Senior living provider The Pennant Group (NASDAQ: PNTG) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 36.6% year on year to $285.4 million. Its non-GAAP profit of $0.32 per share was 4.9% above analysts’ consensus estimates.

Is now the time to buy The Pennant Group? Find out by accessing our full research report, it’s free.

The Pennant Group (PNTG) Q1 CY2026 Highlights:

- Revenue: $285.4 million vs analyst estimates of $280.7 million (36.6% year-on-year growth, 1.6% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.31 (4.9% beat)

- Adjusted EBITDA: $21.71 million vs analyst estimates of $21.48 million (7.6% margin, 1.1% beat)

- Operating Margin: 6.1%, in line with the same quarter last year

- Sales Volumes fell 3.3% year on year (28.9% in the same quarter last year)

- Market Capitalization: $1.1 billion

“Pennant is off to a strong start in 2026,” said Brent Guerisoli, the Company’s Chief Executive Officer.

Company Overview

Spun off from The Ensign Group in 2019 to focus on non-skilled nursing healthcare services, Pennant Group (NASDAQ: PNTG) operates home health, hospice, and senior living facilities across 13 western and midwestern states, serving patients of all ages including seniors.

Revenue Growth

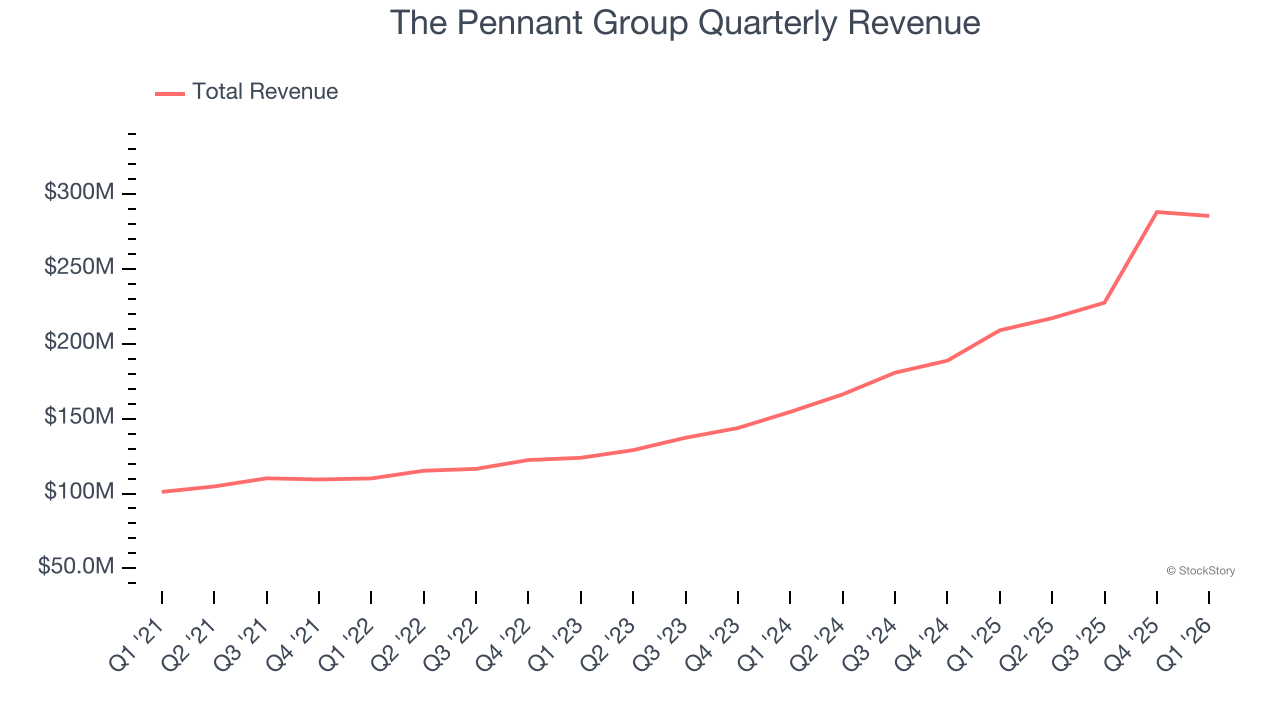

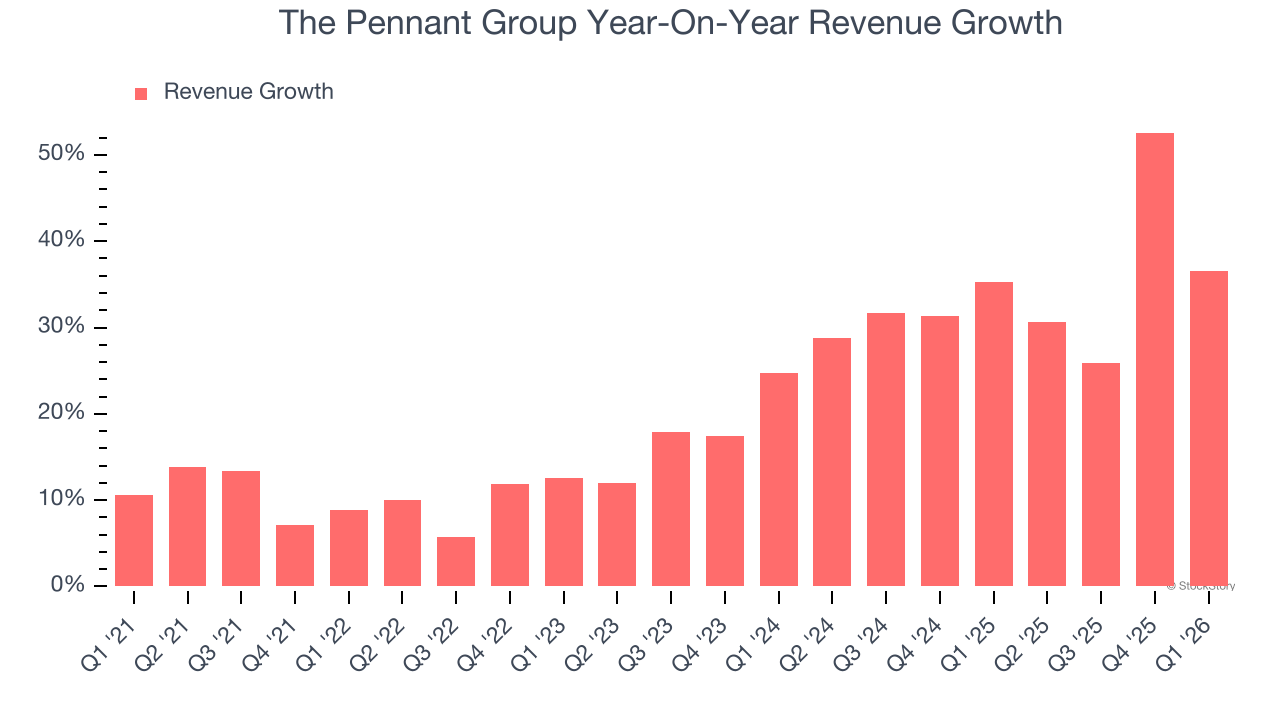

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Thankfully, The Pennant Group’s 21% annualized revenue growth over the last five years was impressive. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. The Pennant Group’s annualized revenue growth of 34.3% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

