Lululemon’s stock price has taken a beating over the past six months, shedding 50.4% of its value and falling to a new 52-week low of $105.41 per share. This was partly driven by its softer quarterly results and may have investors wondering how to approach the situation.

Following the pullback, is this a buying opportunity for LULU? Find out in our full research report, it’s free.

Why Is Lululemon a Good Business?

Originally serving yogis and hockey players, Lululemon (NASDAQ: LULU) is a designer, distributor, and retailer of athletic apparel for men and women.

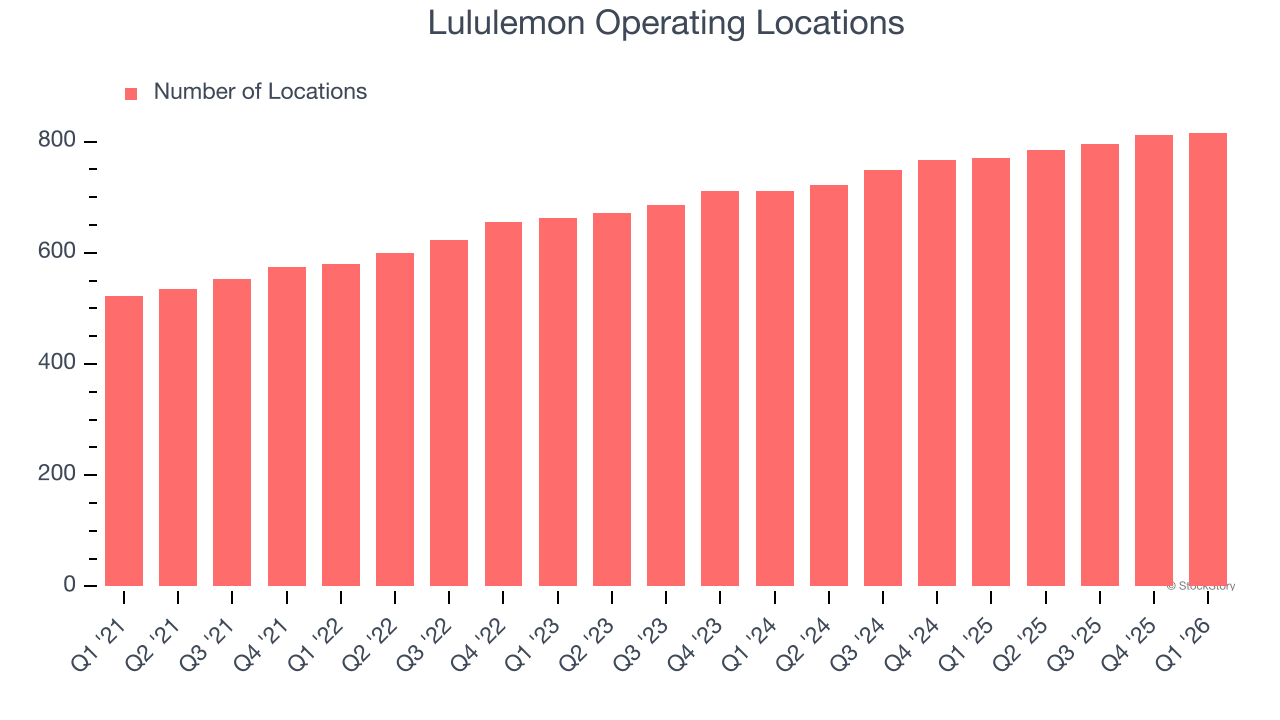

1. Store Growth Signals an Offensive Strategy

A retailer’s store count often determines how much revenue it can generate.

Lululemon operated 816 locations in the latest quarter. It has opened new stores at a rapid clip over the last two years, averaging 7.4% annual growth, much faster than the broader consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

