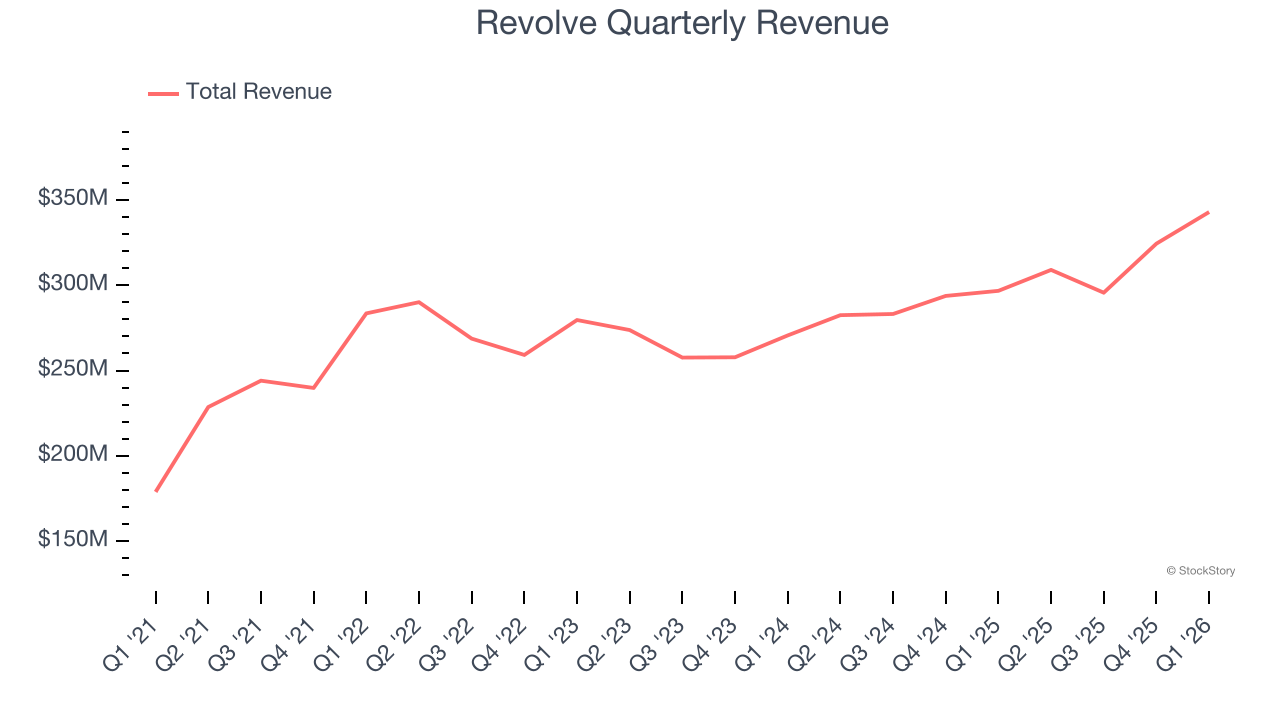

Online fashion retailer Revolve (NYSE: RVLV) announced better-than-expected revenue in Q1 CY2026, with sales up 15.6% year on year to $342.9 million. Its GAAP profit of $0.20 per share was 7.1% above analysts’ consensus estimates.

Is now the time to buy Revolve? Find out by accessing our full research report, it’s free.

Revolve (RVLV) Q1 CY2026 Highlights:

- Revenue: $342.9 million vs analyst estimates of $329 million (15.6% year-on-year growth, 4.2% beat)

- EPS (GAAP): $0.20 vs analyst estimates of $0.19 (7.1% beat)

- Adjusted EBITDA: $21.06 million vs analyst estimates of $20.88 million (6.1% margin, 0.9% beat)

- Operating Margin: 4.6%, in line with the same quarter last year

- Free Cash Flow was $44.9 million, up from -$13.29 million in the previous quarter

