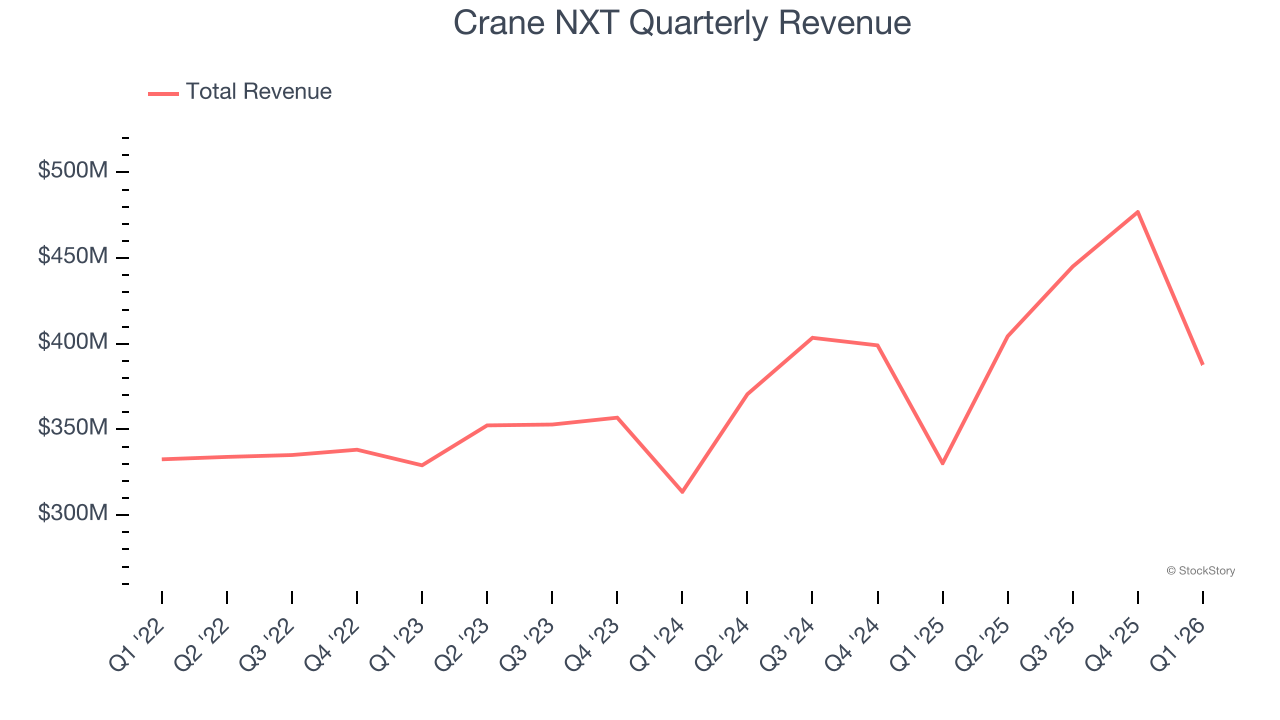

Payment technology company Crane NXT (NYSE: CXT) reported Q1 CY2026 results beating Wall Street’s revenue expectations, with sales up 17.4% year on year to $387.7 million. Its non-GAAP profit of $0.60 per share was 5.4% above analysts’ consensus estimates.

Is now the time to buy Crane NXT? Find out by accessing our full research report, it’s free.

Crane NXT (CXT) Q1 CY2026 Highlights:

- Revenue: $387.7 million vs analyst estimates of $378.1 million (17.4% year-on-year growth, 2.5% beat)

- Adjusted EPS: $0.60 vs analyst estimates of $0.57 (5.4% beat)

- Adjusted EBITDA: $74.7 million vs analyst estimates of $70.99 million (19.3% margin, 5.2% beat)

- Management reiterated its full-year Adjusted EPS guidance of $4.25 at the midpoint

- Operating Margin: 5.7%, down from 11.3% in the same quarter last year

- Free Cash Flow was -$24.1 million compared to -$30.5 million in the same quarter last year

