Personal wellness company WeightWatchers (NASDAQ: WW) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, but sales fell by 9.8% year on year to $168.3 million. On the other hand, the company’s full-year revenue guidance of $627.5 million at the midpoint came in 0.5% below analysts’ estimates. Its GAAP loss of $5.20 per share was 87.7% below analysts’ consensus estimates.

Is now the time to buy WeightWatchers? Find out by accessing our full research report, it’s free.

WeightWatchers (WW) Q1 CY2026 Highlights:

- Revenue: $168.3 million vs analyst estimates of $158.5 million (9.8% year-on-year decline, 6.1% beat)

- EPS (GAAP): -$5.20 vs analyst expectations of -$2.77 (87.7% miss)

- Adjusted EBITDA: -$1.84 million (-1.1% margin, 116% year-on-year decline)

- The company reconfirmed its revenue guidance for the full year of $627.5 million at the midpoint

- EBITDA guidance for the full year is $110 million at the midpoint, above analyst estimates of $107.3 million

- Operating Margin: -18.1%, down from 5.2% in the same quarter last year

- Free Cash Flow was -$39.34 million, down from $14.99 million in the same quarter last year

- Market Capitalization: $118 million

Company Overview

Known by many for its old cable television commercials, WeightWatchers (NASDAQ: WW) is a wellness company offering a range of products and services promoting weight loss and healthy habits.