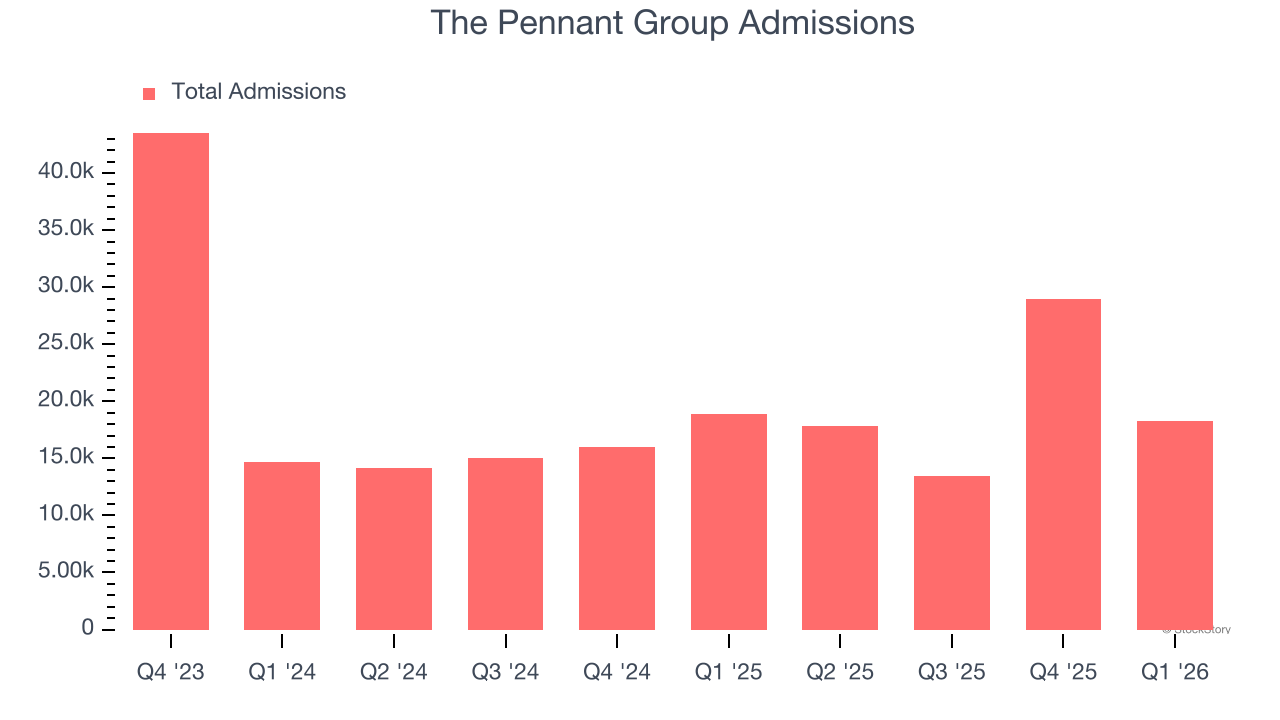

The Pennant Group also reports its number of admissions, which reached 18,264 in the latest quarter. Over the last two years, The Pennant Group’s admissions averaged 9.9% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, The Pennant Group reported wonderful year-on-year revenue growth of 36.6%, and its $285.4 million of revenue exceeded Wall Street’s estimates by 1.6%.

Looking ahead, sell-side analysts expect revenue to grow 16.1% over the next 12 months, a deceleration versus the last two years. Still, this projection is healthy and indicates the market is forecasting success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Adjusted Operating Margin

Adjusted operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies because it excludes non-recurring expenses, interest on debt, and taxes.

