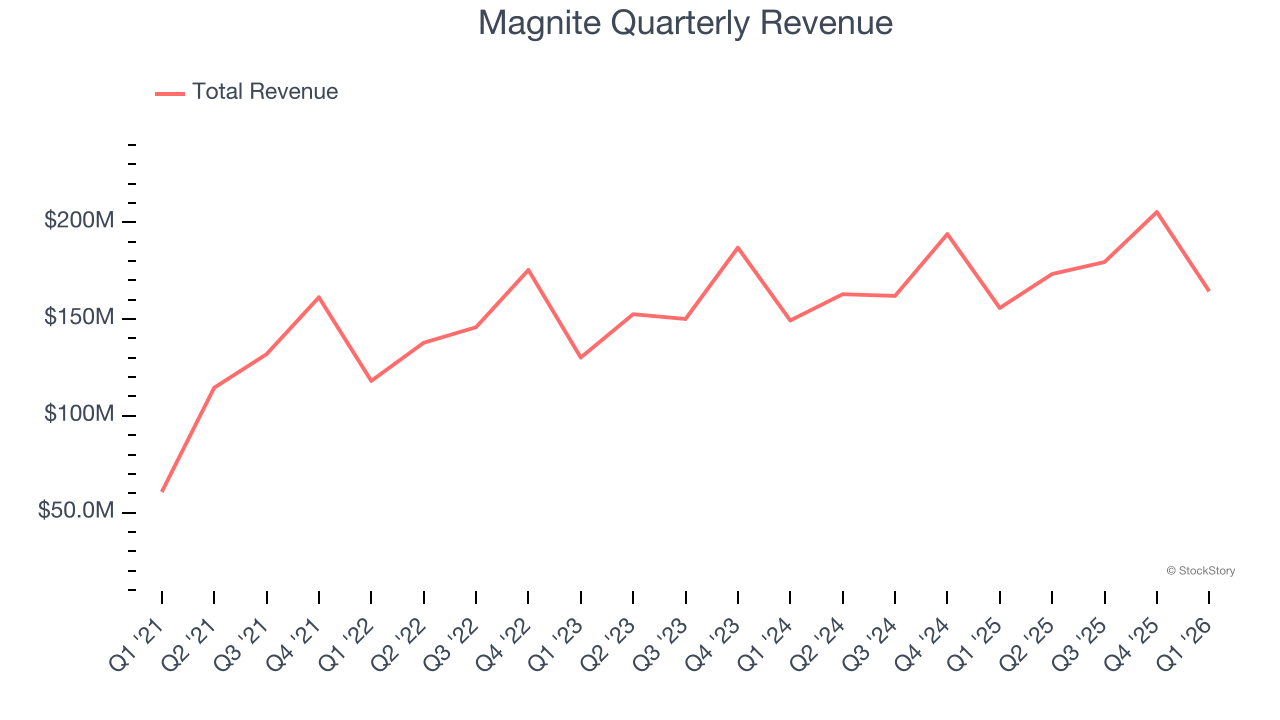

Digital advertising platform Magnite (NASDAQ: MGNI) missed Wall Street’s revenue expectations in Q1 CY2026, but sales rose 5.5% year on year to $164.4 million. Its non-GAAP profit of $0.13 per share was 23% above analysts’ consensus estimates.

Is now the time to buy Magnite? Find out by accessing our full research report, it’s free.

Magnite (MGNI) Q1 CY2026 Highlights:

- Revenue: $164.4 million vs analyst estimates of $174 million (5.5% year-on-year growth, 5.5% miss)

