United Airlines currently trades at $99.55 per share and has shown little upside over the past six months, posting a middling return of 2.2%. The stock also fell short of the S&P 500’s 7.9% gain during that period.

Is now the time to buy United Airlines, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think United Airlines Will Underperform?

We don't have much confidence in United Airlines. Here are three reasons there are better opportunities than UAL and a stock we'd rather own.

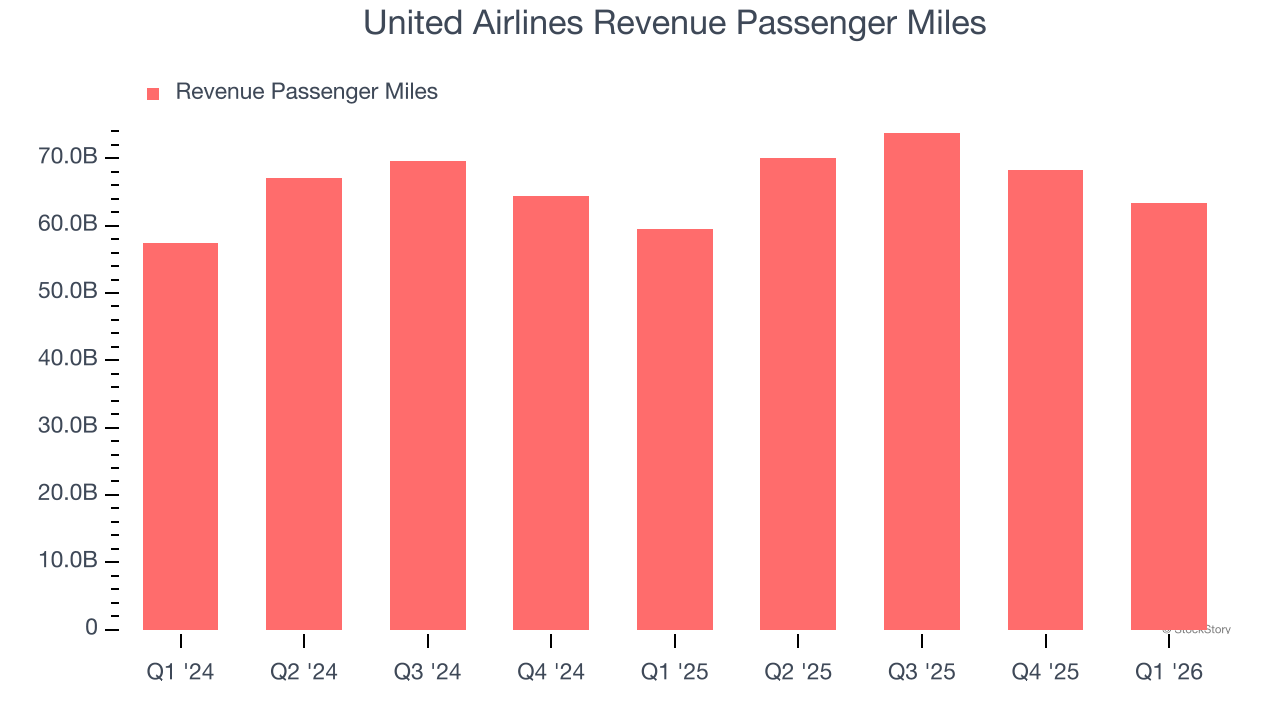

1. Weak Growth in Revenue Passenger Miles Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like United Airlines, our preferred volume metric is revenue passenger miles). While both are important, the latter is the most critical to analyze because prices have a ceiling.

United Airlines’s revenue passenger miles came in at 63.39 billion in the latest quarter, and over the last two years, averaged 5.3% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

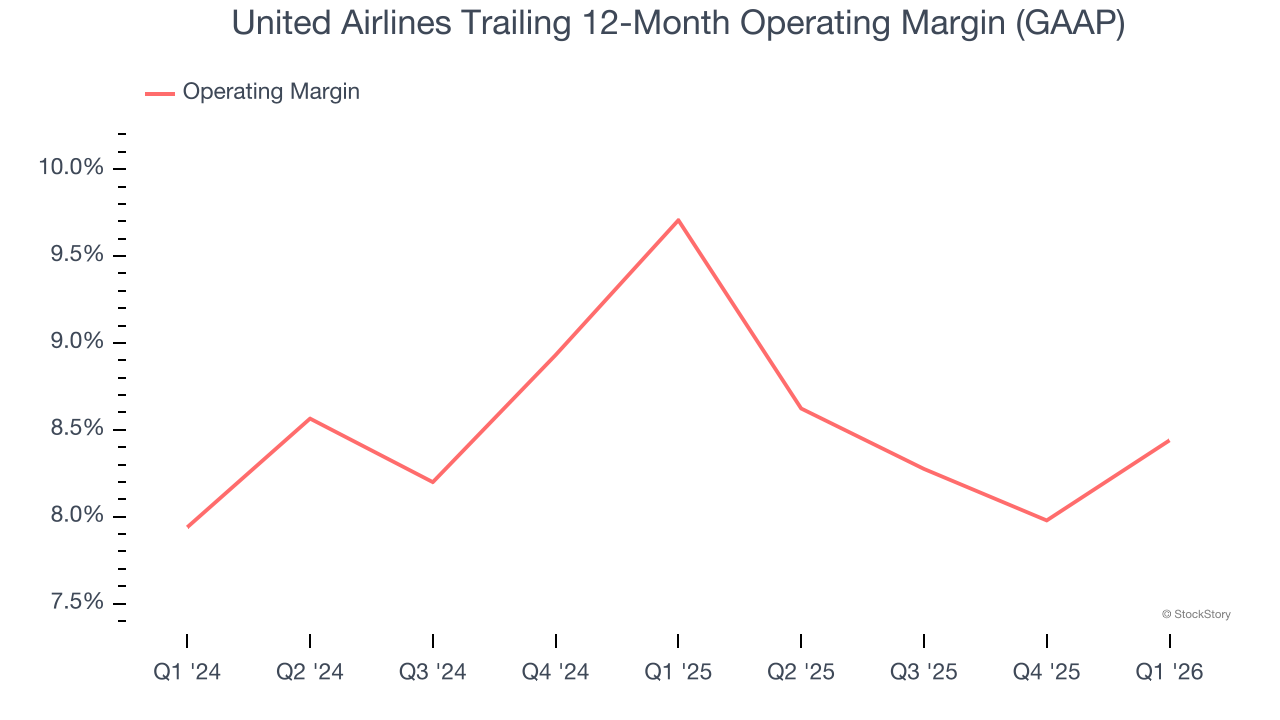

2. Weak Operating Margin Could Cause Trouble

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

United Airlines’s operating margin has been trending down over the last 12 months and averaged 9.1% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

3. Cash Flow Margin Set to Decline

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict United Airlines’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 5.3% for the last 12 months will decrease to 3.4%.

Final Judgment

We see the value of companies helping consumers, but in the case of United Airlines, we’re out. With its shares lagging the market recently, the stock trades at 10.4× forward P/E (or $99.55 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better investments elsewhere. We’d suggest looking at the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.