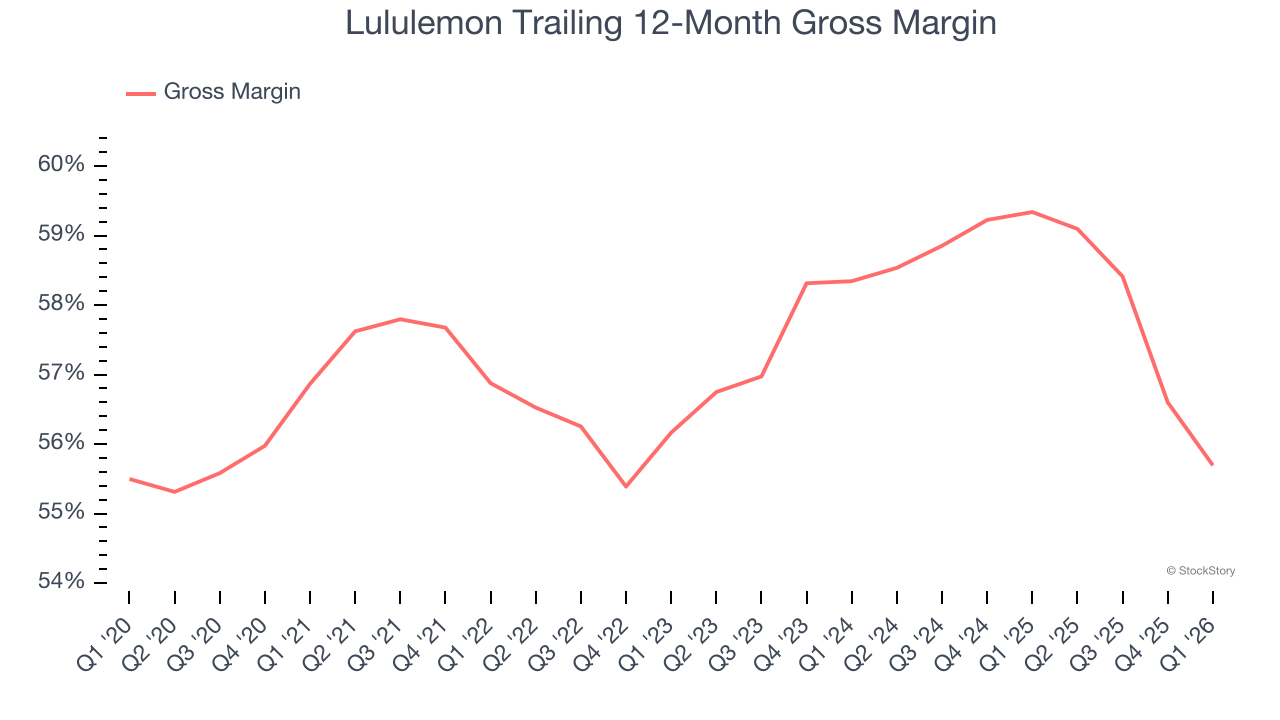

2. Elite Gross Margin Powers Best-In-Class Business Model

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

Lululemon has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent. As you can see below, it averaged an elite 57.5% gross margin over the last two years. That means Lululemon only paid its suppliers $42.52 for every $100 in revenue.

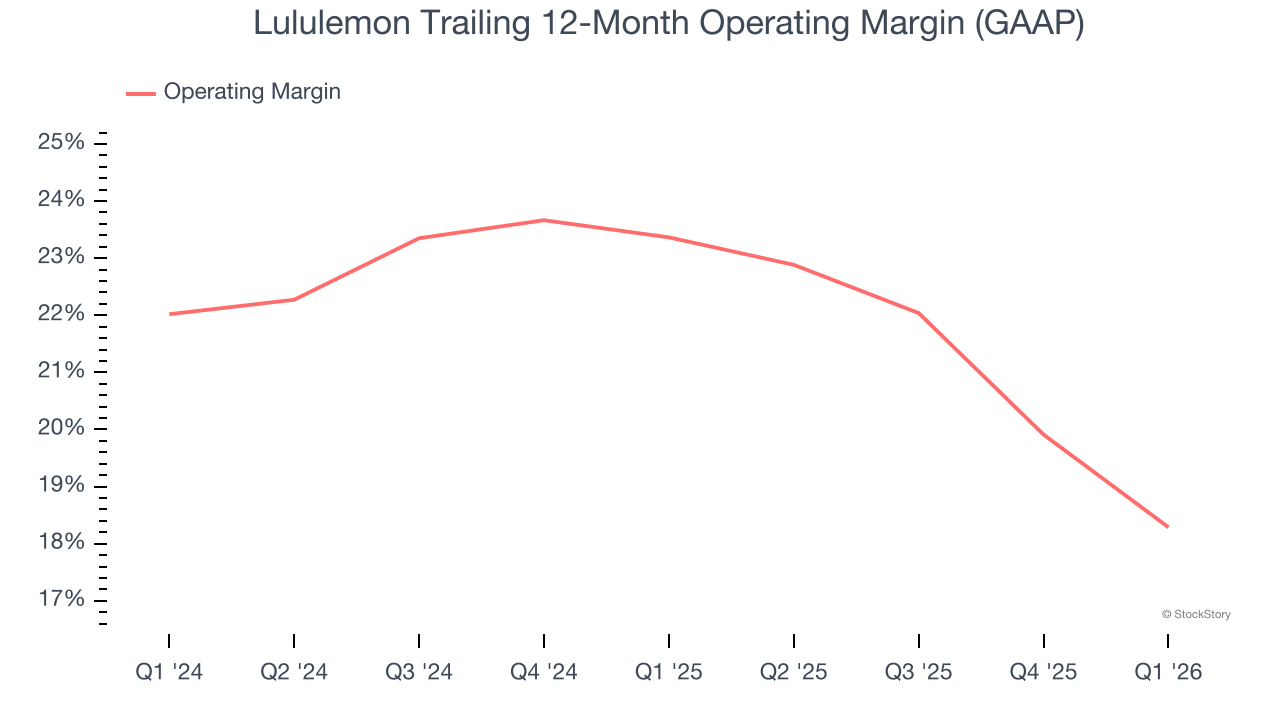

3. Operating Margin Reveals a Well-Run Organization

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses — everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Lululemon has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer retail business, boasting an average operating margin of 20.8%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Final Judgment

These are just a few reasons why we think Lululemon is a high-quality business. With the recent decline, the stock trades at 10× forward P/E (or $105.41 per share). Is now a good time to buy? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Lululemon

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don’t just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn’t over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.