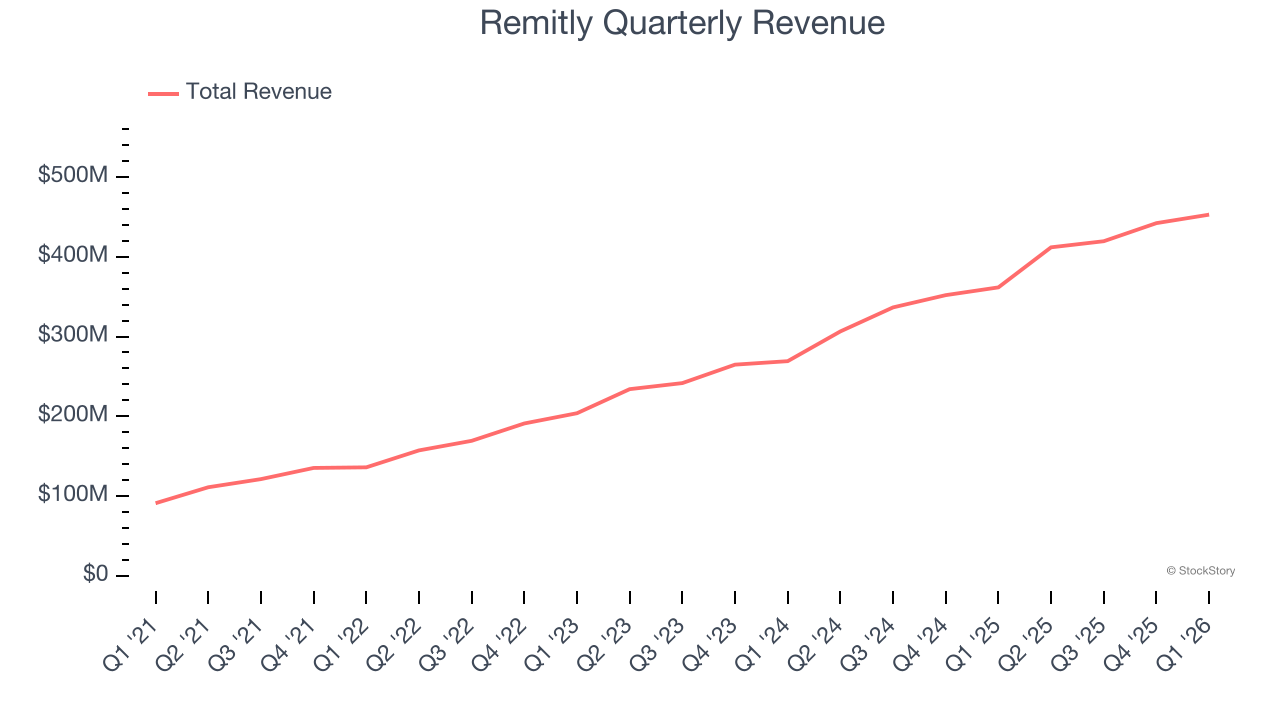

Online money transfer platform Remitly (NASDAQ: RELY) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 25.2% year on year to $452.8 million. The company expects next quarter’s revenue to be around $484 million, close to analysts’ estimates. Its GAAP profit of $0.23 per share was 93.3% above analysts’ consensus estimates.

Is now the time to buy Remitly? Find out by accessing our full research report, it’s free.

Remitly (RELY) Q1 CY2026 Highlights:

- Revenue: $452.8 million vs analyst estimates of $439 million (25.2% year-on-year growth, 3.2% beat)

- EPS (GAAP): $0.23 vs analyst estimates of $0.12 (93.3% beat)

- Adjusted EBITDA: $101.6 million vs analyst estimates of $83.7 million (22.4% margin, 21.3% beat)

- The company slightly lifted its revenue guidance for the full year to $1.97 billion at the midpoint from $1.95 billion

- EBITDA guidance for the full year is $377.5 million at the midpoint, above analyst estimates of $354.7 million

