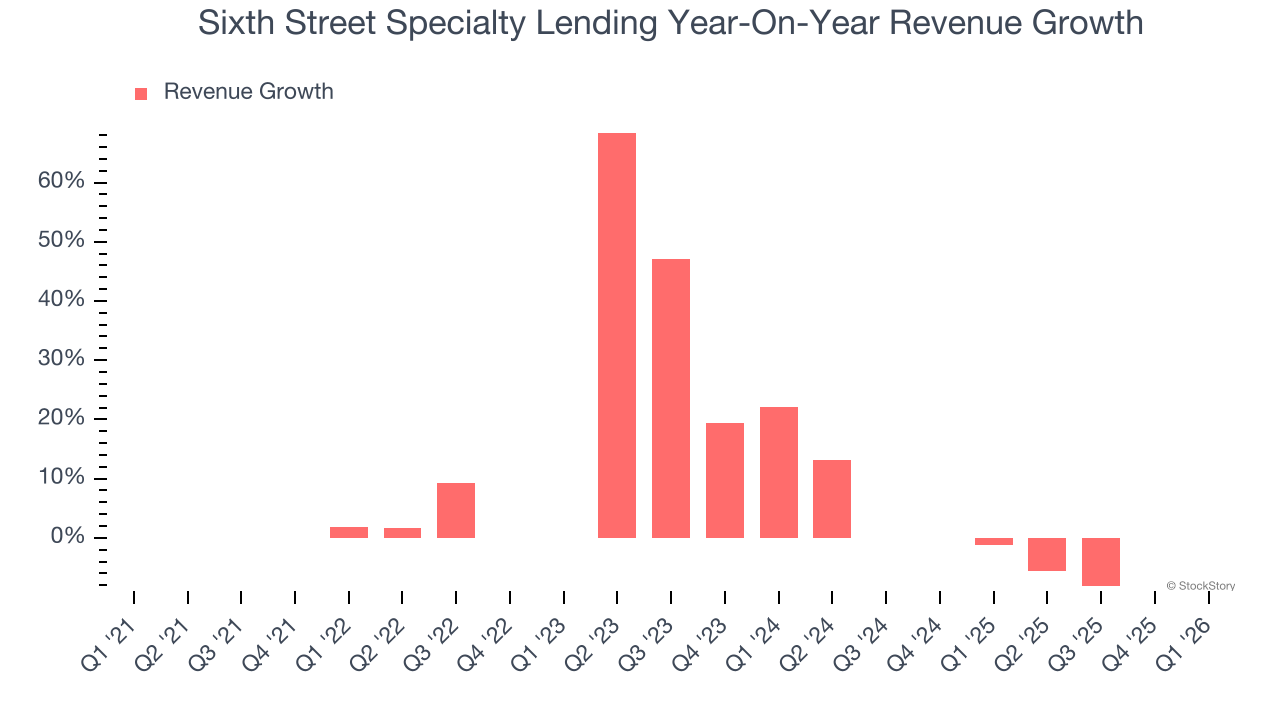

1. Revenue Tumbling Downwards

Long-term growth is the most important, but within financials, a stretched historical view may miss recent interest rate changes and market returns. Sixth Street Specialty Lending’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 3.7% over the last two years.  Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers because they were impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

2. EPS Growth Has Stalled

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sixth Street Specialty Lending’s flat EPS over the last five years was below its 9.6% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Sixth Street Specialty Lending falls short of our quality standards. Following the recent decline, the stock trades at 9.5× forward P/E (or $16.62 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now. Let us point you toward our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of Sixth Street Specialty Lending

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.