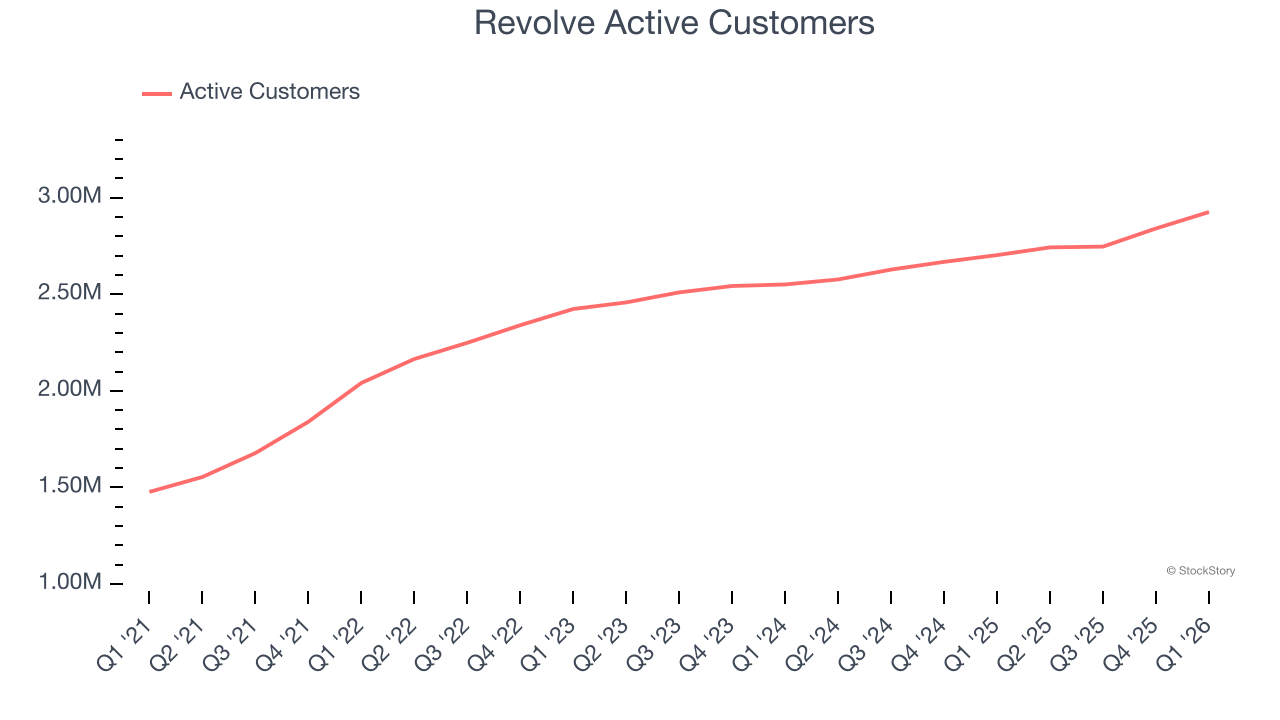

- Active Customers : 2.93 million, up 223,000 year on year

- Market Capitalization: $1.68 billion

"Outstanding execution by our team within a dynamic operating environment led to strong first quarter results and continued market share gains, highlighted by our net sales increasing 16% year-over-year, earnings per share increasing 25% year-over-year, and $49 million in operating cash flow that significantly strengthened our pristine balance sheet," said co-founder and co-CEO Mike Karanikolas.

Company Overview

Launched in 2003 by software engineers Michael Mente and Mike Karanikolas, Revolve (NASDAQ: NYSE) is a fashion retailer leveraging social media and a community of fashion influencers to drive its merchandising strategy.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Revolve grew its sales at a sluggish 5% compounded annual growth rate. This was below our standard for the consumer internet sector and is a poor baseline for our analysis.

This quarter, Revolve reported year-on-year revenue growth of 15.6%, and its $342.9 million of revenue exceeded Wall Street’s estimates by 4.2%.

Looking ahead, sell-side analysts expect revenue to grow 6.6% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Active Customers

Buyer Growth

As an online retailer, Revolve generates revenue growth by expanding its number of users and the average order size in dollars.

