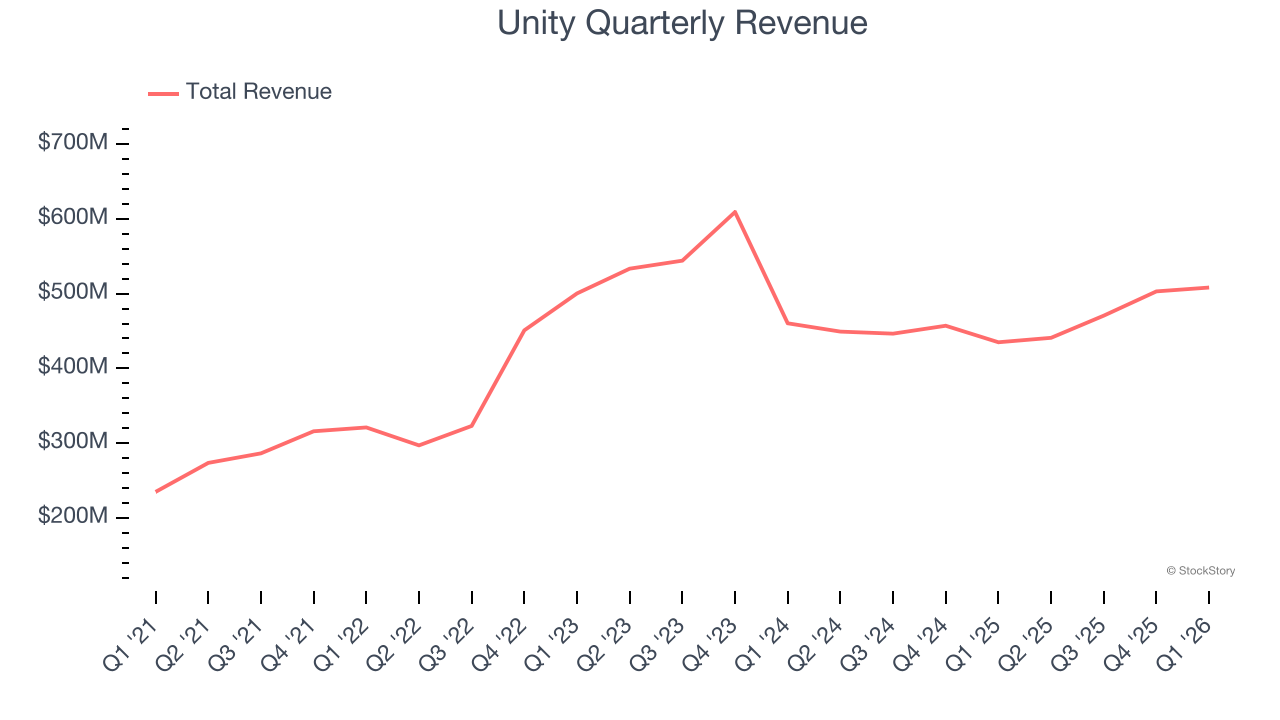

Interactive software platform Unity (NYSE: U) reported Q1 CY2026 results exceeding the market’s revenue expectations, with sales up 16.8% year on year to $508.2 million. The company expects next quarter’s revenue to be around $510 million, close to analysts’ estimates. Its non-GAAP profit of $0.23 per share was 4.2% below analysts’ consensus estimates.

Is now the time to buy Unity? Find out by accessing our full research report, it’s free.

Unity (U) Q1 CY2026 Highlights:

- Revenue: $508.2 million vs analyst estimates of $503.8 million (16.8% year-on-year growth, 0.9% beat)

- Adjusted EPS: $0.23 vs analyst expectations of $0.24 (4.2% miss)

- Adjusted Operating Income: -$274.2 million vs analyst estimates of $111.7 million (-54% margin, significant miss)

- Revenue Guidance for Q2 CY2026 is $510 million at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for Q2 CY2026 is $132.5 million at the midpoint, above analyst estimates of $131.1 million

