Aviation and fleet aftermarket services provider VSE Corporation (NASDAQ: VSEC) announced better-than-expected revenue in Q1 CY2026, with sales up 26.8% year on year to $324.6 million. Its non-GAAP profit of $1.17 per share was 30.7% above analysts’ consensus estimates.

Is now the time to buy VSE Corporation? Find out by accessing our full research report, it’s free.

VSE Corporation (VSEC) Q1 CY2026 Highlights:

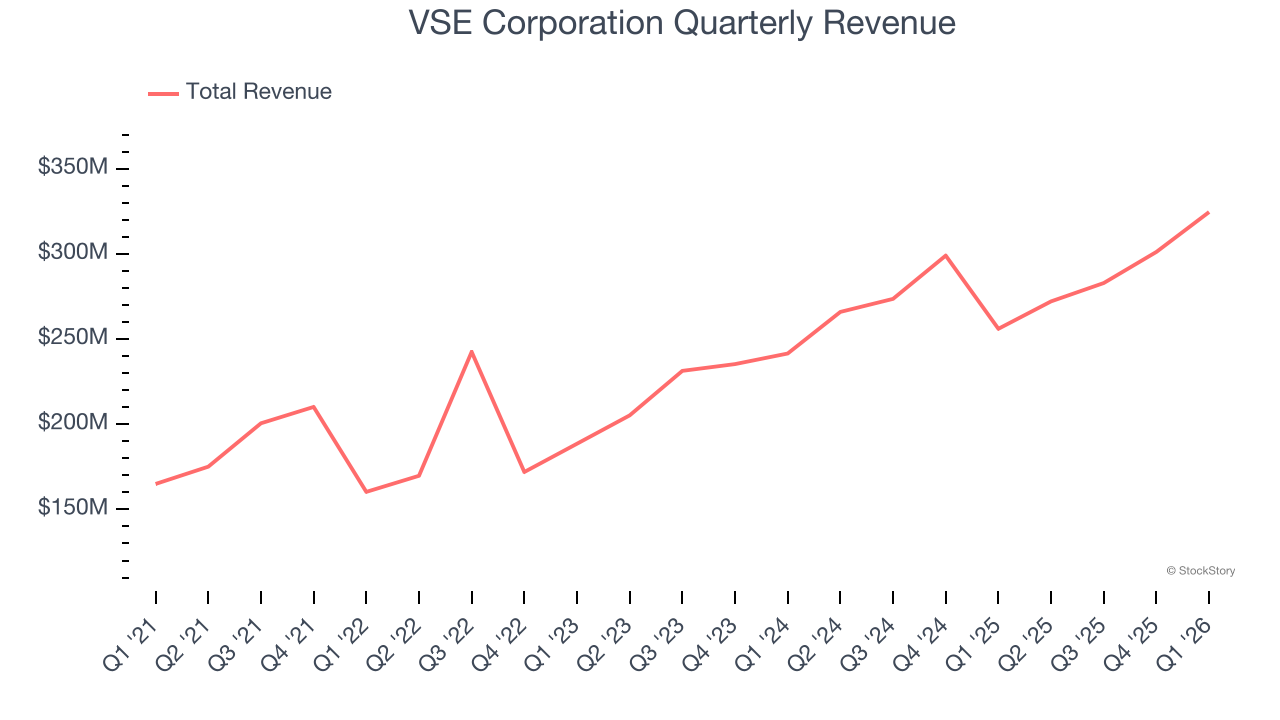

- Revenue: $324.6 million vs analyst estimates of $312.7 million (26.8% year-on-year growth, 3.8% beat)

- Adjusted EPS: $1.17 vs analyst estimates of $0.90 (30.7% beat)

- Adjusted EBITDA: $55.43 million vs analyst estimates of $51.23 million (17.1% margin, 8.2% beat)

