Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at Leslie's (NASDAQ: LESL) and its peers.

Consumer retail companies operate the brick-and-mortar stores where consumers have shopped for centuries. The way people shop is changing with increased penetration of technology, but these retailers are adapting and still very much a part of the consumer fabric.

The 53 consumer retail stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 0.8% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 9.8% on average since the latest earnings results.

Leslie's (NASDAQ: LESL)

Named after founder Philip Leslie, who established the company in 1963, Leslie’s (NASDAQ: LESL) is a retailer that sells pool and spa supplies, equipment, and maintenance services.

Leslie's reported revenues of $184.7 million, up 4.3% year on year. This print exceeded analysts’ expectations by 12.9%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ gross margin and EBITDA estimates.

“Our comprehensive transformation plan delivered measurable results in the second quarter as we position Leslie’s for sustainable profitable growth. Second quarter performance demonstrated the effectiveness of our strategic initiatives, with revenue growth of 4.3%, comparable sales increase of 6.6% and total customer count growth of 8% year-over-year. The early success of our ‘Price Drop’ initiative, launched in March, drove strong transaction growth and customer engagement in the quarter. Importantly, we have funded our price investments through controlled spending and successful cost optimization efforts supporting gross margin expansion in the quarter,” said Jason McDonell, Chief Executive Officer.

Leslie's scored the biggest analyst estimate beat of the whole group. Unsurprisingly, the stock is up 386% since reporting and currently trades at $6.95.

Is now the time to buy Leslie's? Access our full analysis of the earnings results here, it’s free.

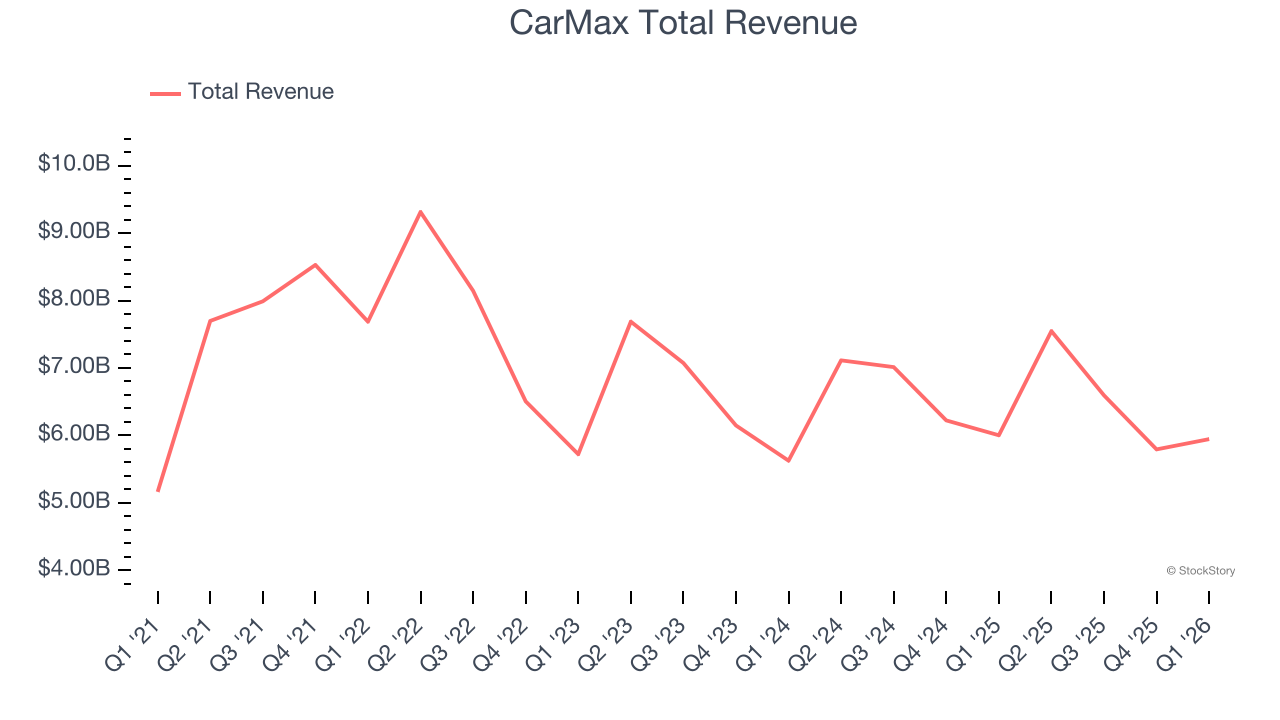

Best Q1: CarMax (NYSE: KMX)

Known for its transparent, customer-centric approach and wide selection of vehicles, Carmax (NYSE: KMX) is the largest automotive retailer in the United States.

CarMax reported revenues of $5.95 billion, flat year on year, outperforming analysts’ expectations by 3.9%. The business had a stunning quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems happy with the results as the stock is up 5.4% since reporting. It currently trades at $51.71.

Is now the time to buy CarMax? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Monro (NASDAQ: MNRO)

Started as a single location in Rochester, New York, Monro (NASDAQ: MNRO) provides common auto services such as brake repairs, tire replacements, and oil changes.

Monro reported revenues of $273.8 million, down 7.2% year on year, falling short of analysts’ expectations by 3.5%. It was a disappointing quarter as it posted a significant miss of analysts’ EBITDA and EPS estimates.

As expected, the stock is down 3.4% since the results and currently trades at $16.

Read our full analysis of Monro’s results here.

Tilly's (NYSE: TLYS)

With an emphasis on skate and surf culture, Tilly’s (NYSE: TLYS) is a specialty retailer that sells clothing, footwear, and accessories geared towards fashion-forward teens and young adults.

Tilly's reported revenues of $124.7 million, up 15.9% year on year. This print beat analysts’ expectations by 2.8%. Overall, it was an exceptional quarter as it also recorded EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ gross margin estimates.

The stock is up 4.6% since reporting and currently trades at $4.65.

Read our full, actionable report on Tilly's here, it’s free.

TJX (NYSE: TJX)

Initially based on a strategy of buying excess inventory from manufacturers or other retailers, TJX (NYSE: TJX) is an off-price retailer that sells brand-name apparel and other goods at prices much lower than department stores.

TJX reported revenues of $14.32 billion, up 9.2% year on year. This result topped analysts’ expectations by 2.4%. It was a very strong quarter as it also produced an impressive beat of analysts’ EBITDA and gross margin estimates.

The stock is up 10.5% since reporting and currently trades at $166.46.

Read our full, actionable report on TJX here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.