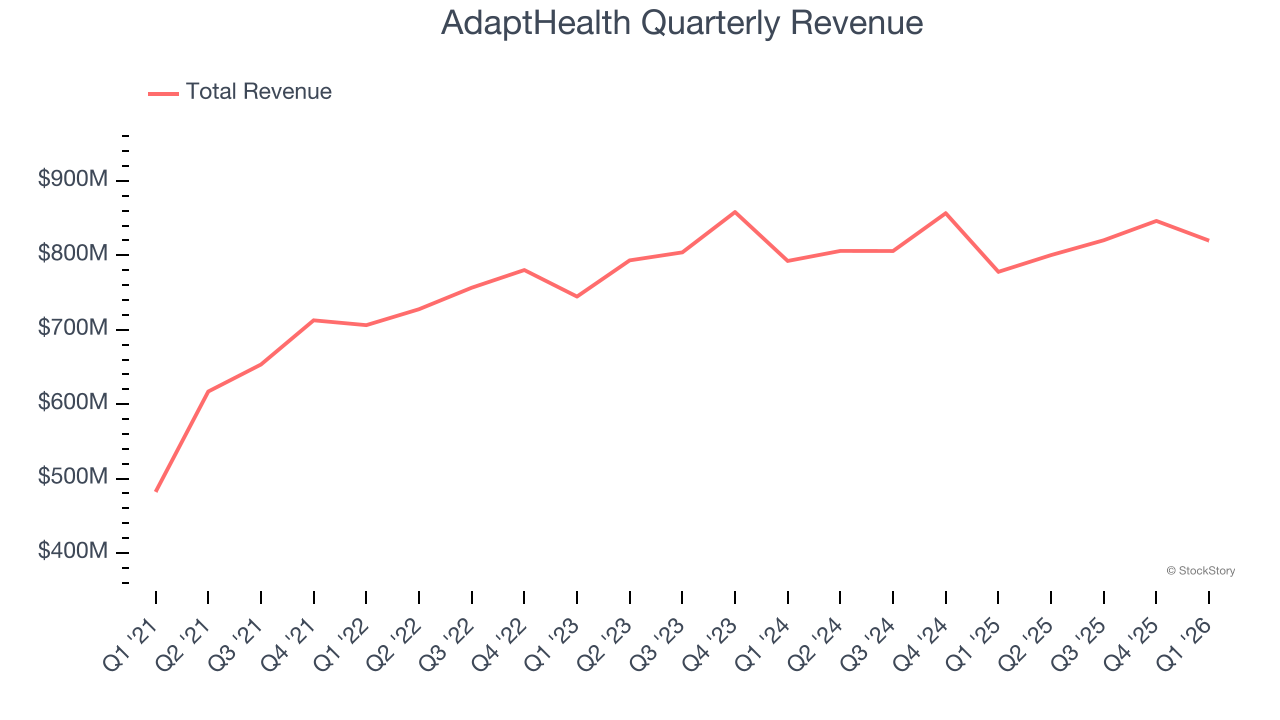

Healthcare services provider AdaptHealth Corp. (NASDAQ: AHCO) reported revenue ahead of Wall Street’s expectations in Q1 CY2026, with sales up 5.4% year on year to $819.8 million. The company expects the full year’s revenue to be around $3.49 billion, close to analysts’ estimates. Its GAAP loss of $0.12 per share was significantly below analysts’ consensus estimates.

Is now the time to buy AdaptHealth? Find out by accessing our full research report, it’s free.

AdaptHealth (AHCO) Q1 CY2026 Highlights:

- Revenue: $819.8 million vs analyst estimates of $797 million (5.4% year-on-year growth, 2.9% beat)

- EPS (GAAP): -$0.12 vs analyst estimates of -$0.01 (significant miss)

- Adjusted EBITDA: $121.2 million vs analyst estimates of $127.4 million (14.8% margin, 4.9% miss)

- The company slightly lifted its revenue guidance for the full year to $3.49 billion at the midpoint from $3.48 billion

- EBITDA guidance for the full year is $705 million at the midpoint, in line with analyst expectations

- Operating Margin: 0.7%, down from 3% in the same quarter last year

- Free Cash Flow was -$27.49 million compared to -$58,000 in the same quarter last year

- Market Capitalization: $1.77 billion

“The opening months of 2026 have set the stage for what will be a defining year for AdaptHealth,” said Suzanne Foster, Chief Executive Officer.

Company Overview

With a network of approximately 680 locations serving patients across all 50 states, AdaptHealth (NASDAQ: AHCO) provides home medical equipment, supplies, and related services to patients with chronic conditions like sleep apnea, diabetes, and respiratory disorders.

