Agilysys has gotten torched over the last six months - since December 2025, its stock price has dropped 21% to $96.01 per share. This may have investors wondering how to approach the situation.

Is now the time to buy Agilysys, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Agilysys Not Exciting?

Despite the more favorable entry price, we’re swiping left on Agilysys for now. Here are two reasons you should be careful with AGYS, plus one stock we’d rather own.

1. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Agilysys, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

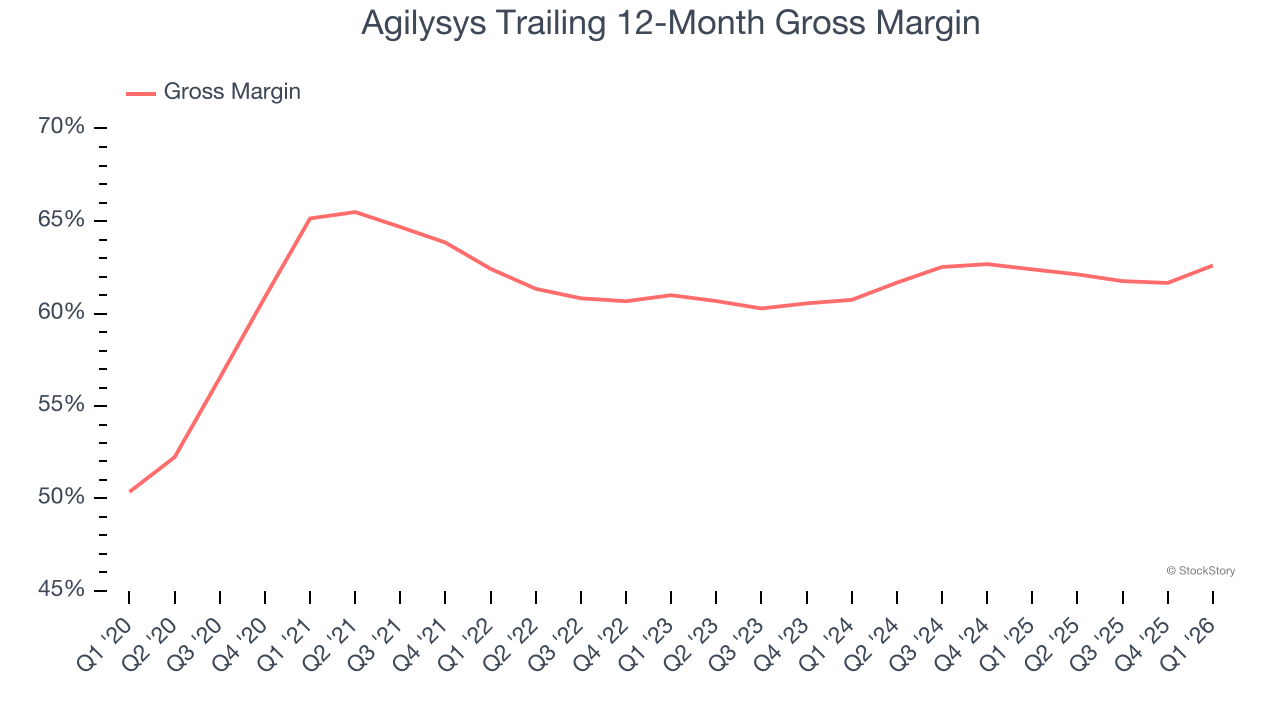

Agilysys’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 62.6% gross margin over the last year. That means Agilysys paid its providers a lot of money ($37.39 for every $100 in revenue) to run its business.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Agilysys has seen gross margins improve by 1.9 percentage points over the last 2 years, which is solid in the software space.

2. Operating Margin Rising, Profits Up

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses — everything from the cost of goods sold to sales and R&D.

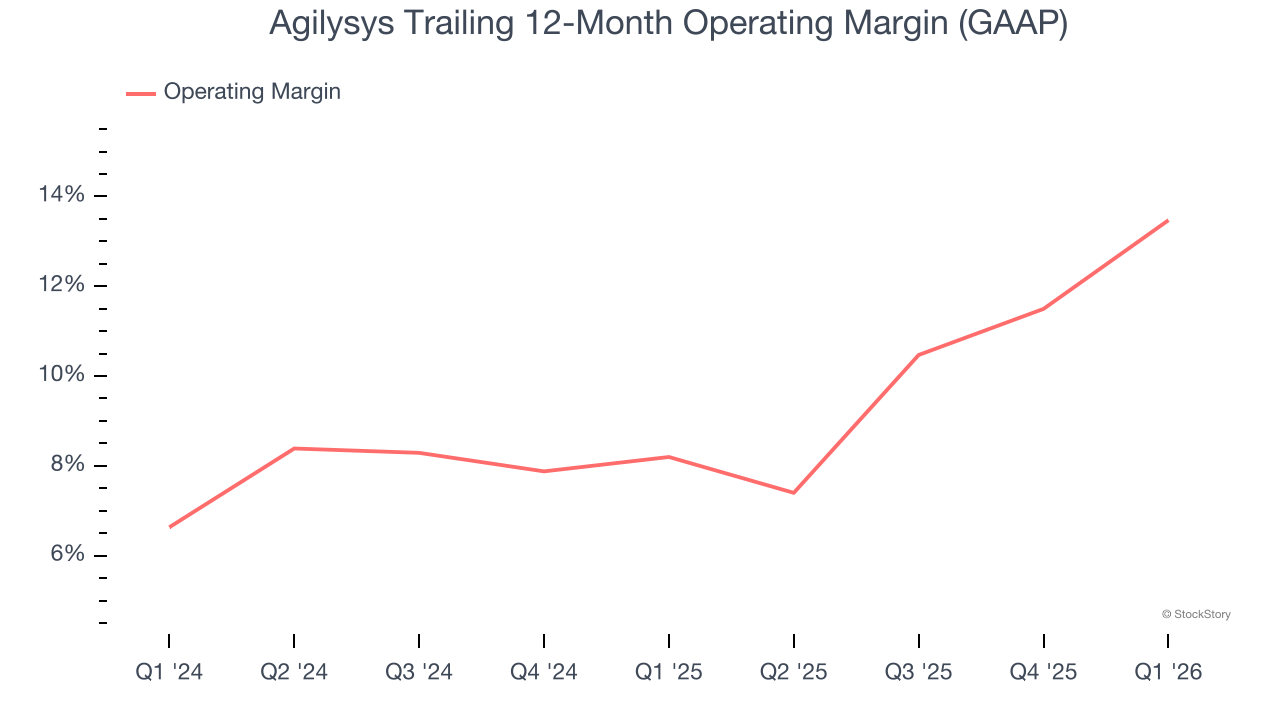

Looking at the trend in its profitability, Agilysys’s operating margin rose by 5.3 percentage points over the last two years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 13.5%.

Final Judgment

Agilysys isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 6.7× forward price-to-sales (or $96.01 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We’re pretty confident there are superior stocks to buy right now. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Agilysys

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.