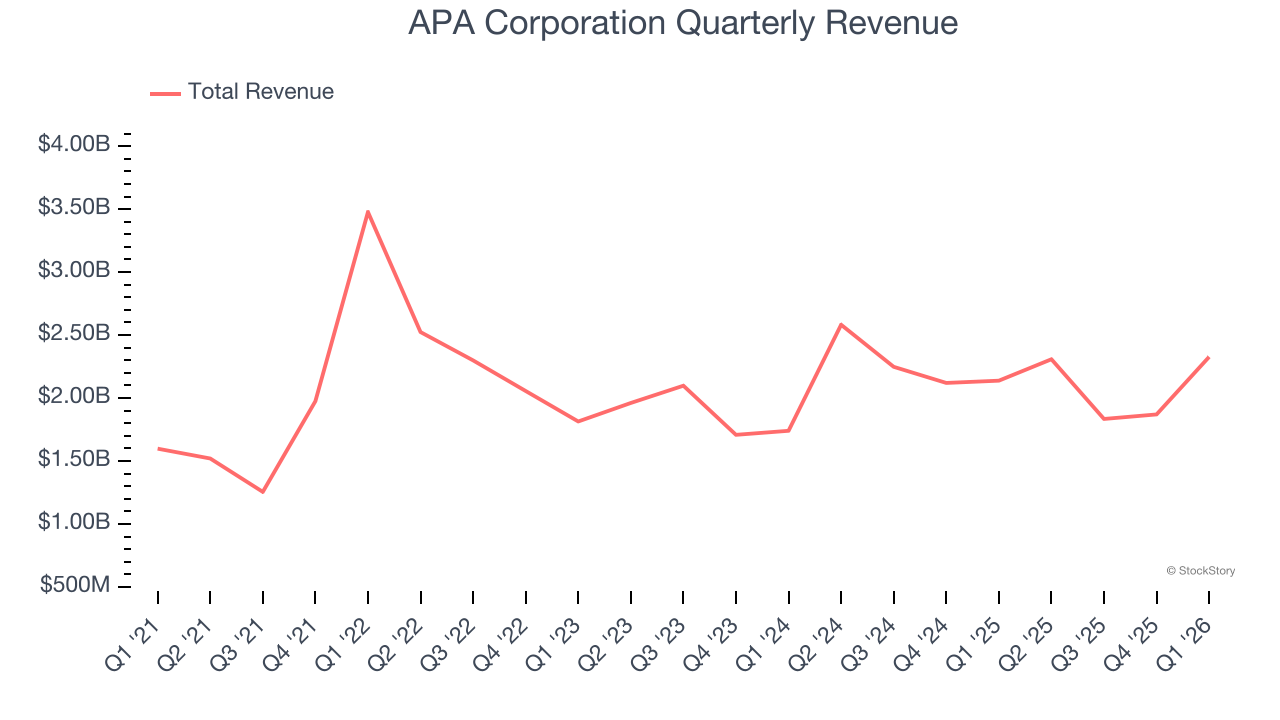

Oil and gas producer APA Corporation (NASDAQ: APA) announced better-than-expected revenue in Q1 CY2026, with sales up 8.8% year on year to $2.33 billion. Its non-GAAP profit of $1.38 per share was 20.9% above analysts’ consensus estimates.

Is now the time to buy APA Corporation? Find out by accessing our full research report, it’s free.