Revenue Growth

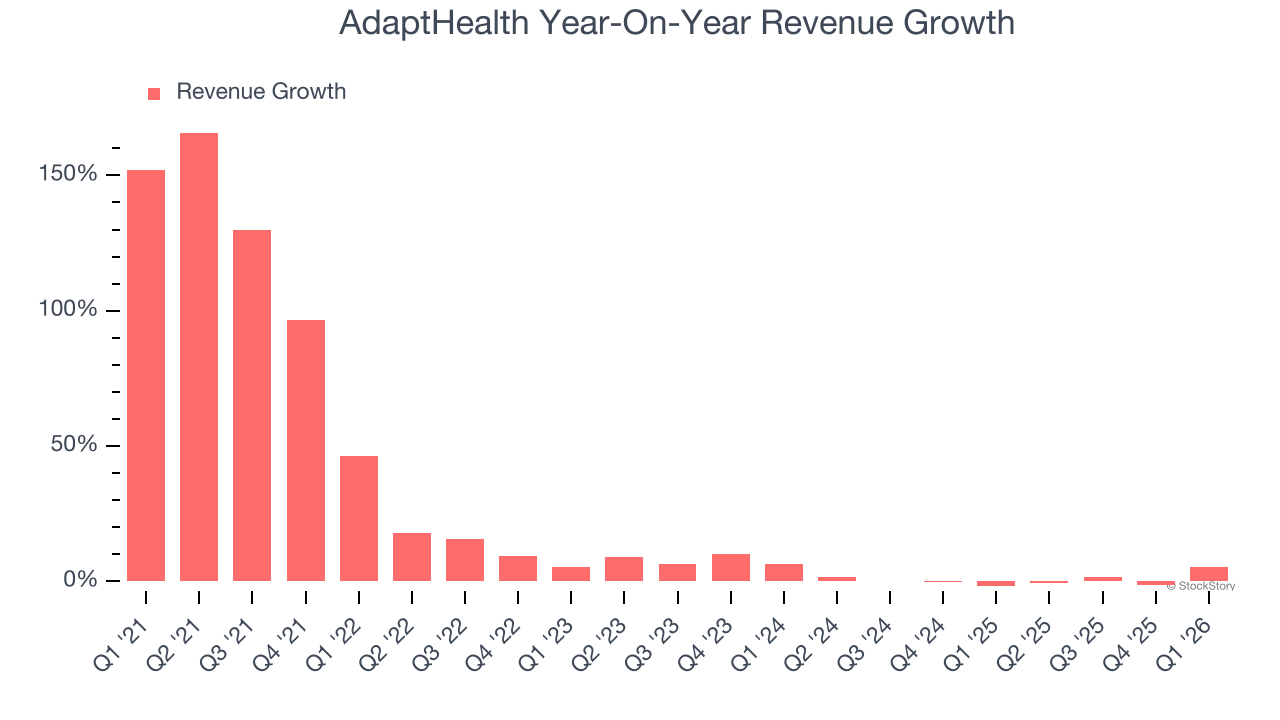

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, AdaptHealth grew its sales at an impressive 19.3% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. AdaptHealth’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years.

This quarter, AdaptHealth reported year-on-year revenue growth of 5.4%, and its $819.8 million of revenue exceeded Wall Street’s estimates by 2.9%.

Looking ahead, sell-side analysts expect revenue to grow 7.8% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and implies its newer products and services will spur better top-line performance.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