Over the last two years, Revolve’s active customers , a key performance metric for the company, increased by 5.8% annually to 2.93 million in the latest quarter. This growth rate lags behind the hottest consumer internet applications. If Revolve wants to accelerate growth, it likely needs to engage users more effectively with its existing offerings or innovate with new products.

In Q1, Revolve added 223,000 active customers , leading to 8.3% year-on-year growth. The quarterly print was higher than its two-year result, suggesting its new initiatives are accelerating buyer growth.

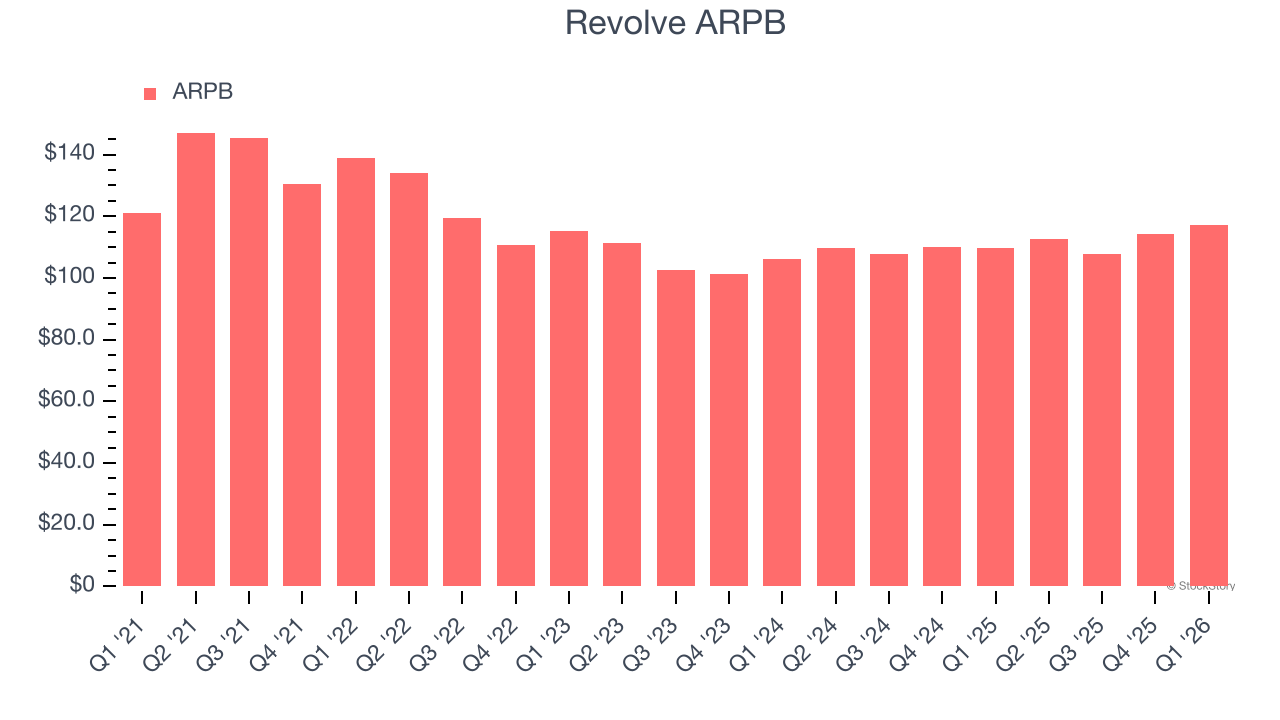

Revenue Per Buyer

Average revenue per buyer (ARPB) is a critical metric to track because it measures how much customers spend per order.

Revolve’s ARPB growth has been mediocre over the last two years, averaging 3.6%. This isn’t great when combined with its weaker active customers performance. If Revolve tries boosting ARPB by taking a more aggressive approach to monetization, it’s unclear whether buyer growth would be sustainable.

This quarter, Revolve’s ARPB clocked in at $117.18. It grew by 6.8% year on year, slower than its buyer growth.

Key Takeaways from Revolve’s Q1 Results

It was encouraging to see Revolve beat analysts’ revenue expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 2.6% to $22.82 immediately following the results.

So do we think Revolve is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).