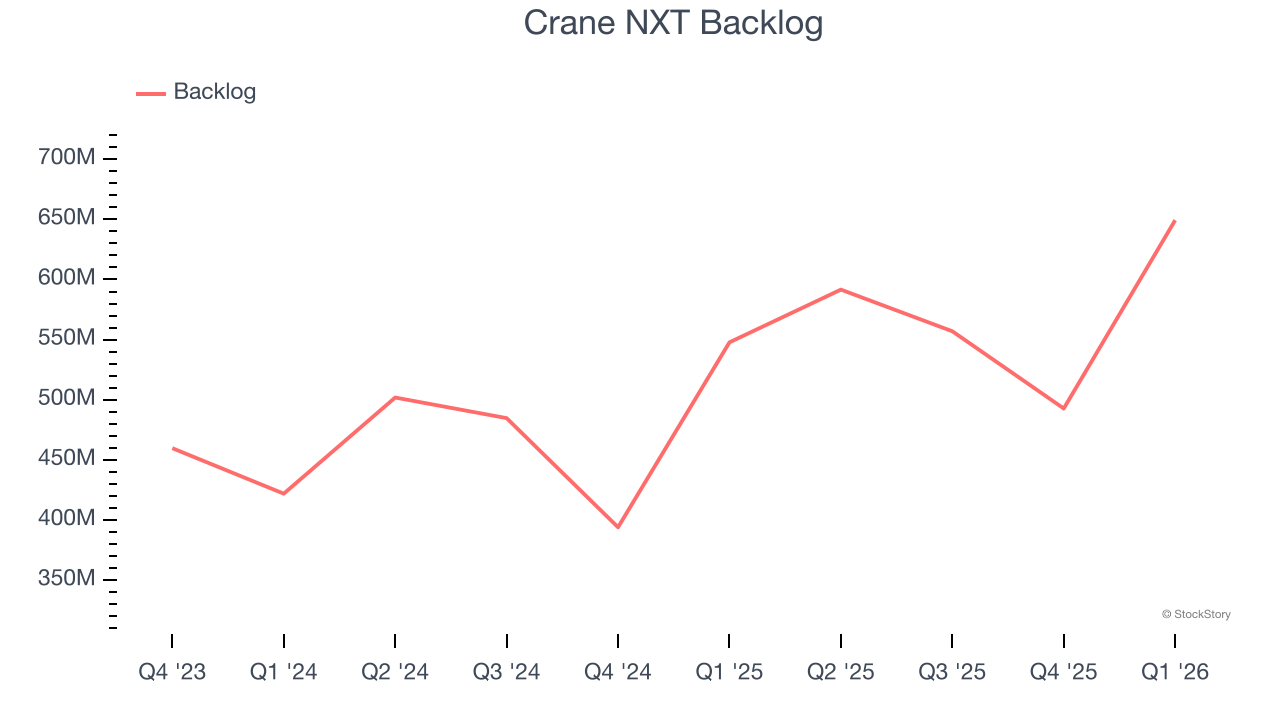

- Backlog: $649.3 million at quarter end, up 18.5% year on year

- Market Capitalization: $2.55 billion

Aaron W. Saak, Crane NXT's President and Chief Executive Officer, stated: "In the first quarter, we delivered on our value creation priorities, accelerating organic growth and building on our leadership positions. With the Antares Vision acquisition complete, our portfolio is increasingly integrated and aligned to growing markets with sustainable tailwinds."

Company Overview

Born from a corporate transformation completed in 2023, Crane NXT (NYSE: CXT) provides specialized technology solutions for payment processing, banknote security, and authentication systems for financial institutions and businesses.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $1.71 billion in revenue over the past 12 months, Crane NXT is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale. On the bright side, it can still flex high growth rates because it’s working from a smaller revenue base.