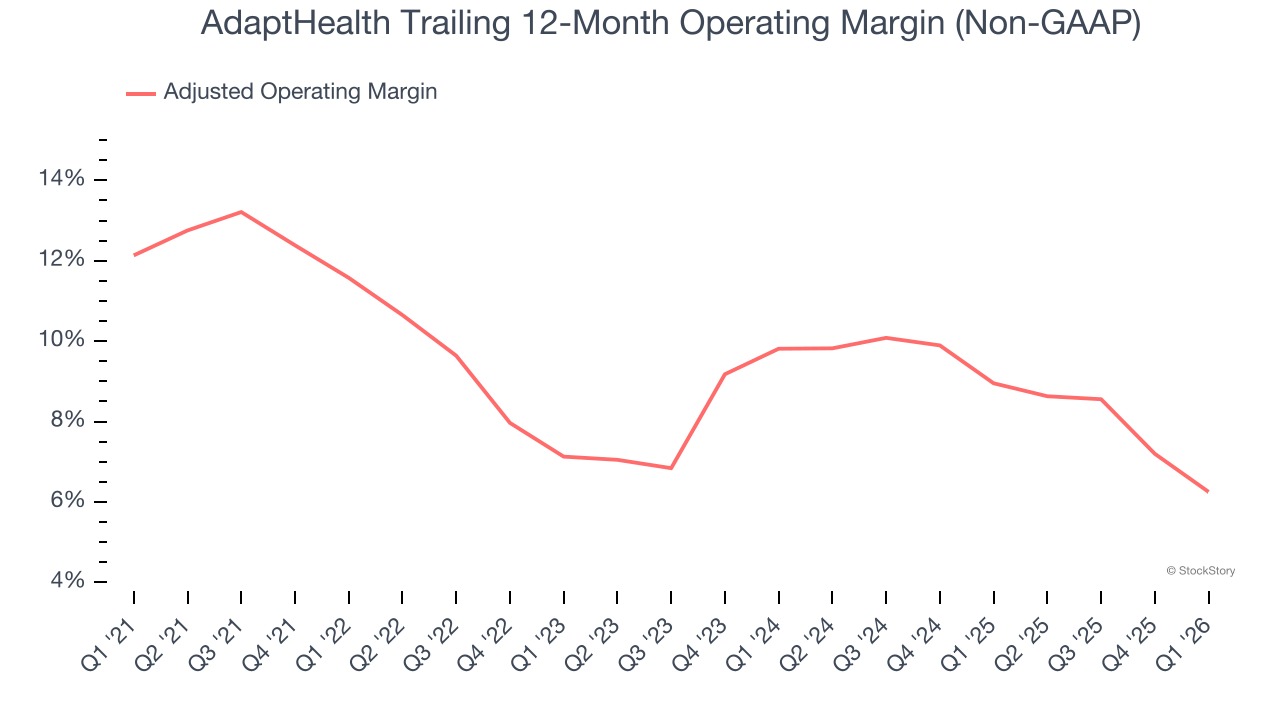

Adjusted Operating Margin

Adjusted operating margin is a key measure of profitability. Think of it as net income (the bottom line) excluding the impact of non-recurring expenses, taxes, and interest on debt - metrics less connected to business fundamentals.

AdaptHealth was profitable over the last five years but held back by its large cost base. Its average adjusted operating margin of 8.7% was weak for a healthcare business.

Looking at the trend in its profitability, AdaptHealth’s adjusted operating margin decreased by 5.3 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.6 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q1, AdaptHealth’s breakeven margin was 0.7%, down 3.6 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

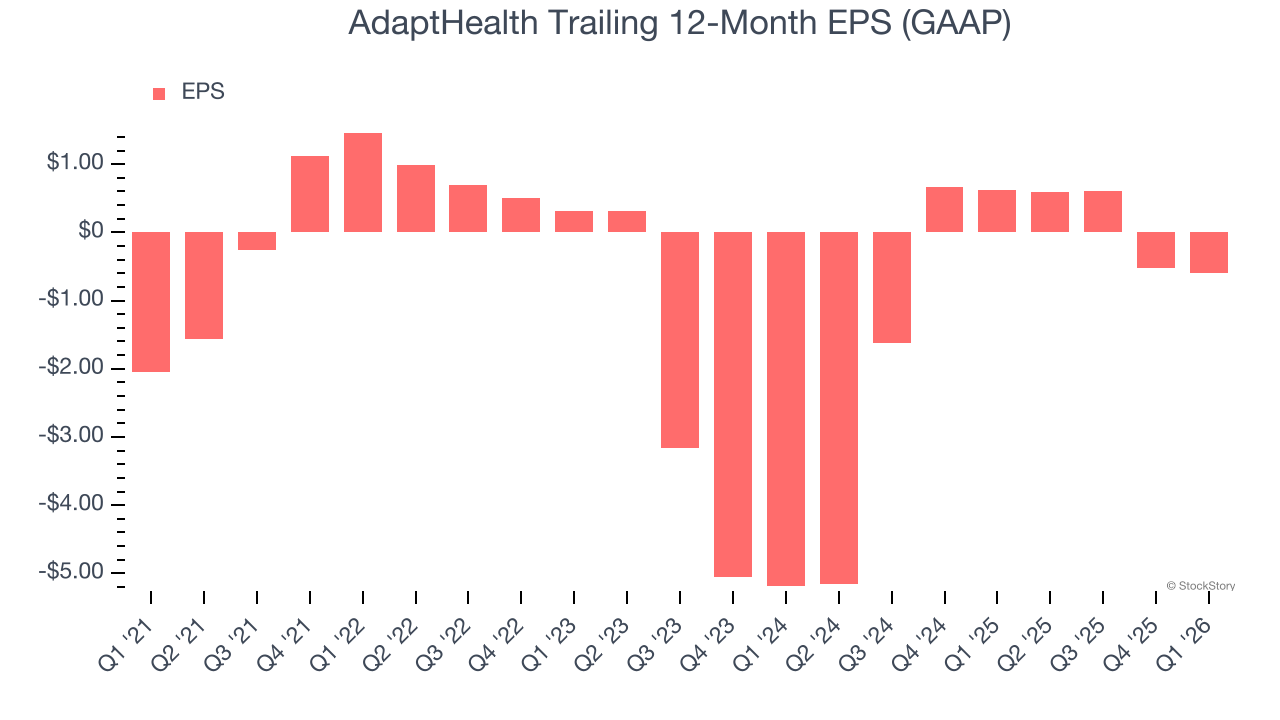

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although AdaptHealth’s full-year earnings are still negative, it reduced its losses and improved its EPS by 22% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q1, AdaptHealth reported EPS of negative $0.12, down from negative $0.05 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast AdaptHealth’s full-year EPS of negative $0.59 will flip to positive $0.97.

Key Takeaways from AdaptHealth’s Q1 Results

We enjoyed seeing AdaptHealth beat analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance was in line with Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 2.8% to $12.69 immediately after reporting.

Big picture, is AdaptHealth a buy here and now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).