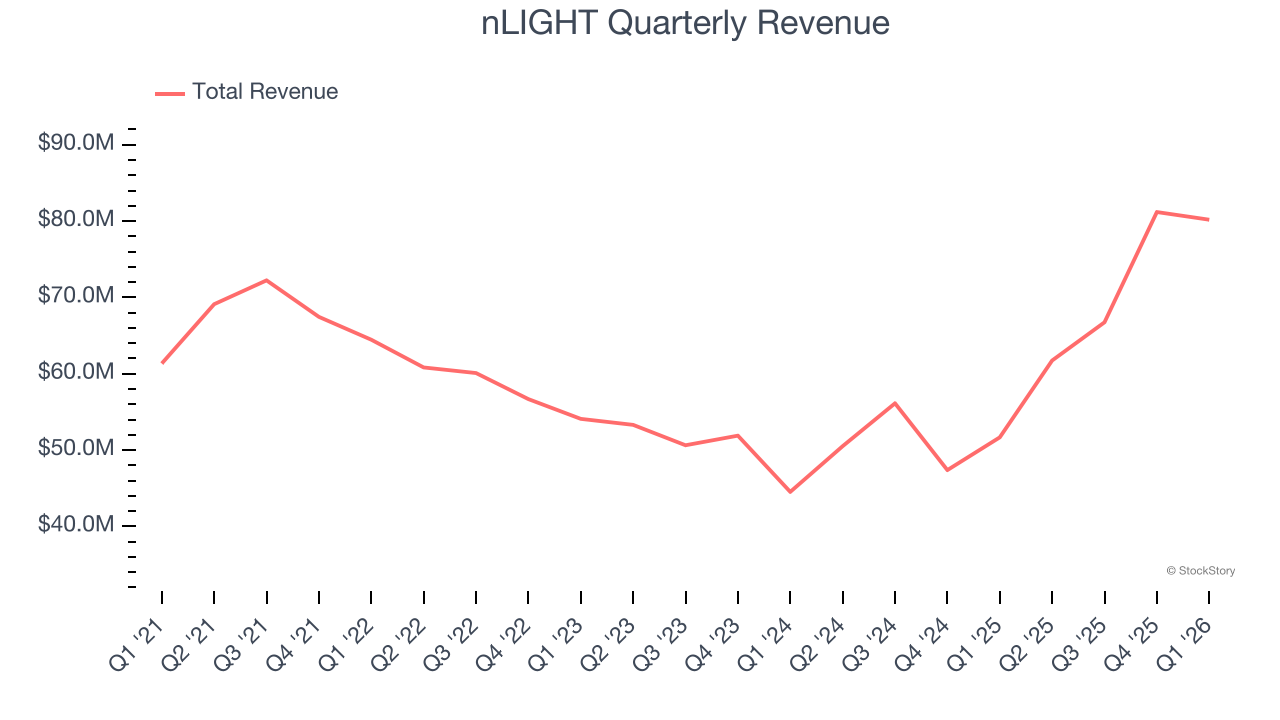

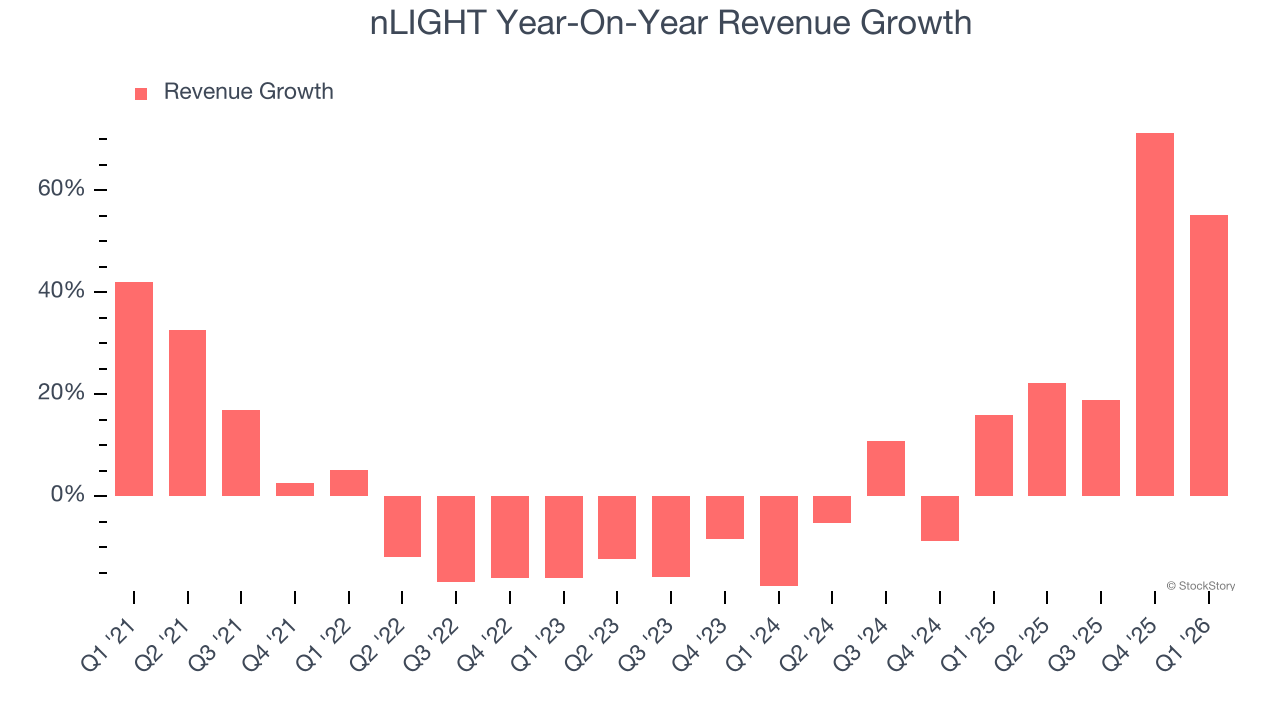

Laser company nLIGHT (NASDAQ: LASR) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 55.2% year on year to $80.18 million. On top of that, next quarter’s revenue guidance ($78 million at the midpoint) was surprisingly good and 9.9% above what analysts were expecting. Its non-GAAP profit of $0.20 per share was significantly above analysts’ consensus estimates.

Is now the time to buy nLIGHT? Find out by accessing our full research report, it’s free.

nLIGHT (LASR) Q1 CY2026 Highlights:

- Revenue: $80.18 million vs analyst estimates of $72.08 million (55.2% year-on-year growth, 11.2% beat)

- Adjusted EPS: $0.20 vs analyst estimates of $0.08 (significant beat)

- Adjusted EBITDA: $13.83 million vs analyst estimates of $7.21 million (17.2% margin, 91.8% beat)

- Revenue Guidance for Q2 CY2026 is $78 million at the midpoint, above analyst estimates of $70.97 million

- EBITDA guidance for Q2 CY2026 is $10 million at the midpoint, above analyst estimates of $6.69 million