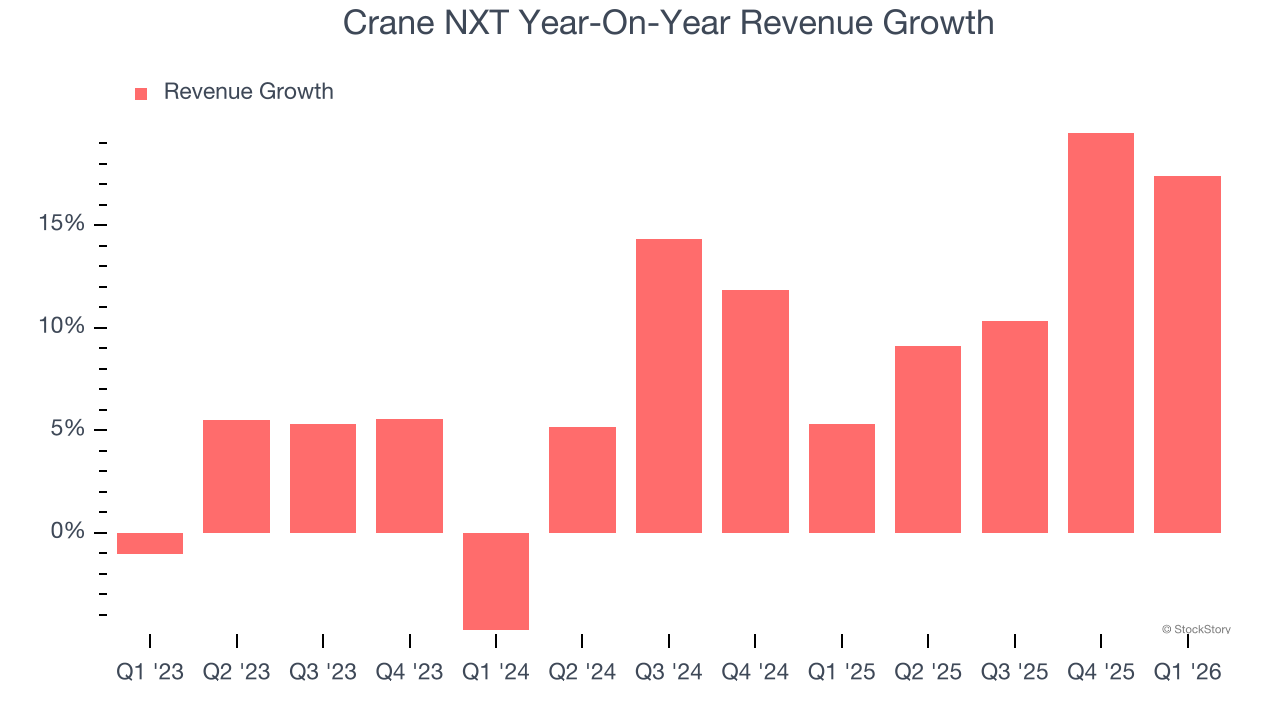

As you can see below, Crane NXT’s 8.3% annualized revenue growth over the last three years was solid. This shows it had high demand, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. Crane NXT’s annualized revenue growth of 11.6% over the last two years is above its three-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Crane NXT’s backlog reached $649.3 million in the latest quarter and averaged 15.3% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Crane NXT’s products and services but raises concerns about capacity constraints.

This quarter, Crane NXT reported year-on-year revenue growth of 17.4%, and its $387.7 million of revenue exceeded Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