- Operating Margin: 11.9%, up from 3.4% in the same quarter last year

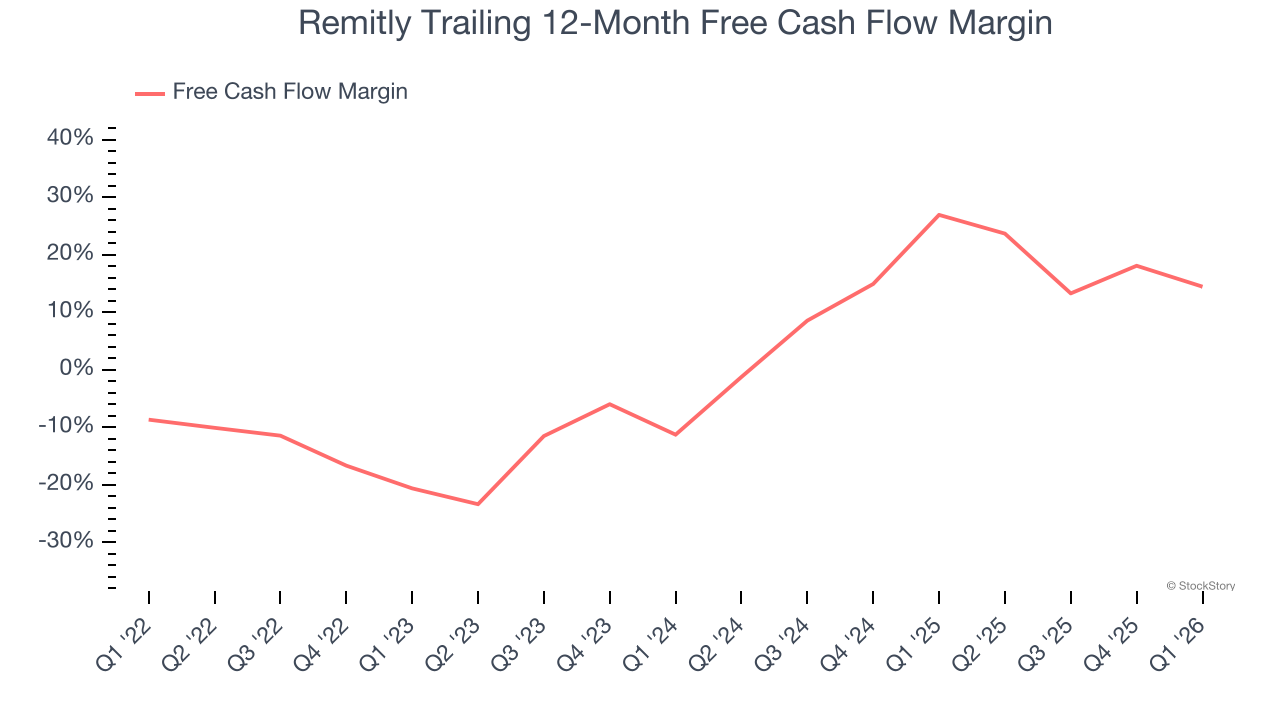

- Free Cash Flow Margin: 16.1%, down from 32.4% in the previous quarter

- Market Capitalization: $4.99 billion

“We delivered an exceptional Q1, achieving record revenue and Adjusted EBITDA,” said Sebastian Gunningham, Chief Executive Officer, Remitly.

Company Overview

With Amazon founder Jeff Bezos as an early investor, Remitly (NASDAQ: RELY) is an online platform that enables consumers to safely and quickly send money globally.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Remitly grew its sales at an incredible 33.8% compounded annual growth rate. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Remitly reported robust year-on-year revenue growth of 25.2%, and its $452.8 million of revenue topped Wall Street estimates by 3.2%. Company management is currently guiding for a 17.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 18.1% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and implies the market sees success for its products and services.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Remitly has shown robust cash profitability, driven by its cost-effective customer acquisition strategy that enables it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 19.9% over the last two years, quite impressive for a consumer internet business.

Taking a step back, we can see that Remitly’s margin expanded by 35.1 percentage points over the last few years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Remitly’s free cash flow clocked in at $72.71 million in Q1, equivalent to a 16.1% margin. The company’s cash profitability regressed as it was 16.8 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

Key Takeaways from Remitly’s Q1 Results

We were impressed by how significantly Remitly blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. Investors were likely hoping for more, and shares traded down 4.3% to $22.69 immediately following the results.

So do we think Remitly is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).