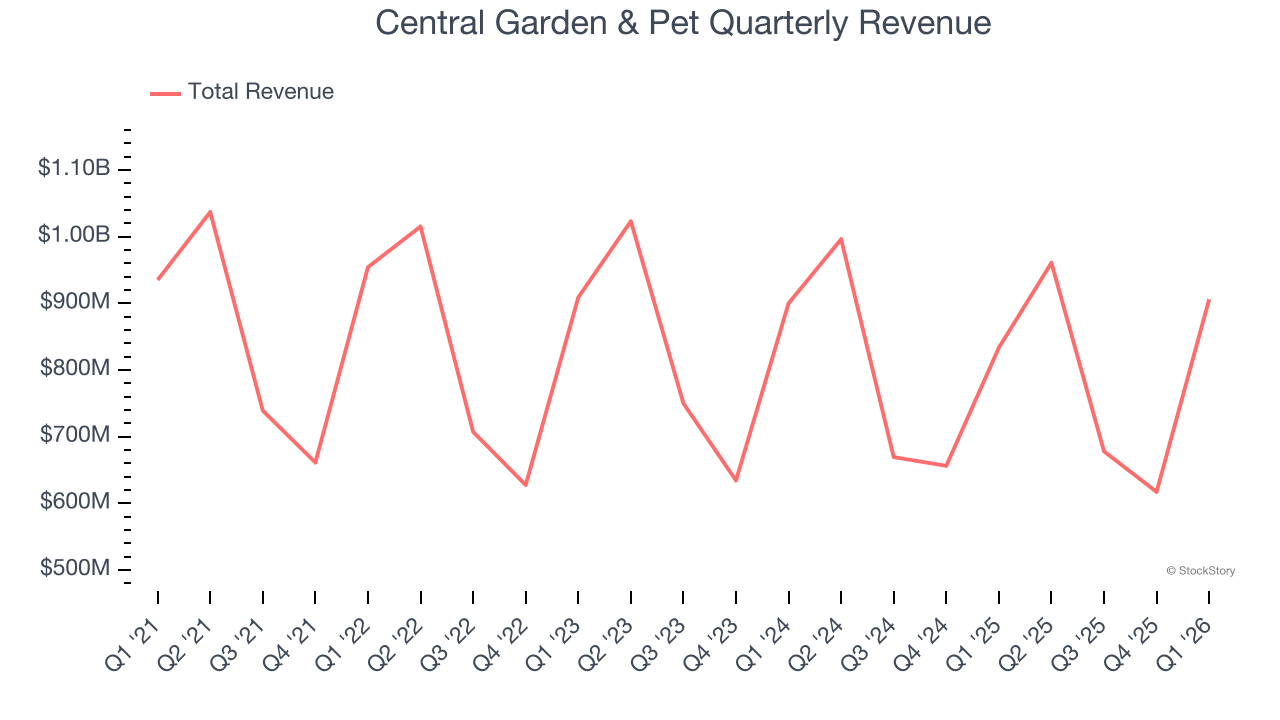

Pet company Central Garden & Pet (NASDAQ: CENT) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 8.7% year on year to $906.2 million. Its non-GAAP profit of $1.29 per share was 17.3% above analysts’ consensus estimates.

Is now the time to buy Central Garden & Pet? Find out by accessing our full research report, it’s free.

Central Garden & Pet (CENT) Q1 CY2026 Highlights:

- Revenue: $906.2 million vs analyst estimates of $851.4 million (8.7% year-on-year growth, 6.4% beat)

- Adjusted EPS: $1.29 vs analyst estimates of $1.10 (17.3% beat)

- Adjusted EBITDA: $189.2 million vs analyst estimates of $124.1 million (20.9% margin, 52.5% beat)

- Management reiterated its full-year Adjusted EPS guidance of $2.70 at the midpoint

- Operating Margin: 12.6%, up from 11.2% in the same quarter last year

- Free Cash Flow was -$60.09 million compared to -$57.52 million in the same quarter last year

- Market Capitalization: $2.07 billion

Company Overview

Enhancing the lives of both pets and homeowners, Central Garden & Pet (NASDAQ: CENT) is a leading producer and distributor of essential products for pet care, lawn and garden maintenance, and pest control.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $3.16 billion in revenue over the past 12 months, Central Garden & Pet carries some recognizable products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Central Garden & Pet’s demand was weak over the last three years. Its sales fell by 1% annually, a rough starting point for our analysis.