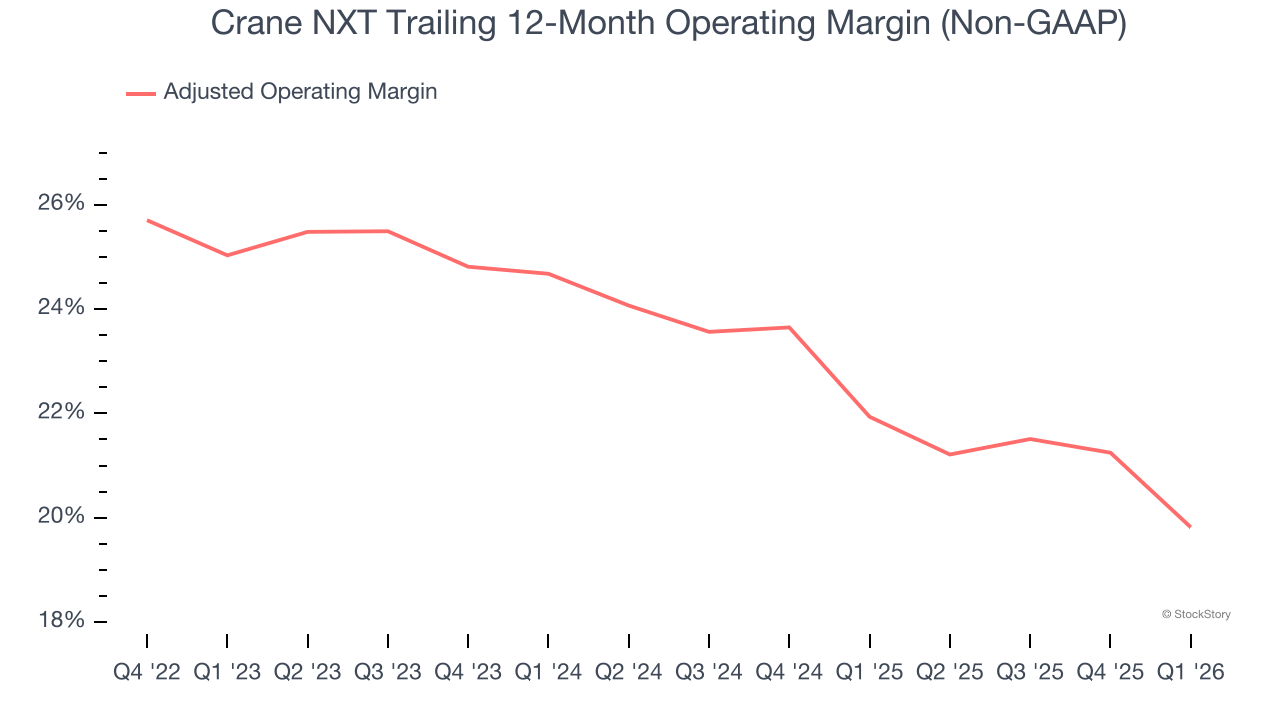

Crane NXT has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average adjusted operating margin of 22.8%.

Looking at the trend in its profitability, Crane NXT’s adjusted operating margin decreased by 5.2 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q1, Crane NXT generated an adjusted operating margin profit margin of 9.5%, down 5.4 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

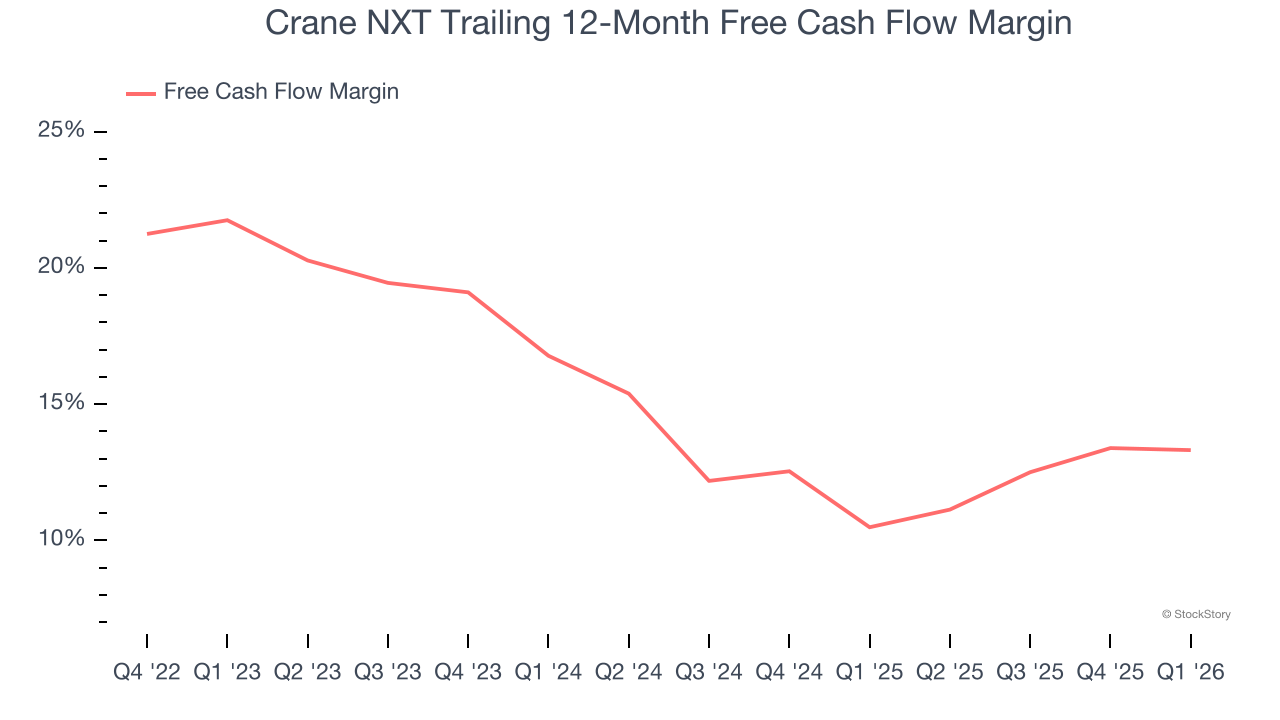

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Crane NXT has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the business services sector, averaging 14.9% over the last five years.

Taking a step back, we can see that Crane NXT’s margin dropped by 8.4 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity.

Crane NXT burned through $24.1 million of cash in Q1, equivalent to a negative 6.2% margin. The company’s cash burn was similar to its $30.5 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

Key Takeaways from Crane NXT’s Q1 Results

We enjoyed seeing Crane NXT beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance was in line. Overall, this print had some key positives. The stock remained flat at $45.64 immediately after reporting.

Should you buy the stock or not? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).