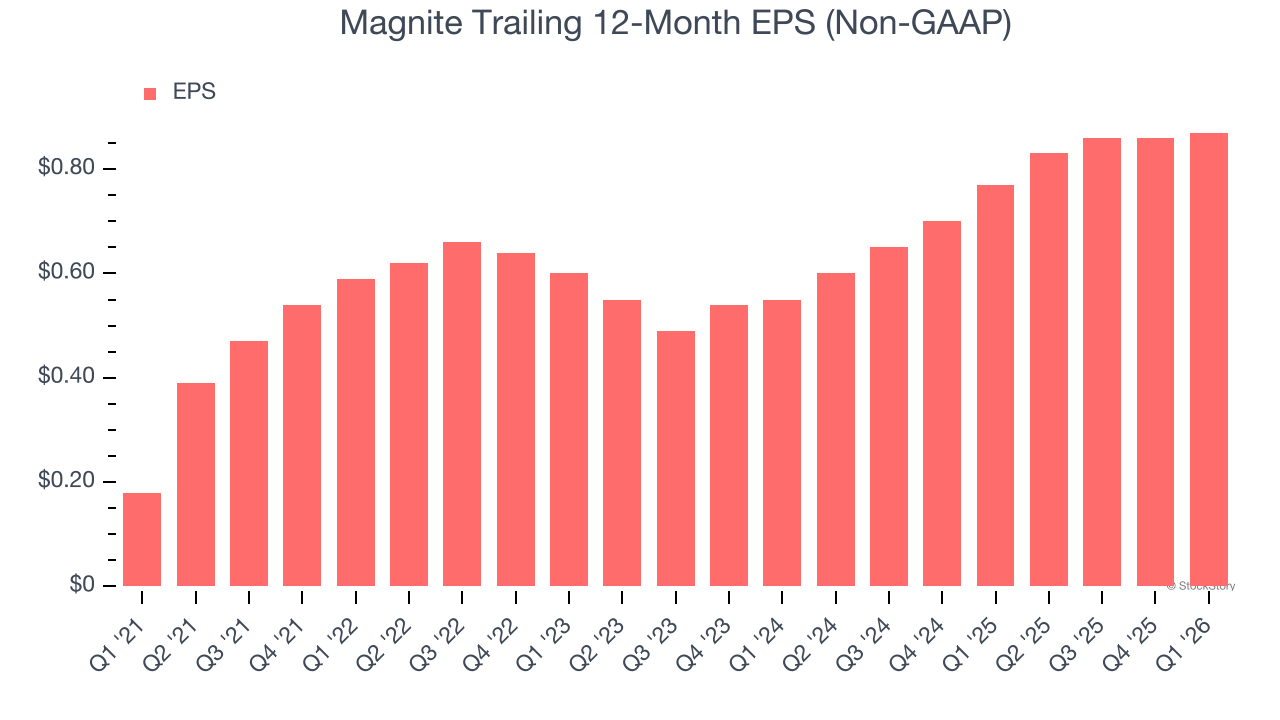

- Adjusted EPS: $0.13 vs analyst estimates of $0.11 (23% beat)

- Adjusted EBITDA: $42.86 million vs analyst estimates of $37.37 million (26.1% margin, 14.7% beat)

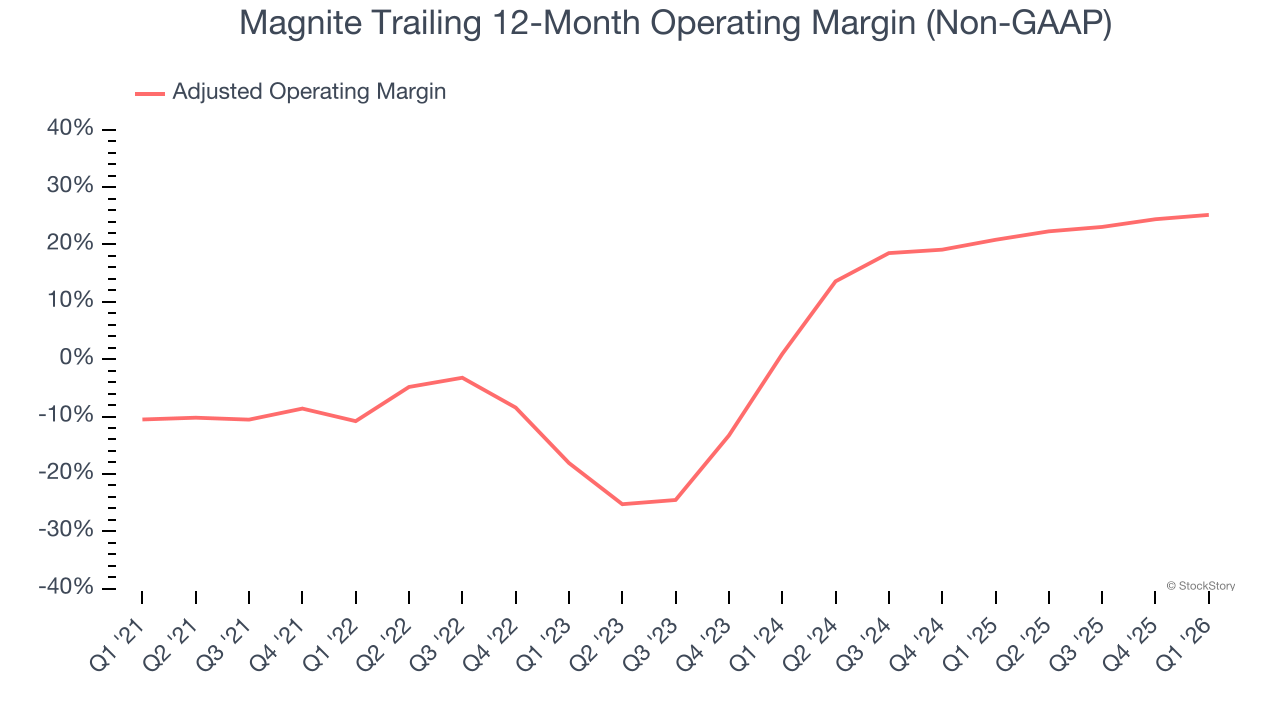

- Operating Margin: 4.7%, up from -0.9% in the same quarter last year

- Free Cash Flow was -$130.2 million compared to -$11.82 million in the same quarter last year

- Market Capitalization: $1.95 billion

“Magnite once again exceeded total top and bottom line expectations, with growth paced by CTV at 30%. Our CTV success is broad based and supported by publisher, agency and DSP momentum. Buyer marketplaces coupled with ClearLine, live sports, and strong SMB trends continue to support the growth acceleration in CTV. AI is also becoming foundational in almost every area of our business, from agentic buying, to creative development, to inventory curation, to workflow. It is powering greater productivity throughout our ecosystem and company. We are starting to see some improvements in key areas of DV+, namely mobile app and commerce media partners. We also remain ready in our DV+ business, as it relates to pending remedies related to the Google trial.” said Michael G. Barrett, CEO of Magnite.