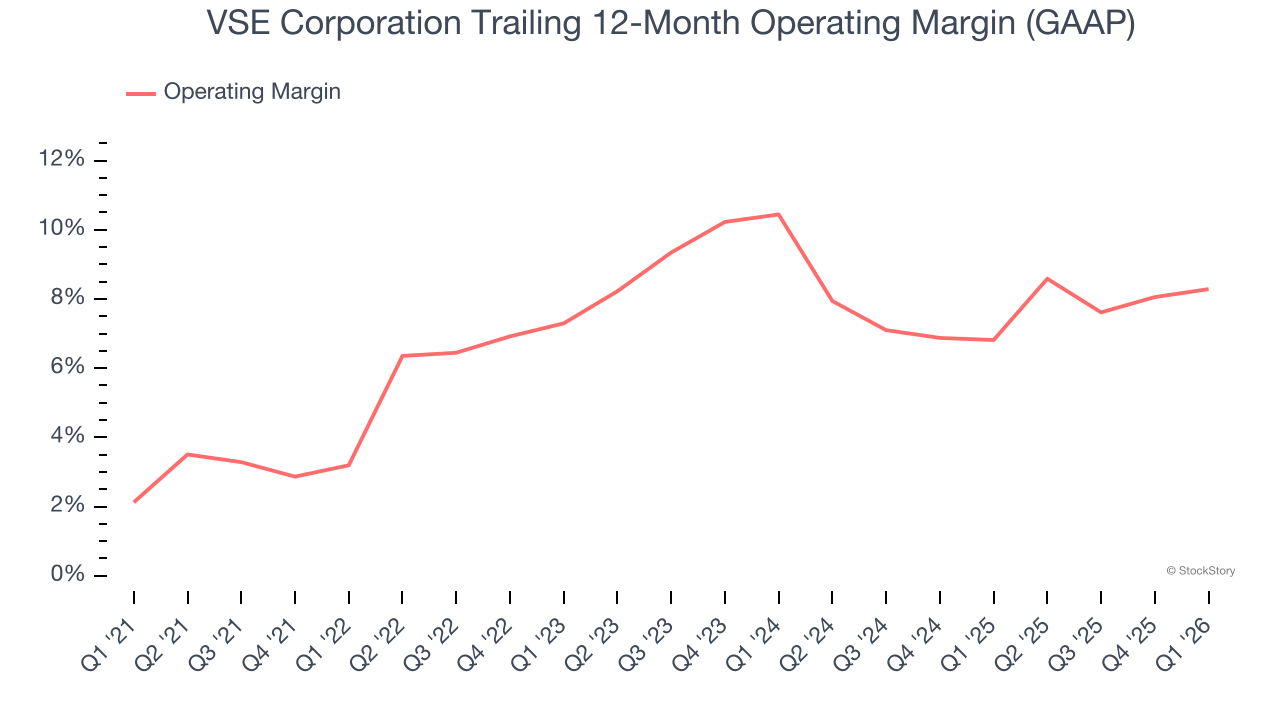

- Operating Margin: 10.1%, in line with the same quarter last year

- Free Cash Flow was -$68.72 million compared to -$49.51 million in the same quarter last year

- Market Capitalization: $4.72 billion

Company Overview

With roots dating back to 1959 and a strategic focus on extending the life of transportation assets, VSE Corporation (NASDAQ: VSEC) provides aftermarket parts distribution and maintenance, repair, and overhaul services for aircraft and vehicle fleets in commercial and government markets.