- Operating Margin: -69.1%, down from -29.4% in the same quarter last year

- Free Cash Flow Margin: 13.1%, down from 23.6% in the previous quarter

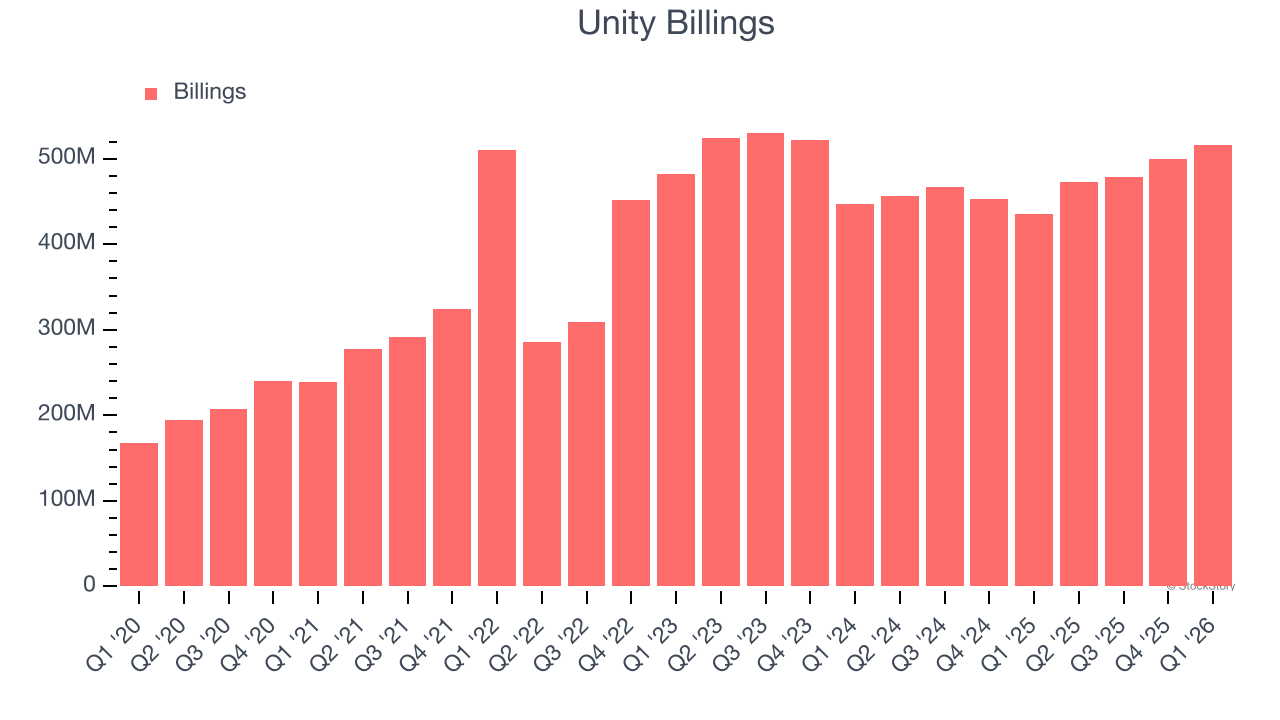

- Billings: $515.6 million at quarter end, up 18.5% year on year

- Market Capitalization: $11.9 billion

Company Overview

Powering over half of the world's mobile games and expanding into industries from automotive to architecture, Unity (NYSE: U) provides software tools and services that allow developers to create, run, and monetize interactive 2D and 3D content across multiple platforms.

Revenue Growth

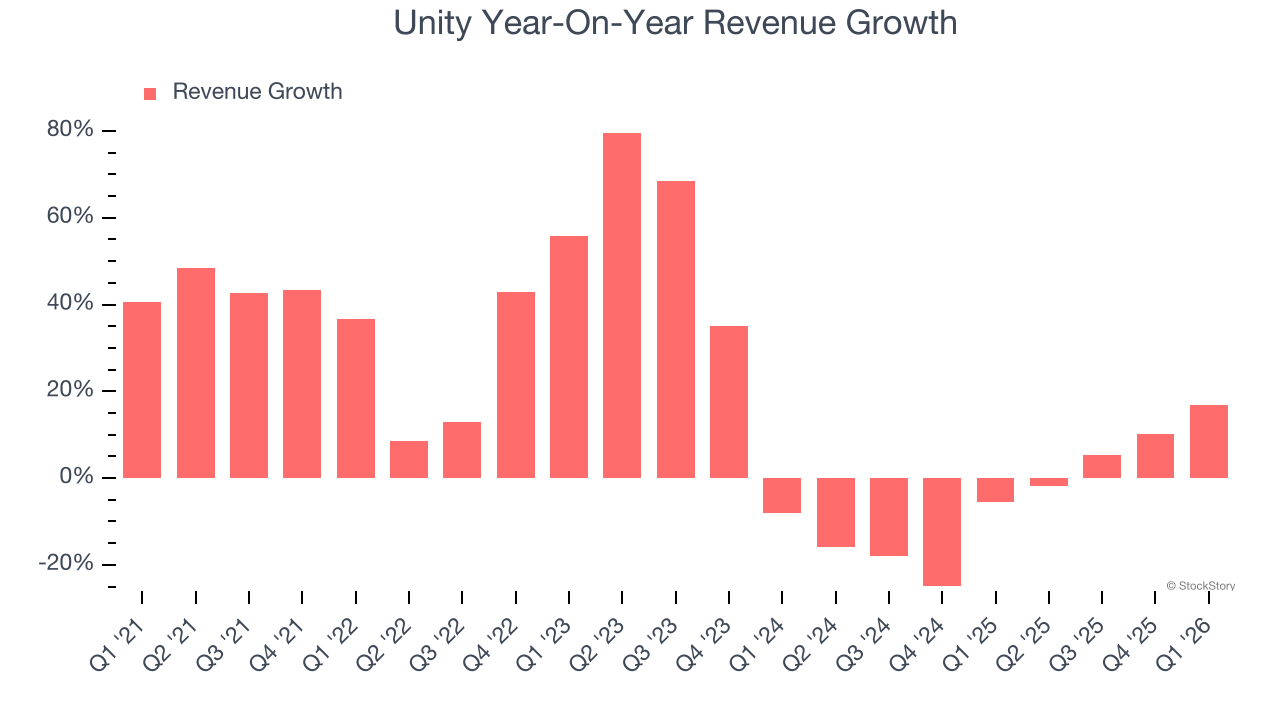

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Unity grew its sales at a decent 18% compounded annual growth rate. Its growth was slightly above the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Unity’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 5.4% over the last two years.

This quarter, Unity reported year-on-year revenue growth of 16.8%, and its $508.2 million of revenue exceeded Wall Street’s estimates by 0.9%. Company management is currently guiding for a 15.7% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.8% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Unity’s billings came in at $515.6 million in Q1, and over the last four quarters, its growth was underwhelming as it averaged 8.7% year-on-year increases. This performance mirrored its total sales and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Unity to acquire new customers as its CAC payback period checked in at 115.5 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

Key Takeaways from Unity’s Q1 Results

We enjoyed seeing Unity beat analysts’ EBITDA expectations this quarter. We were also glad its billings outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter was in line. Overall, this print had some key positives. The stock traded up 6.4% to $29.01 immediately after reporting.

Unity may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).