APA Corporation (APA) Q1 CY2026 Highlights:

- Revenue: $2.33 billion vs analyst estimates of $2.08 billion (8.8% year-on-year growth, 12% beat)

- Adjusted EPS: $1.38 vs analyst estimates of $1.14 (20.9% beat)

- Adjusted Operating Income: $914 million vs analyst estimates of $838.4 million (39.3% margin, 9% beat)

- Operating Margin: 35.7%, up from 34.6% in the same quarter last year

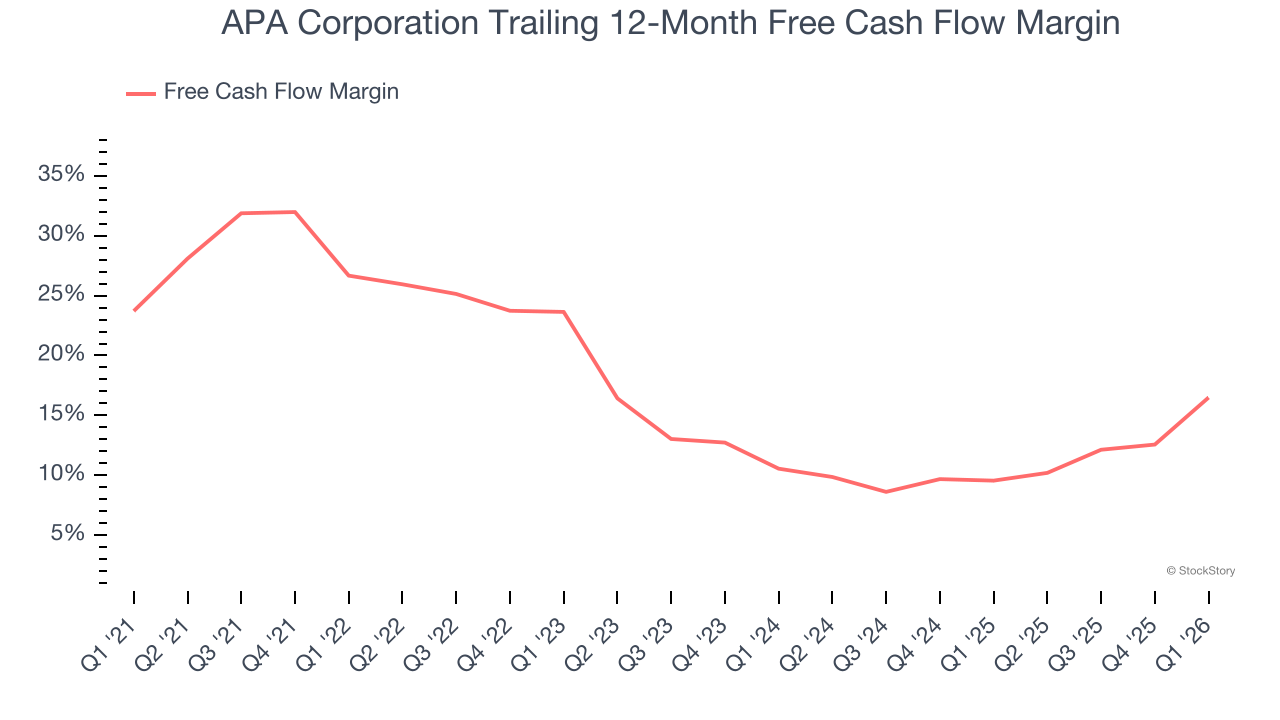

- Free Cash Flow Margin: 20.5%, up from 5.9% in the same quarter last year

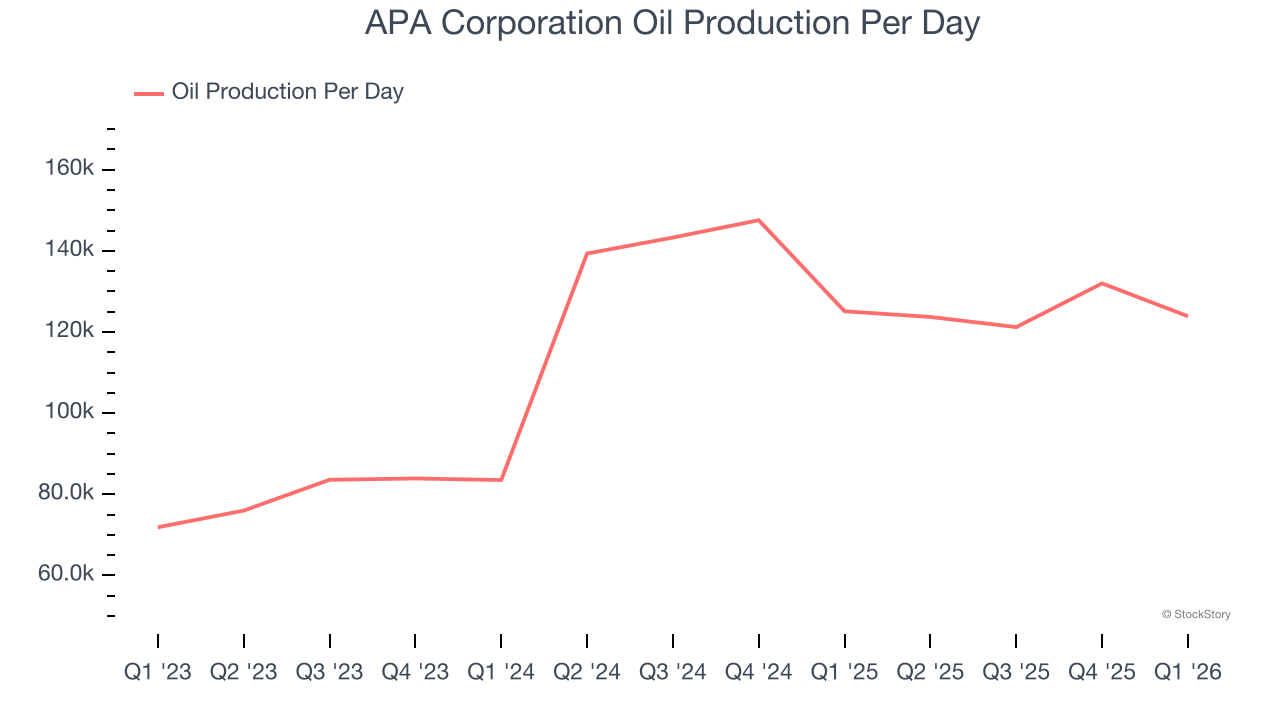

- Oil production per day: in line with the same quarter last year

- Market Capitalization: $14.66 billion

Company Overview

Operating in three continents with a history stretching back to 1954, APA Corporation (NASDAQ: APA) explores for, develops, and produces crude oil, natural gas, and natural gas liquids in the U.S., Egypt, and the U.K. North Sea.

Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Luckily, APA Corporation’s sales grew at a solid 13.9% compounded annual growth rate over the last five years. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers, a great starting point for our analysis.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. APA Corporation’s annualized revenue growth of 3.2% over the last ten years is below its five-year trend, but we still think the results suggest decent demand.

Revenue provides useful context, but it is heavily influenced by commodity prices and acquisitions. Production volumes, by contrast, reveal whether the underlying asset base is actually growing. Over the last two years, APA Corporation’s oil production per day averaged 30.3% year-on-year growth while its natural gas production per day averaged 3.6% year-on-year growth.

This quarter, APA Corporation reported year-on-year revenue growth of 8.8%, and its $2.33 billion of revenue exceeded Wall Street’s estimates by 12%. This quarter, APA Corporation’s Oil production per day fell by 1% year on year.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

