Webster Financial’s 26.8% return over the past six months has outpaced the S&P 500 by 19.2%, and its stock price has climbed to $72.68 per share. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Webster Financial, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Webster Financial Not Exciting?

Despite the momentum, we're cautious about Webster Financial. Here are three reasons we avoid WBS and a stock we'd rather own.

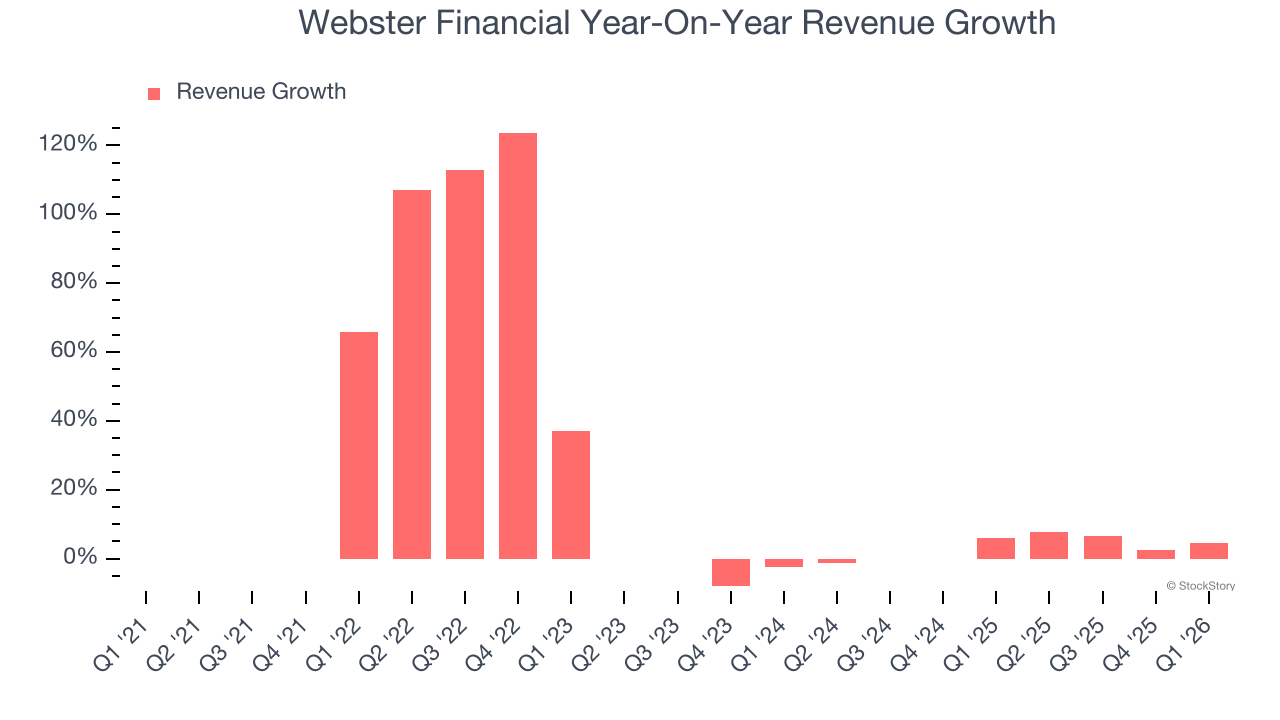

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Webster Financial’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.6% over the last two years was well below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

