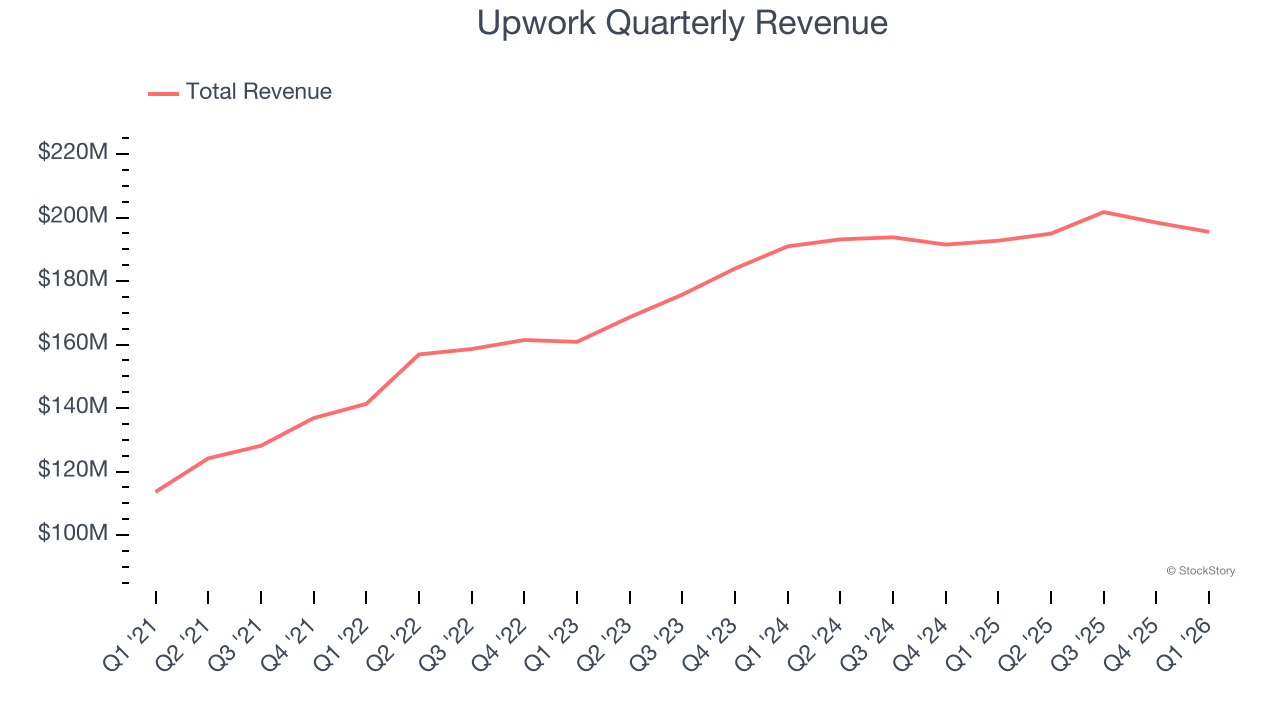

Online work marketplace Upwork (NASDAQ: UPWK) met Wall Street’s revenue expectations in Q1 CY2026, with sales up 1.4% year on year to $195.5 million. On the other hand, next quarter’s revenue guidance of $190 million was less impressive, coming in 6.9% below analysts’ estimates. Its non-GAAP profit of $0.35 per share was 29% above analysts’ consensus estimates.

Is now the time to buy Upwork? Find out by accessing our full research report, it’s free.

Upwork (UPWK) Q1 CY2026 Highlights:

- Revenue: $195.5 million vs analyst estimates of $195.9 million (1.4% year-on-year growth, in line)

- Adjusted EPS: $0.35 vs analyst estimates of $0.27 (29% beat)

- Adjusted EBITDA: $57.43 million vs analyst estimates of $46.39 million (29.4% margin, 23.8% beat)

- The company dropped its revenue guidance for the full year to $775 million at the midpoint from $842.5 million, a 8% decrease

- Management raised its full-year Adjusted EPS guidance to $1.53 at the midpoint, a 4.8% increase

- EBITDA guidance for the full year is $255 million at the midpoint, above analyst estimates of $241.6 million