Revenue Growth

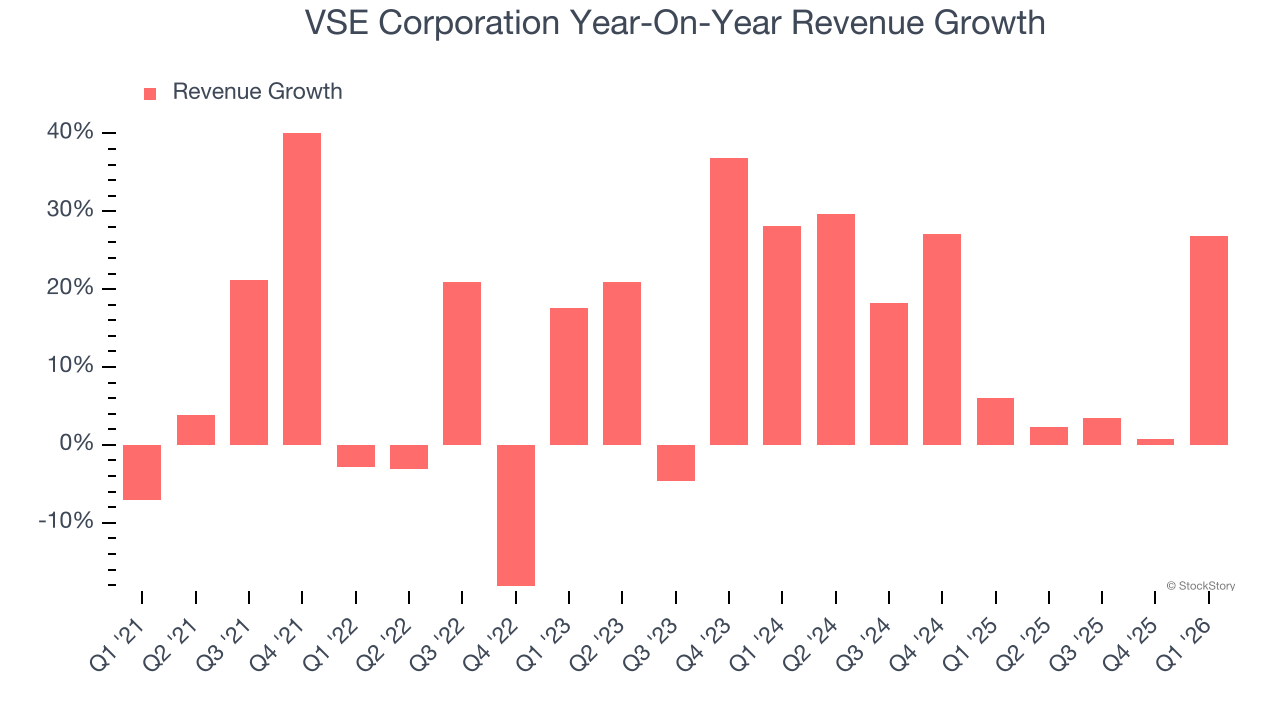

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, VSE Corporation’s sales grew at an excellent 12.7% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. VSE Corporation’s annualized revenue growth of 13.7% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, VSE Corporation reported robust year-on-year revenue growth of 26.8%, and its $324.6 million of revenue topped Wall Street estimates by 3.8%.

Looking ahead, sell-side analysts expect revenue to grow 58.9% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will catalyze better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

VSE Corporation was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, VSE Corporation’s operating margin rose by 5.1 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, VSE Corporation generated an operating margin profit margin of 10.1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