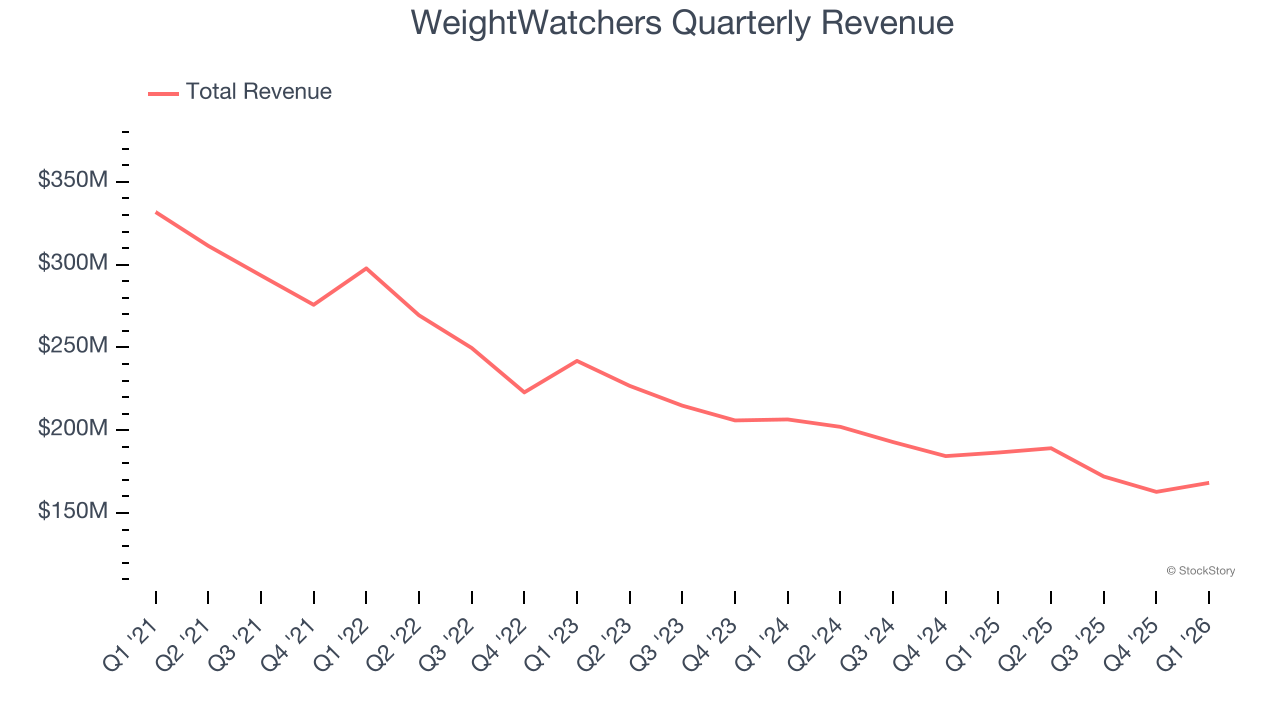

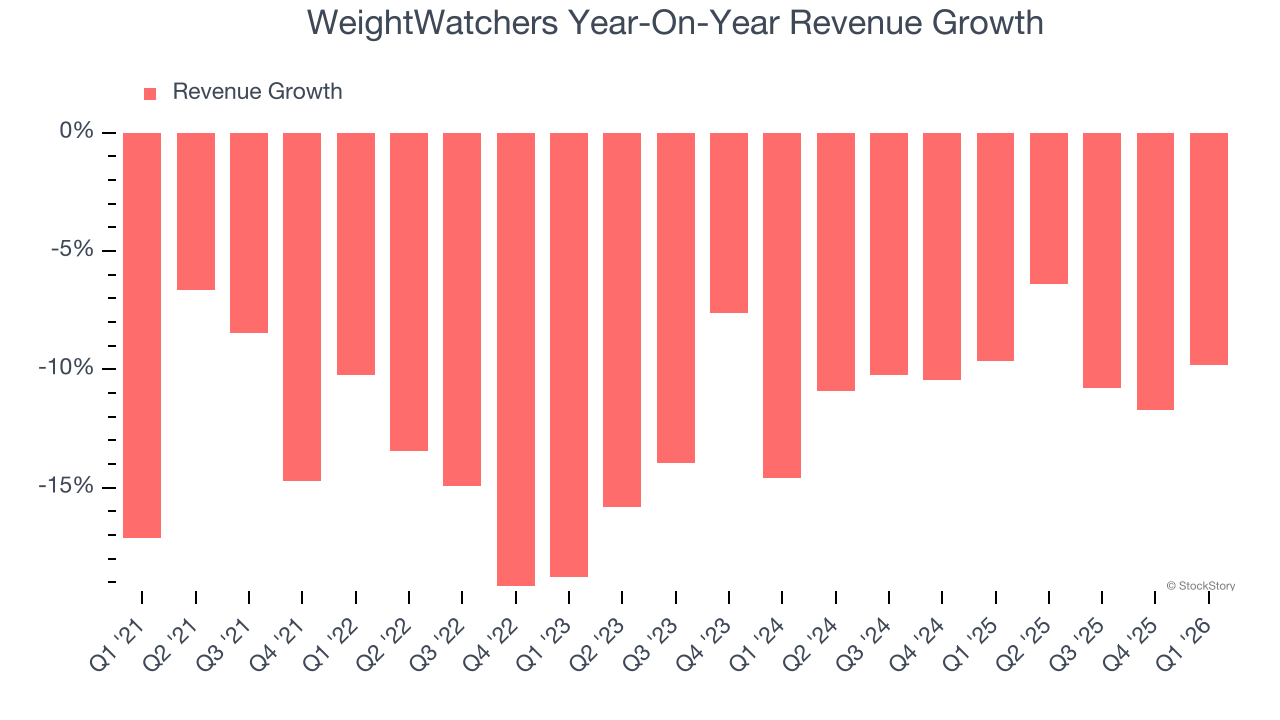

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, WeightWatchers’s demand was weak and its revenue declined by 12% per year. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. WeightWatchers’s annualized revenue declines of 10% over the last two years suggest its demand continued shrinking.

This quarter, WeightWatchers’s revenue fell by 9.8% year on year to $168.3 million but beat Wall Street’s estimates by 6.1%.

Looking ahead, sell-side analysts expect revenue to decline by 10.6% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not lead to better top-line performance yet.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