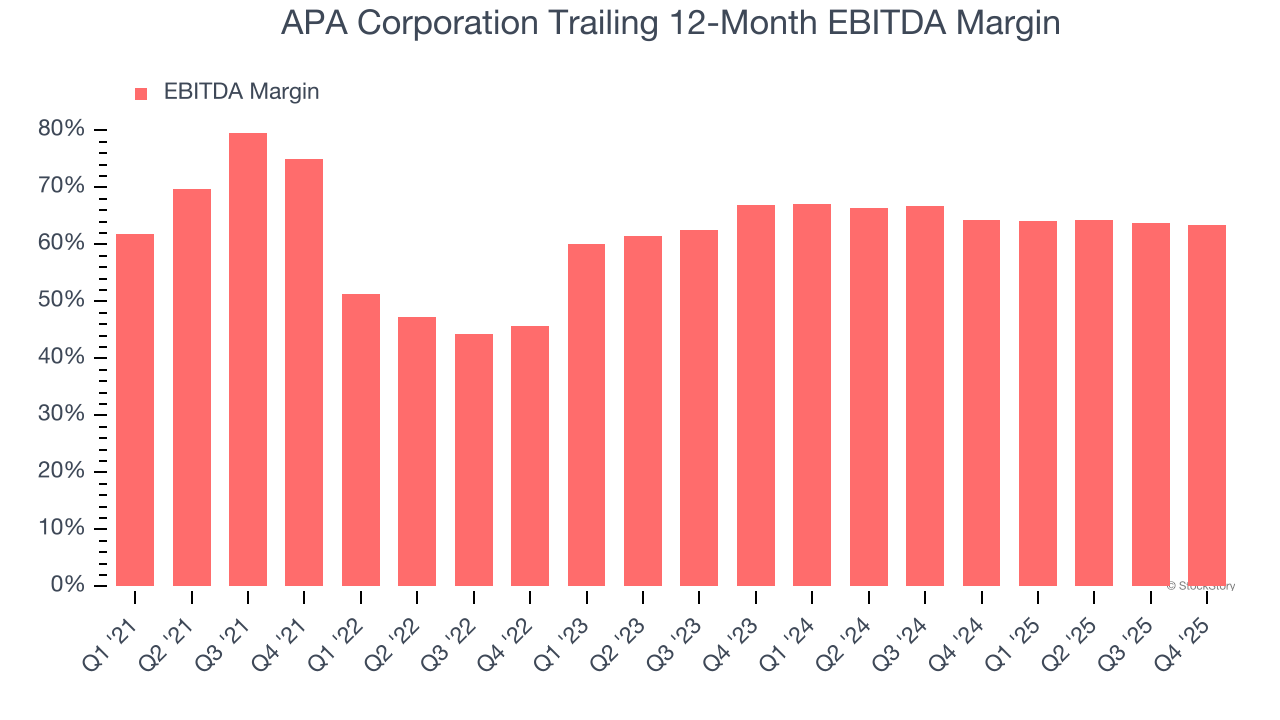

Adjusted EBITDA Margin

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

APA Corporation has been a well-oiled machine over the last five years. It demonstrated elite profitability for an upstream and integrated energy business, boasting an average EBITDA margin of 60.9%.

Looking at the trend in its profitability, APA Corporation’s EBITDA margin decreased by 10.8 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

Cash Is King

As mentioned above, adjusted EBITDA ignores capital structure and drilling expenditure decisions. These are two huge aspects of an Energy producer, so in order to understand a comprehensive picture of business quality, an investor needs to account for these. Said differently, adjusted EBITDA margins could be solid but free cash flow is abysmal because decline rates of the asset are extreme and the drilling is expensive. Free cash flow tells you about not only the economics of the production that has happened but how much it costs to stay in business as well (further drilling or extraction).

APA Corporation has shown robust cash profitability, driven by its attractive business model that enables it to reinvest or return capital to investors. The company’s free cash flow margin averaged 17.4% over the last five years, quite impressive for an upstream and integrated energy business.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

APA Corporation’s ratio of quarterly free cash flow volatility to WTI Crude price volatility over the past five years was 3.8 (lower is better), indicating unusually strong insulation from commodity swings. This stability supports superior capital access in downturns and positions APA Corporation to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of APA Corporation? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

APA Corporation’s free cash flow clocked in at $477 million in Q1, equivalent to a 20.5% margin. This result was good as its margin was 14.6 percentage points higher than in the same quarter last year. Its cash profitability was also above its five-year level, and we hope the company can build on this trend.

Key Takeaways from APA Corporation’s Q1 Results

It was good to see APA Corporation beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock remained flat at $38.23 immediately following the results.

So do we think APA Corporation is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).