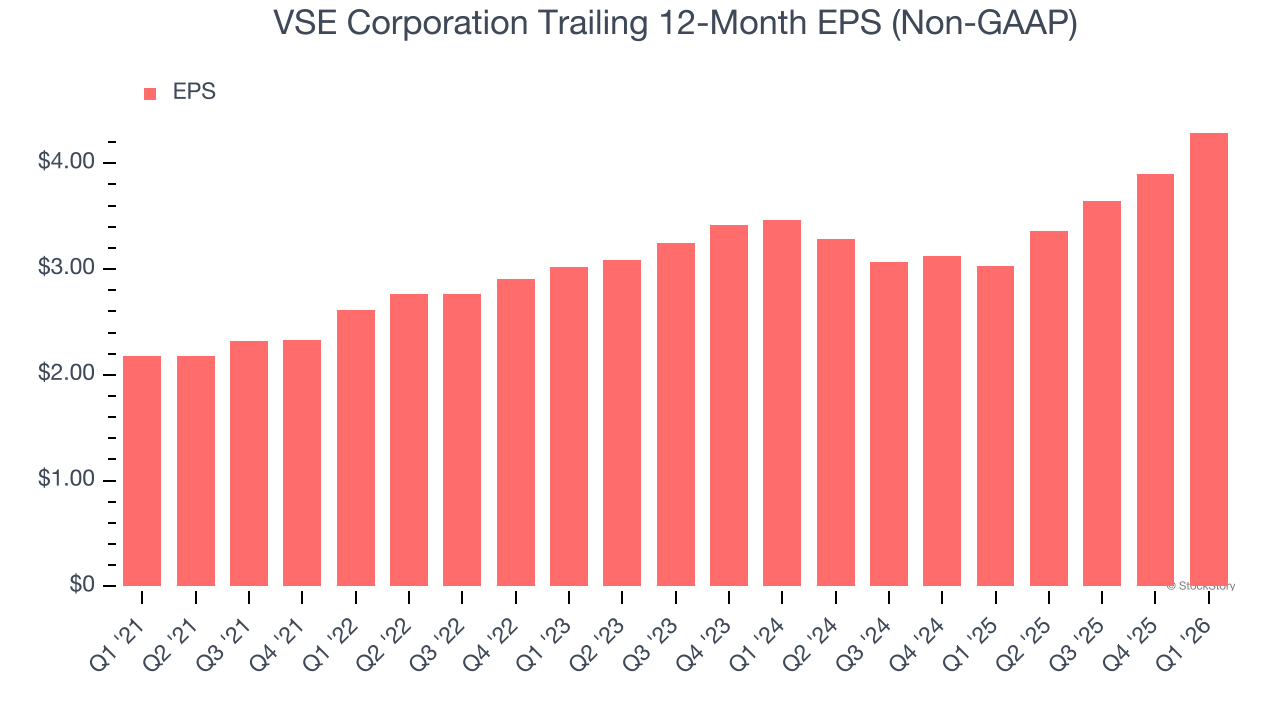

VSE Corporation’s remarkable 14.5% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Although it performed well, VSE Corporation’s two-year annual EPS growth of 11.4% lower than its 13.7% two-year revenue growth.

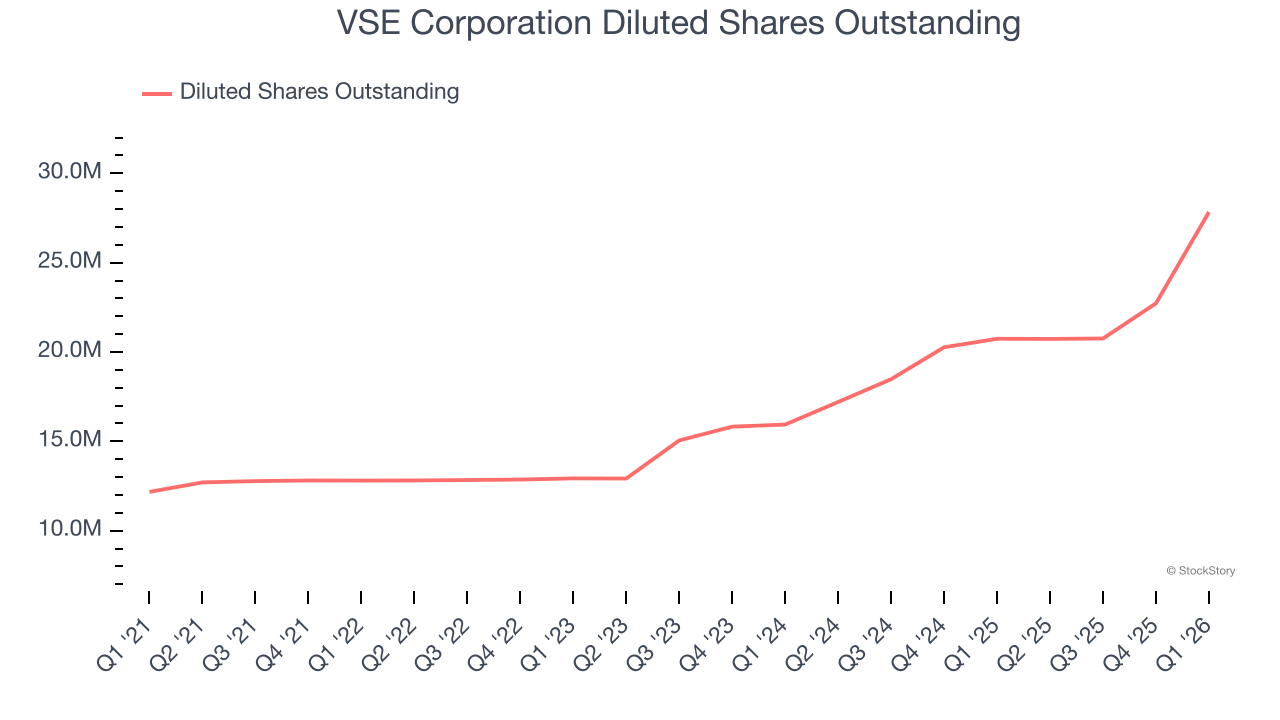

We can take a deeper look into VSE Corporation’s earnings to better understand the drivers of its performance. A two-year view shows VSE Corporation has diluted its shareholders, growing its share count by 74.6%. This has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q1, VSE Corporation reported adjusted EPS of $1.17, up from $0.78 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects VSE Corporation’s full-year EPS of $4.29 to grow 13.8%.

Key Takeaways from VSE Corporation’s Q1 Results

It was good to see VSE Corporation beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 5.1% to $186.88 immediately following the results.

Sure, VSE Corporation had a solid quarter, but if we look at the bigger picture, is this stock a buy? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).