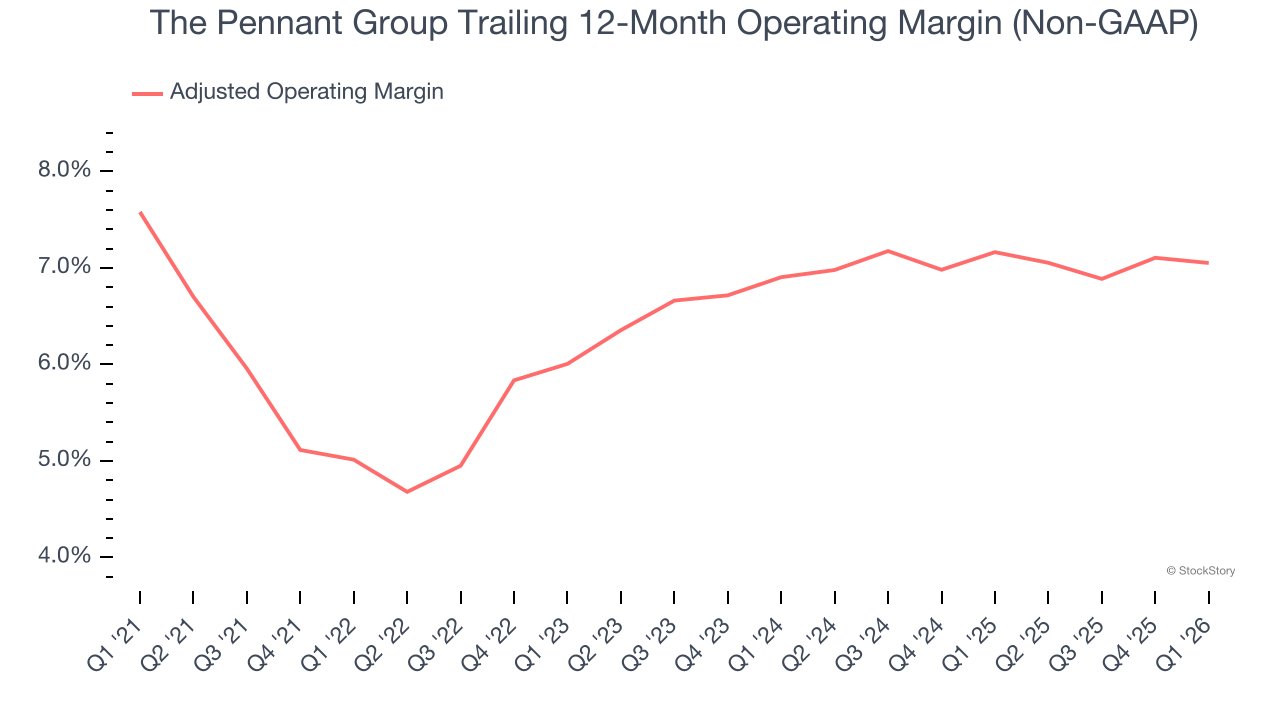

The Pennant Group was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 6.6% was weak for a healthcare business.

On the plus side, The Pennant Group’s adjusted operating margin rose by 2 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, The Pennant Group generated an adjusted operating margin profit margin of 7%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

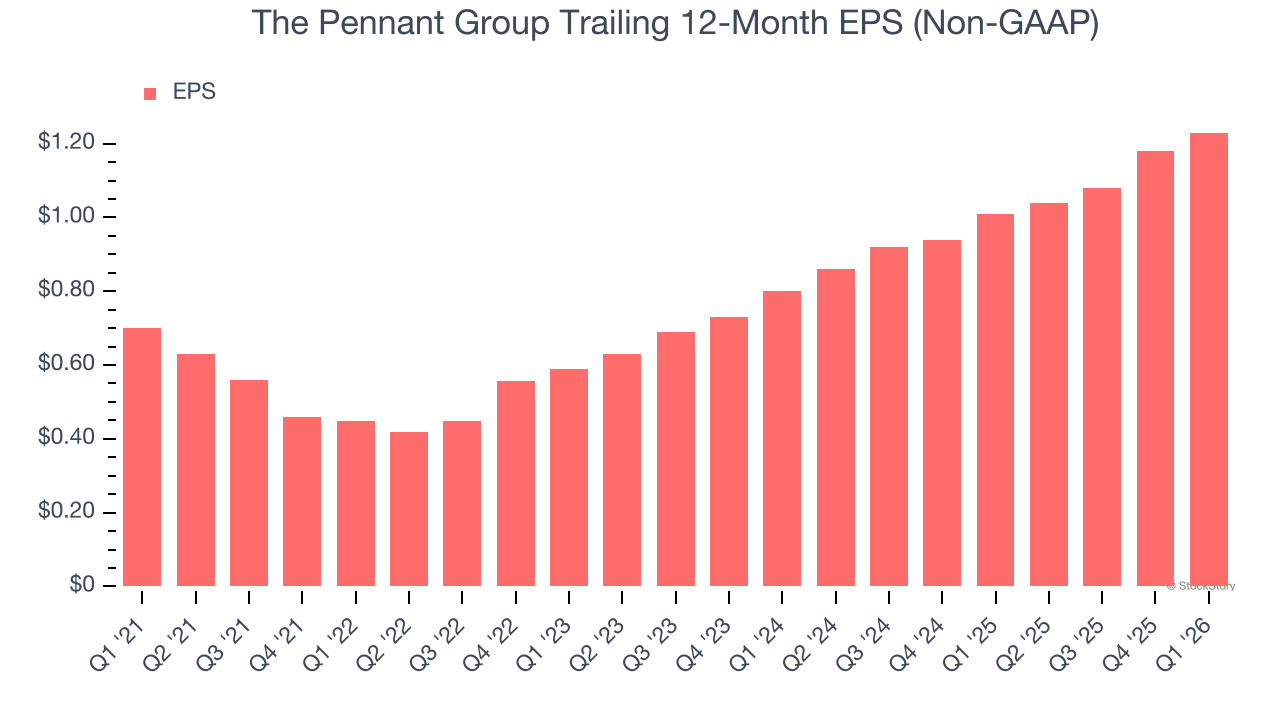

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

The Pennant Group’s EPS grew at a remarkable 11.9% compounded annual growth rate over the last five years. Despite its adjusted operating margin improvement during that time, this performance was lower than its 21% annualized revenue growth, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