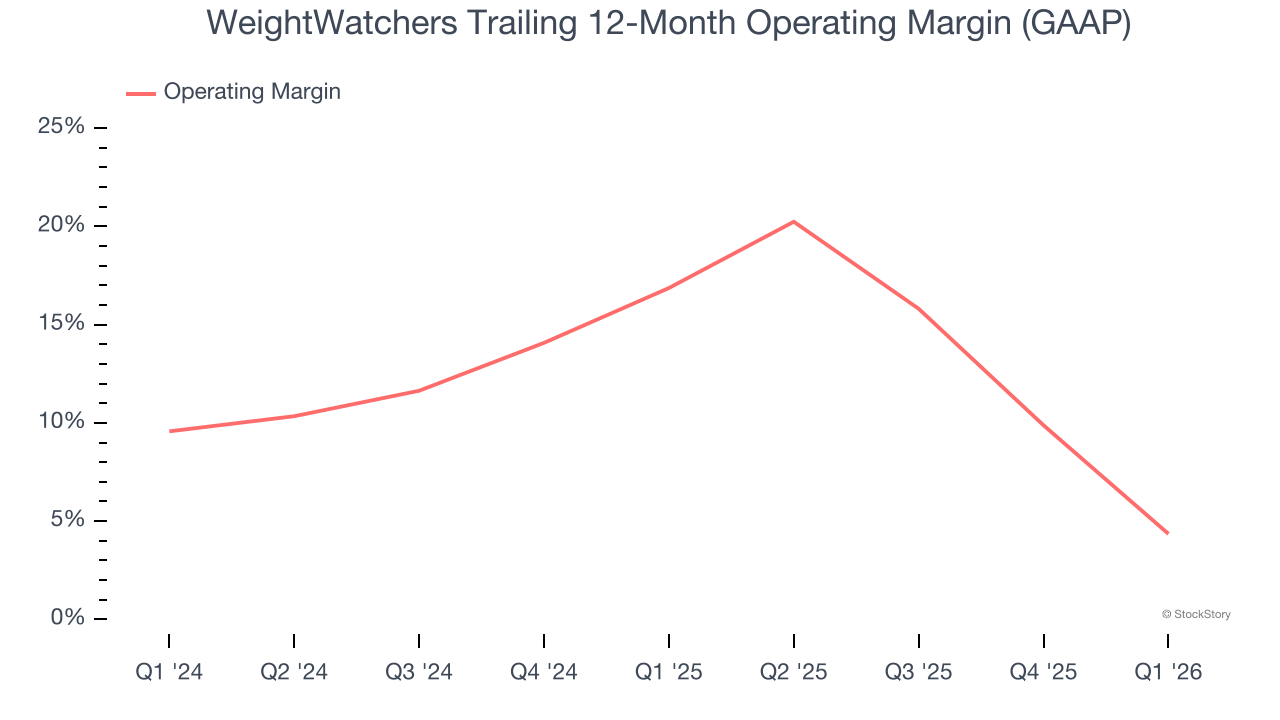

Operating Margin

WeightWatchers’s operating margin has shrunk over the last 12 months and averaged 10.9% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, WeightWatchers generated an operating margin profit margin of negative 18.1%, down 23.3 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

Cash Is King

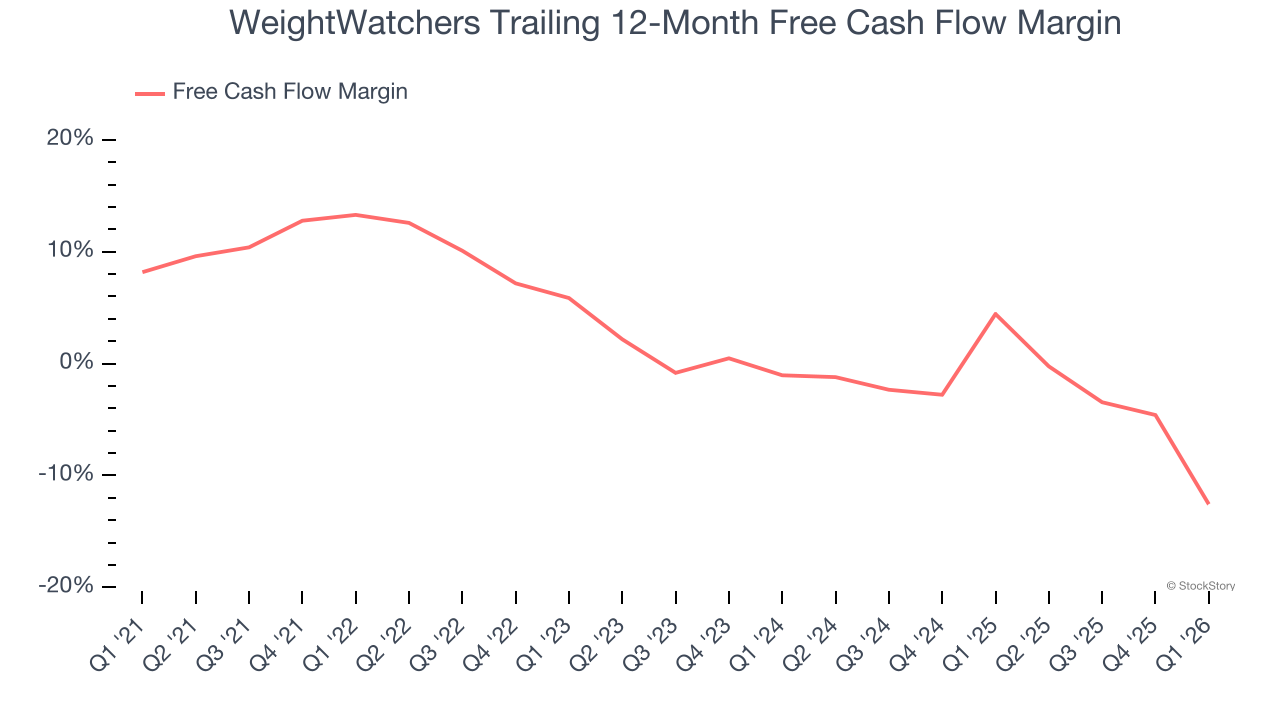

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the last two years, WeightWatchers’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 3.6%, meaning it lit $3.64 of cash on fire for every $100 in revenue.

WeightWatchers burned through $39.34 million of cash in Q1, equivalent to a negative 23.4% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Key Takeaways from WeightWatchers’s Q1 Results

We enjoyed seeing WeightWatchers beat analysts’ revenue expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter was mixed. The stock remained flat at $11.80 immediately following the results.

So should you invest in WeightWatchers right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).