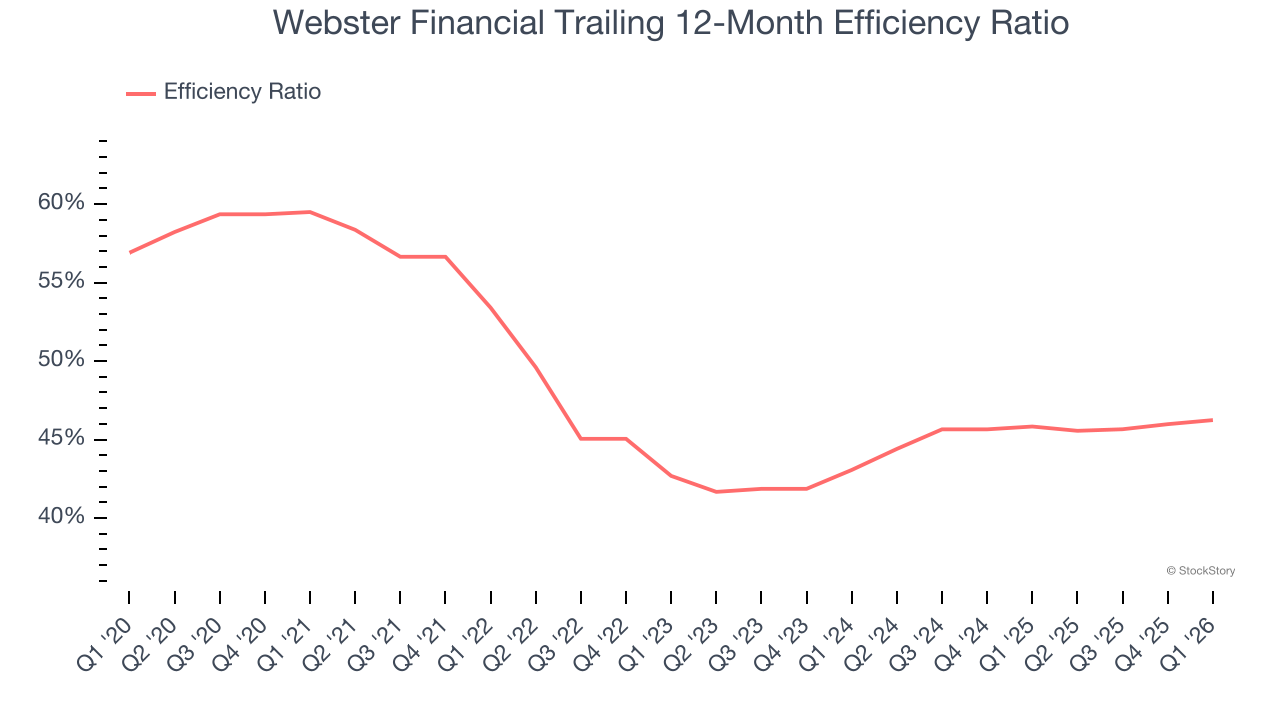

2. Efficiency Ratio Expected to Falter

Topline growth is certainly important, but the overall profitability of this growth matters for the bottom line. For banks, we look at efficiency ratio, which is non-interest expense (salaries, rent, IT, marketing, excluding interest paid out to depositors) as a percentage of total revenue.

Markets emphasize efficiency ratio trends over static measurements, recognizing that revenue compositions drive different expense bases. Lower efficiency ratios signal superior performance by indicating that banks are controlling costs effectively relative to their income.

For the next 12 months, Wall Street expects Webster Financial to become less profitable as it anticipates an efficiency ratio of 47.6% compared to 46.2% over the past year.

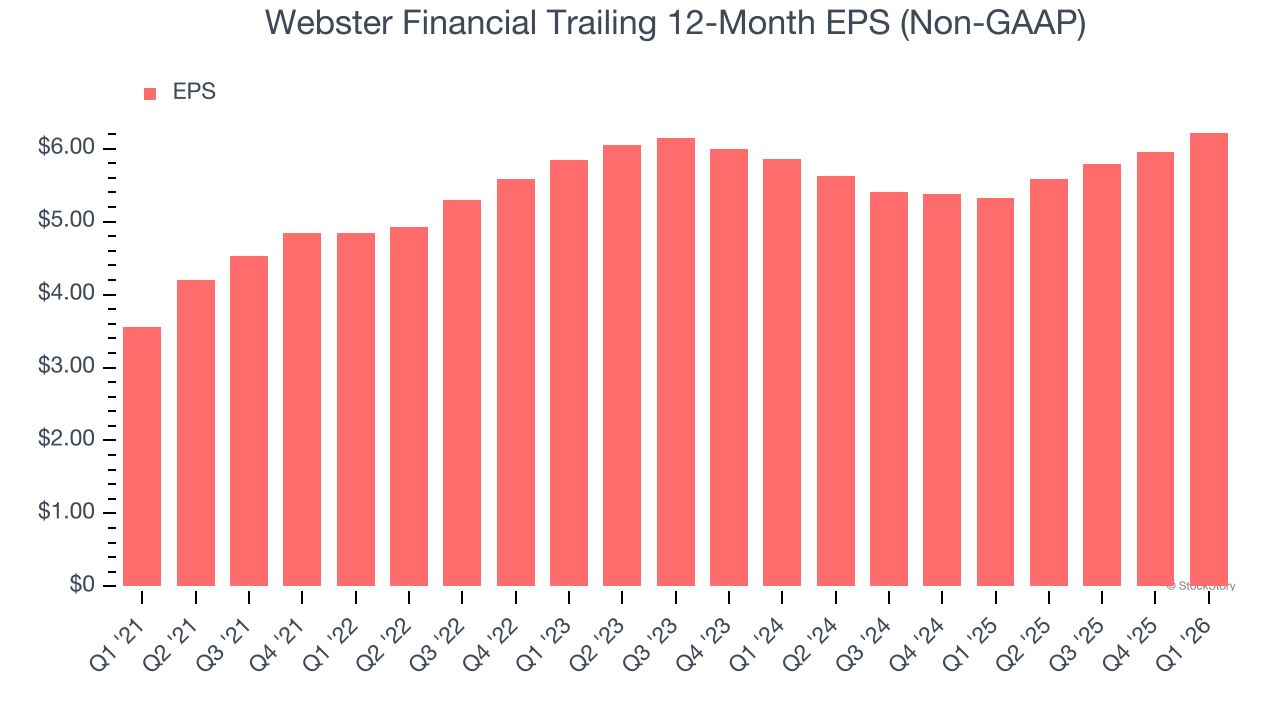

3. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Webster Financial’s weak 3% annual EPS growth over the last two years aligns with its revenue trend. On the bright side, this tells us its incremental sales were profitable.

Final Judgment

Webster Financial isn’t a terrible business, but it doesn’t pass our quality test. With its shares outperforming the market lately, the stock trades at 1.2× forward P/B (or $72.68 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere. We’d recommend looking at the most dominant software business in the world.

Stocks We Would Buy Instead of Webster Financial

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month - FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.