- Operating Margin: 16.7%, down from 20.1% in the same quarter last year

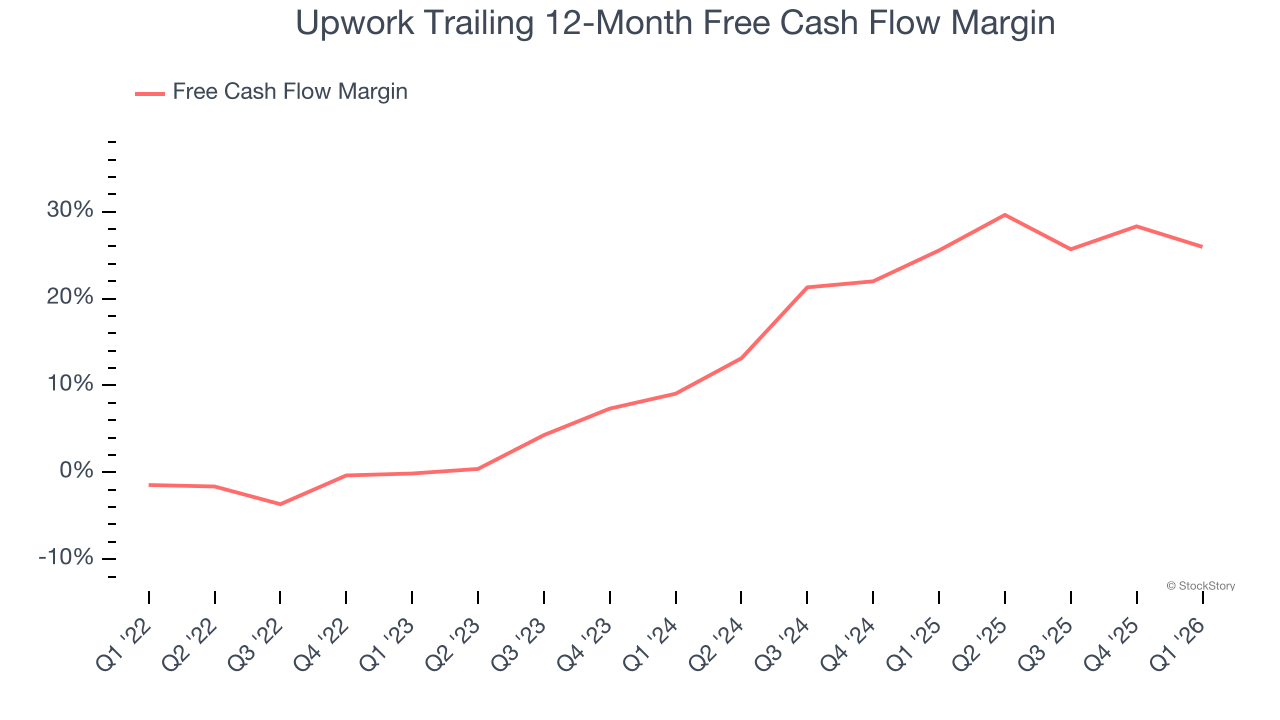

- Free Cash Flow Margin: 6.6%, down from 28.9% in the previous quarter

- Market Capitalization: $1.24 billion

"This was a dynamic first quarter, where we delivered strong profitability while navigating a challenging demand environment," said Hayden Brown, president and CEO of Upwork Inc.

Company Overview

Formed through the 2013 merger of Elance and oDesk, Upwork (NASDAQ: UPWK) is an online platform where businesses and independent professionals connect to get work done.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Upwork grew its sales at a tepid 7.4% compounded annual growth rate. This wasn’t a great result compared to the rest of the consumer internet sector, but there are still things to like about Upwork.

This quarter, Upwork grew its revenue by 1.4% year on year, and its $195.5 million of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 2.5% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.4% over the next 12 months, an acceleration versus the last three years. This projection is above the sector average and implies its newer products and services will fuel better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Upwork has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging 25.8% over the last two years.

Taking a step back, we can see that Upwork’s margin expanded by 26.1 percentage points over the last few years. This is encouraging because it gives the company more optionality.

Upwork’s free cash flow clocked in at $12.91 million in Q1, equivalent to a 6.6% margin. The company’s cash profitability regressed as it was 9.4 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

Key Takeaways from Upwork’s Q1 Results

We were impressed by how significantly Upwork blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 19.3% to $8.54 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).