Over the past six months, Core Natural Resources’s shares (currently trading at $81.75) have posted a disappointing 8.5% loss, well below the S&P 500’s 8.5% gain. This might have investors contemplating their next move.

Given the weaker price action, is now an opportune time to buy CNR? Find out in our full research report, it’s free.

Why Does Core Natural Resources Spark Debate?

Tracing its origins to 1864 and operating some mines southwest of Pittsburgh, Core Natural Resources (NYSE: CNR) mines and exports metallurgical coal used in steelmaking and thermal coal for power generation.

Two Positive Attributes:

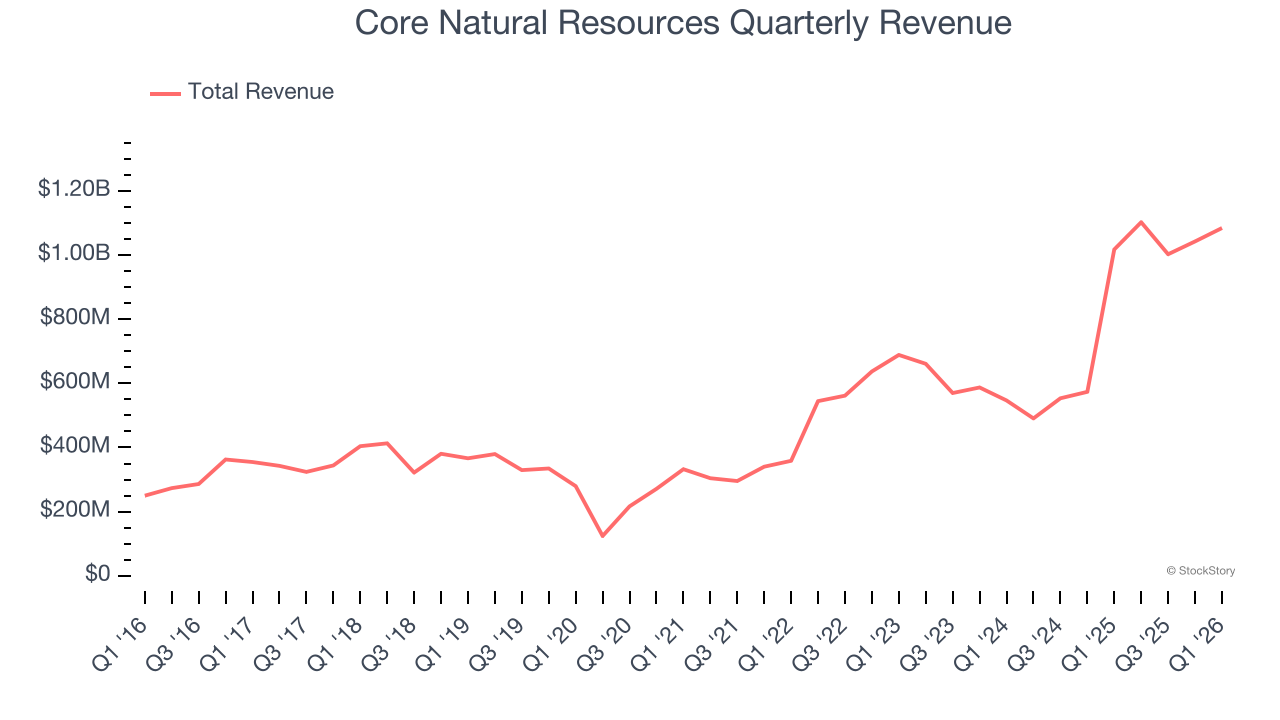

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical industries such as Energy can make mediocre companies look great for a time, but a long-term view reveals which businesses can actually withstand and adapt to changing conditions. Over the last five years, Core Natural Resources grew its sales at an incredible 35% compounded annual growth rate. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program.

Core Natural Resources’s $4.23 billion of revenue in the last year is mid-sized for the industry.

One Reason to Be Careful:

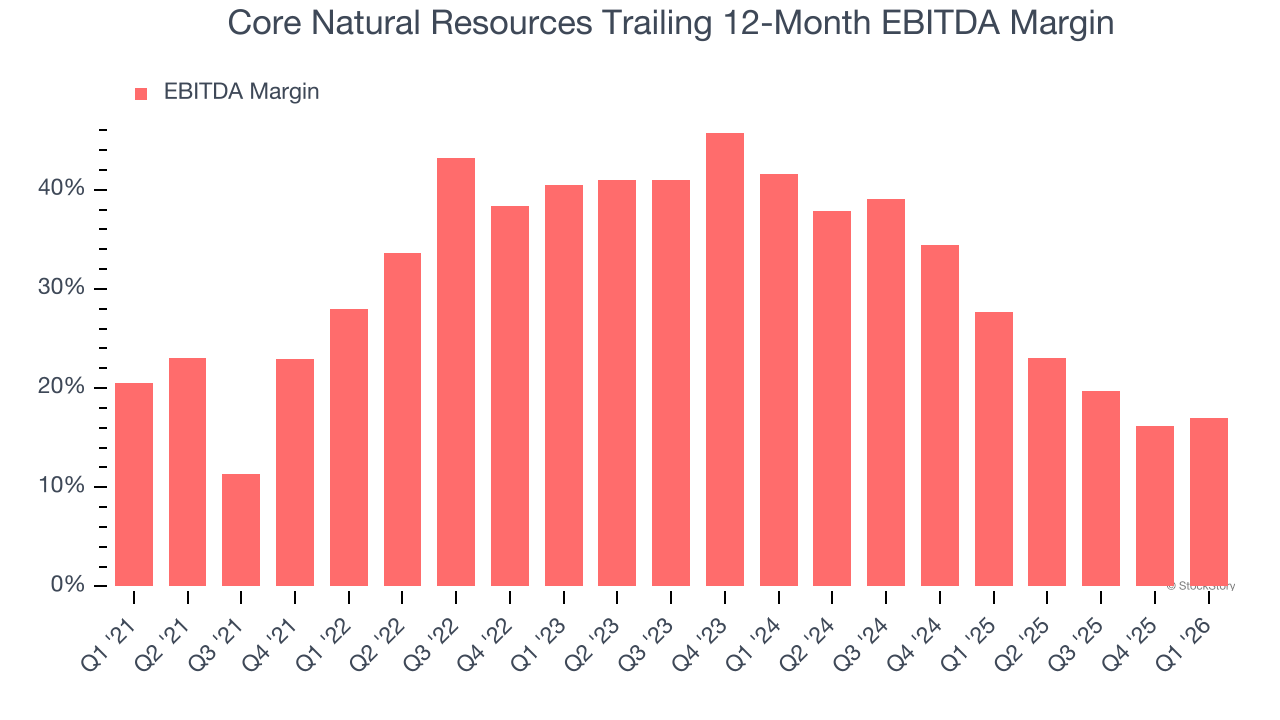

Shrinking EBITDA Margin

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

Analyzing the trend in its profitability, Core Natural Resources’s EBITDA margin decreased by 11 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Core Natural Resources’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its EBITDA margin for the trailing 12 months was 17%.

Final Judgment

Core Natural Resources’s merits more than compensate for its flaws. After the recent drawdown, the stock trades at 4.7× forward EV-to-EBITDA (or $81.75 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it’s flagging this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.