Boot Barn currently trades at $177.55 per share and has shown little upside over the past six months, posting a small loss of 4.5%. The stock also fell short of the S&P 500’s 6.3% gain during that period.

Is now the time to buy BOOT? Find out in our full research report, it’s free.

Why Does Boot Barn Spark Debate?

With a strong store presence in Texas, California, Florida, and Oklahoma, Boot Barn (NYSE: BOOT) is a western-inspired apparel and footwear retailer.

Two Positive Attributes:

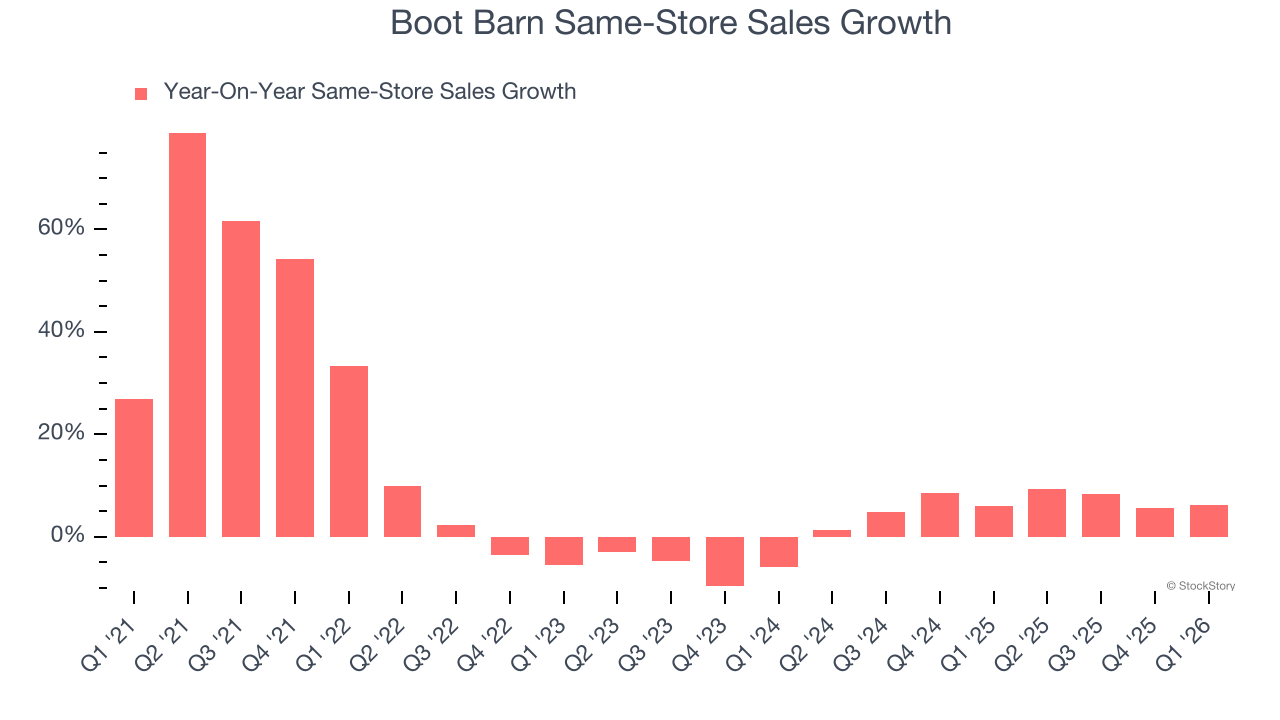

1. Surging Same-Store Sales Show Increasing Demand

Same-store sales is a key performance indicator used to measure organic growth at brick-and-mortar shops for at least a year.

Boot Barn has been one of the most successful retailers over the last two years thanks to skyrocketing demand within its existing locations. On average, the company has posted exceptional year-on-year same-store sales growth of 6.3%.

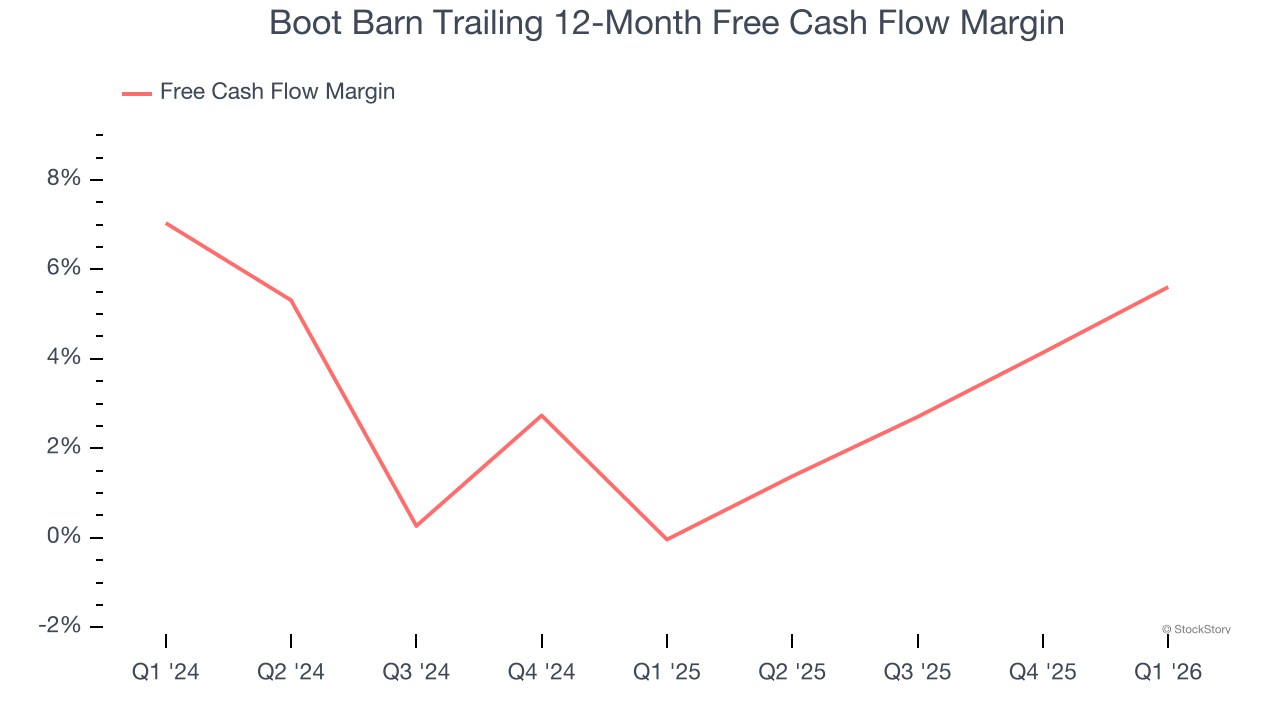

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn’t a prominently featured metric in company financials and earnings releases, but we think it’s telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Boot Barn’s margin expanded by 5.6 percentage points over the last year. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat. Boot Barn’s free cash flow margin for the trailing 12 months was 5.6%.

One Reason to Be Careful:

Fewer Distribution Channels Limit Its Ceiling

With $2.25 billion in revenue over the past 12 months, Boot Barn is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers. On the bright side, it can grow faster because it has more white space to build new stores.

Final Judgment

Boot Barn’s merits more than compensate for its flaws. With its shares underperforming the market lately, the stock trades at 20.3× forward P/E (or $177.55 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Boot Barn

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.