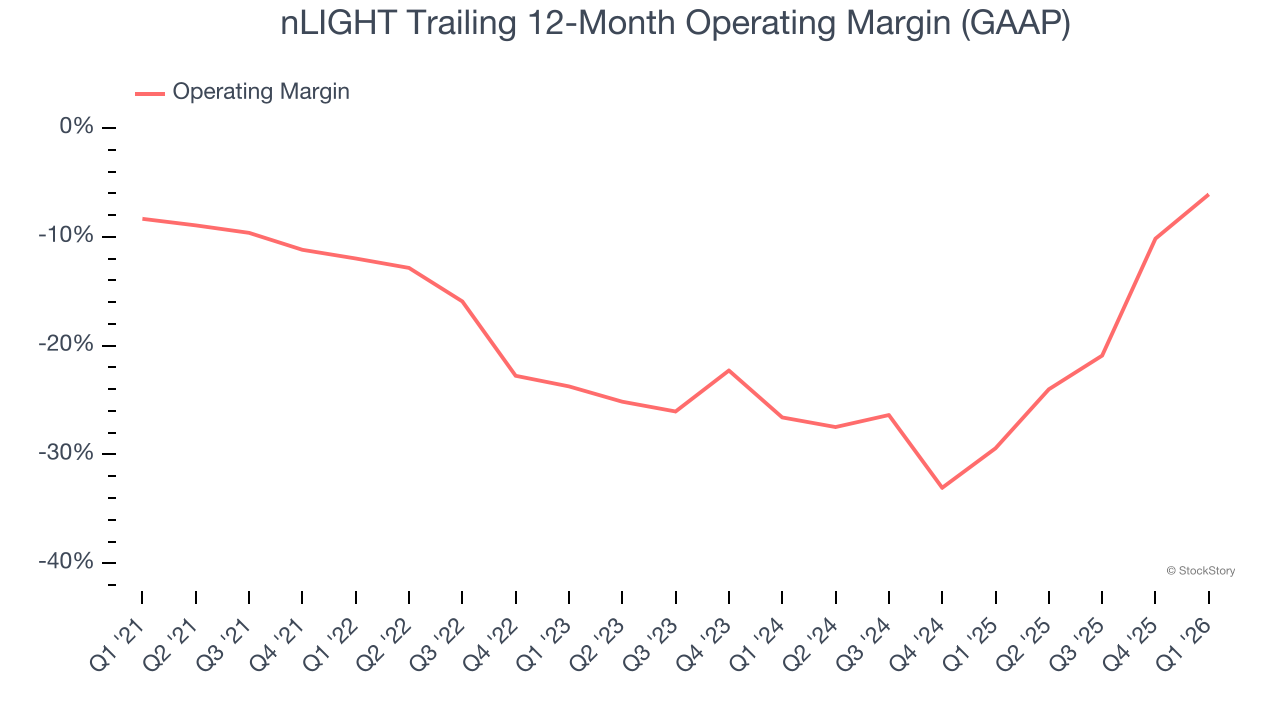

- Operating Margin: -0.9%, up from -18.6% in the same quarter last year

- Free Cash Flow was $7.57 million, up from -$2.30 million in the same quarter last year

- Market Capitalization: $4.02 billion

Company Overview

Founded by a former CEO and Harvard-educated entrepreneur Scott Keeneyn, nLIGHT (NASDAQ: LASR) offers semiconductor and fiber lasers to the industrial, aerospace & defense, and medical sectors.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, nLIGHT grew its sales at a sluggish 3.8% compounded annual growth rate. This was below our standard for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. nLIGHT’s annualized revenue growth of 20.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

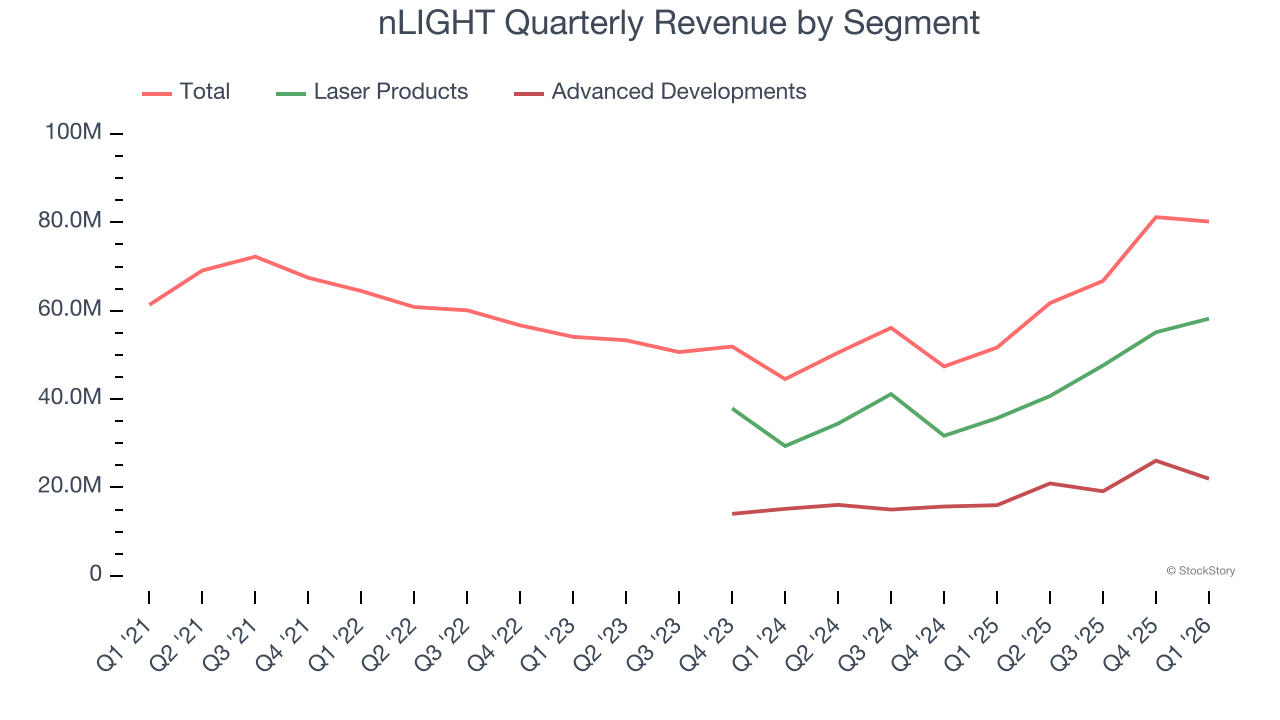

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Laser Products and Advanced Developments, which are 72.6% and 27.4% of revenue. Over the last two years, nLIGHT’s Laser Products revenue (lasers, amplifiers, and directed energy products) averaged 29.3% year-on-year growth while its Advanced Developments revenue (R&D contracts) averaged 29.8% growth.