Company Overview

Born from the 2020 merger of Rubicon Project and Telaria, Magnite (NASDAQ: MGNI) operates the world's largest independent sell-side advertising platform that automates the buying and selling of digital advertising inventory across all channels and formats.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $722.6 million in revenue over the past 12 months, Magnite is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

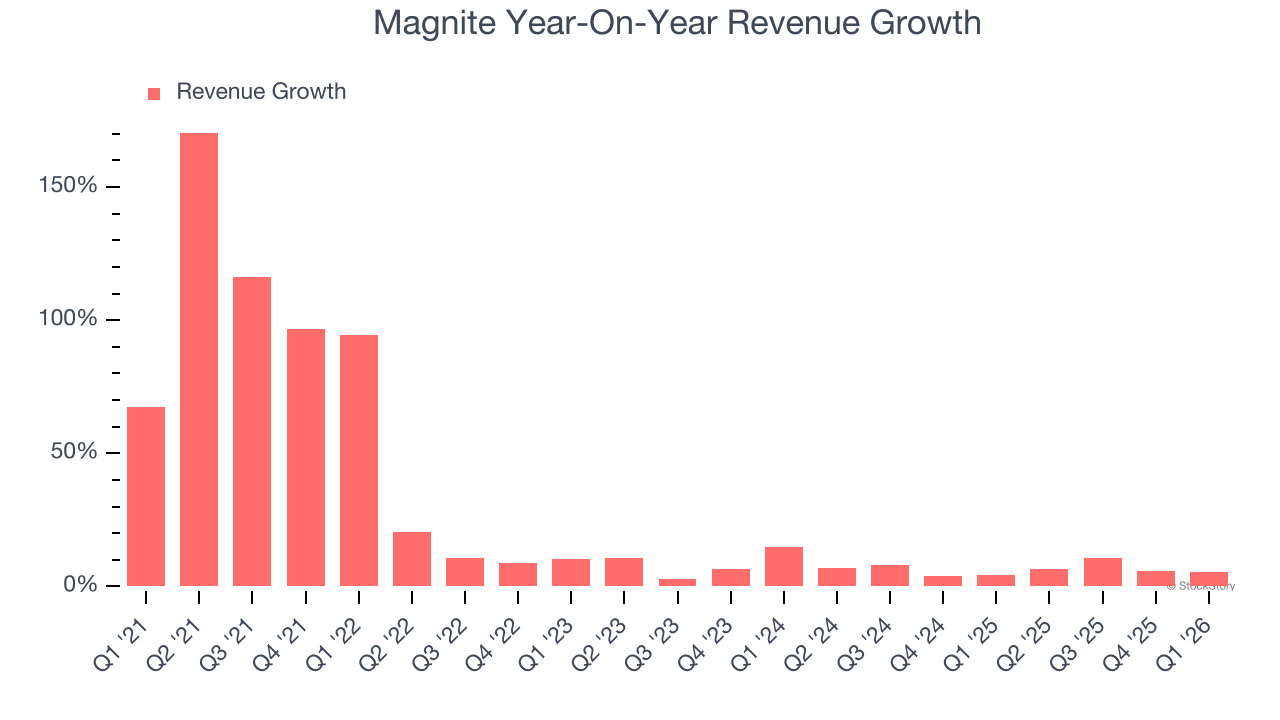

As you can see below, Magnite’s 24% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows Magnite’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Magnite’s annualized revenue growth of 6.3% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Magnite’s revenue grew by 5.5% year on year to $164.4 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 15.4% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will catalyze better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Adjusted Operating Margin

Magnite was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 5.2% was weak for a business services business.

On the plus side, Magnite’s adjusted operating margin rose by 36 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q1, Magnite generated an adjusted operating margin profit margin of 16.7%, up 3.9 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Magnite’s EPS grew at 37% compounded annual growth rate over the last five years, higher than its 24% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into Magnite’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Magnite’s adjusted operating margin expanded by 36 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Magnite, its two-year annual EPS growth of 25.8% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, Magnite reported adjusted EPS of $0.13, up from $0.12 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Magnite’s Q1 Results

It was good to see Magnite beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed. Overall, this print was mixed. Investors were likely hoping for more, and shares traded down 1.6% to $13.18 immediately after reporting.

Big picture, is Magnite a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).