This quarter, Central Garden & Pet reported year-on-year revenue growth of 8.7%, and its $906.2 million of revenue exceeded Wall Street’s estimates by 6.4%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection is underwhelming and indicates its newer products will not catalyze better top-line performance yet.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Cash Is King

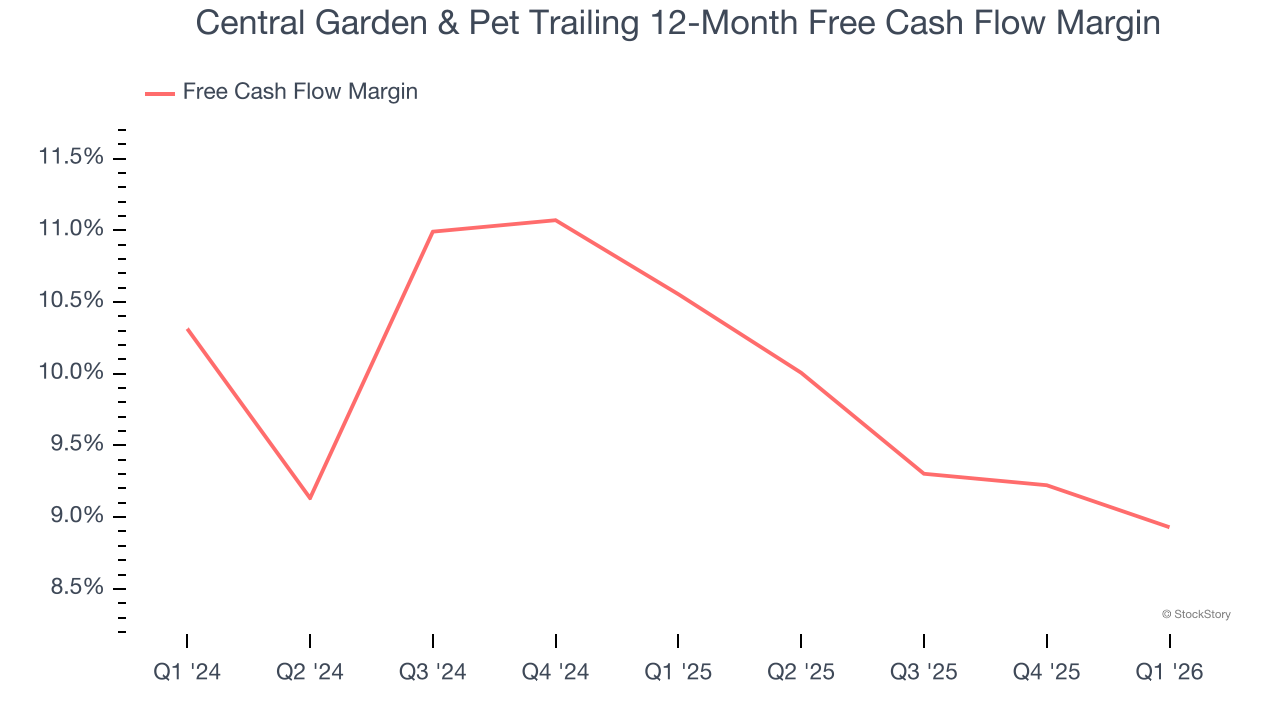

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Central Garden & Pet has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 9.7% over the last two years, quite impressive for a consumer staples business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Central Garden & Pet’s margin dropped by 1.6 percentage points over the last year. If its declines continue, it could signal increasing investment needs and capital intensity.

Central Garden & Pet burned through $60.09 million of cash in Q1, equivalent to a negative 6.6% margin. The company’s cash burn was similar to its $57.52 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

Key Takeaways from Central Garden & Pet’s Q1 Results

We were impressed by how significantly Central Garden & Pet blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EPS guidance missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 2.4% to $37.78 immediately after reporting.

Indeed, Central Garden & Pet had a rock-solid quarterly earnings result, but is this stock a good investment here? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).