This quarter, nLIGHT reported magnificent year-on-year revenue growth of 55.2%, and its $80.18 million of revenue beat Wall Street’s estimates by 11.2%. Company management is currently guiding for a 26.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 1.1% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Although nLIGHT broke even this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 18.3% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

On the plus side, nLIGHT’s operating margin rose by 5.9 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

nLIGHT’s operating margin was negative 0.9% this quarter. The company's consistent lack of profits raise a flag.

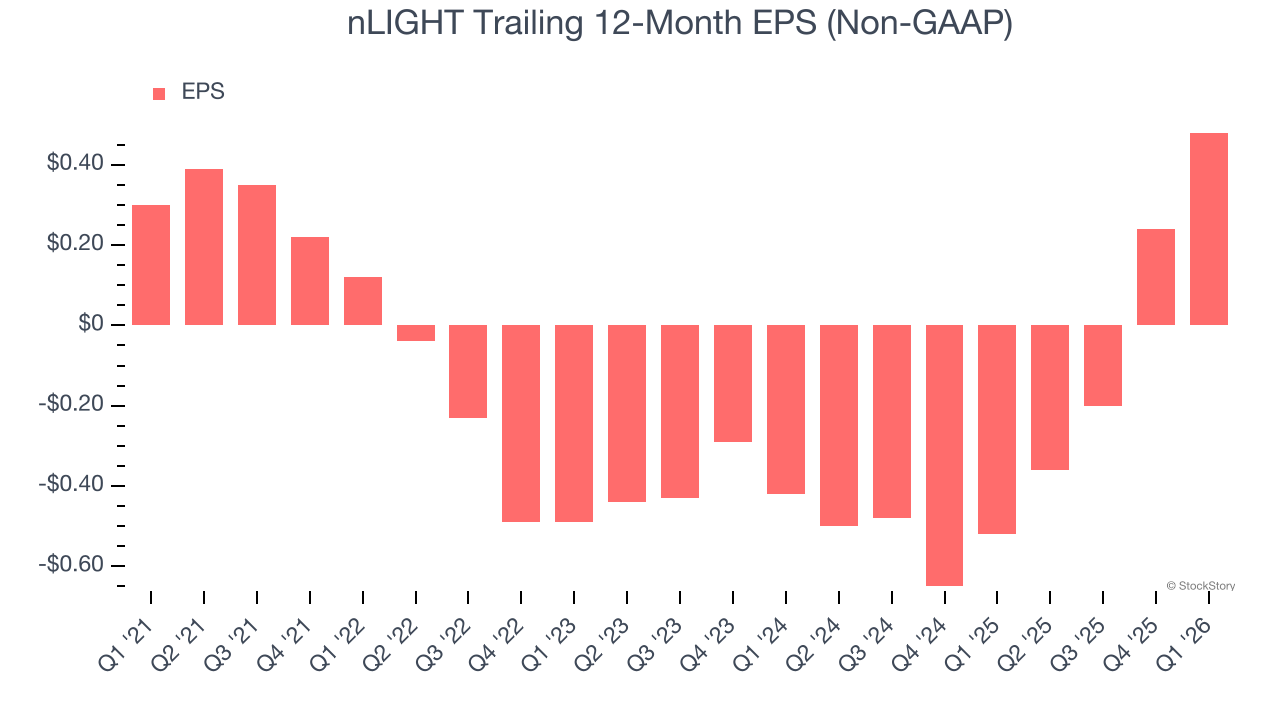

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

nLIGHT’s EPS grew at 9.9% compounded annual growth rate over the last five years, higher than its 3.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into nLIGHT’s earnings to better understand the drivers of its performance. As we mentioned earlier, nLIGHT’s operating margin expanded by 5.9 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For nLIGHT, its two-year annual EPS growth of 77.3% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, nLIGHT reported adjusted EPS of $0.20, up from negative $0.04 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects nLIGHT’s full-year EPS of $0.48 to shrink by 27.7%.

Key Takeaways from nLIGHT’s Q1 Results

We were impressed by nLIGHT’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2.7% to $68.72 immediately following the results.

Indeed, nLIGHT had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).