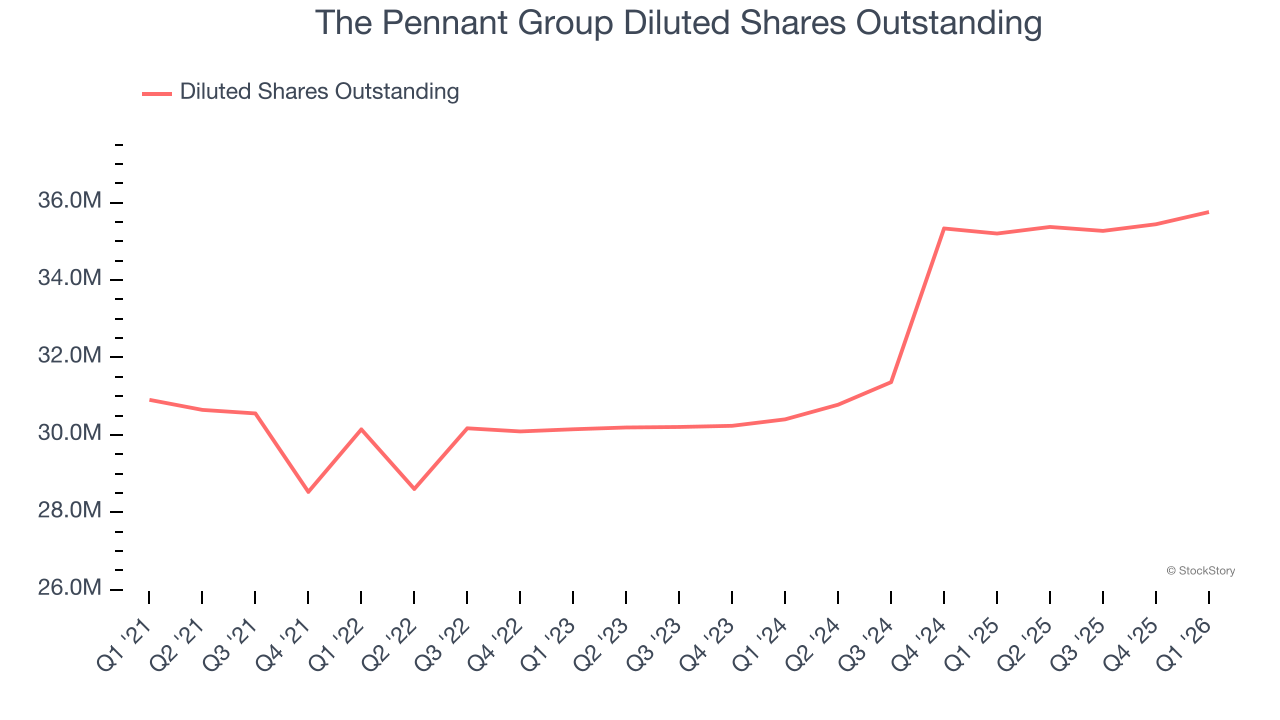

Diving into the nuances of The Pennant Group’s earnings can give us a better understanding of its performance. A five-year view shows The Pennant Group has diluted its shareholders, growing its share count by 15.7%. This dilution overshadowed its increased operational efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, The Pennant Group reported adjusted EPS of $0.32, up from $0.27 in the same quarter last year. This print beat analysts’ estimates by 4.9%. Over the next 12 months, Wall Street expects The Pennant Group’s full-year EPS of $1.23 to grow 12.7%.

Key Takeaways from The Pennant Group’s Q1 Results

It was encouraging to see The Pennant Group beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $32.53 immediately after reporting.

The Pennant Group may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).