CSG currently trades at $80.34 per share and has shown little upside over the past six months, posting a middling return of 2.6%.

Is now the time to buy CSG, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is CSG Not Exciting?

We don't have much confidence in CSG. Here are three reasons why CSGS doesn't excite us and a stock we'd rather own.

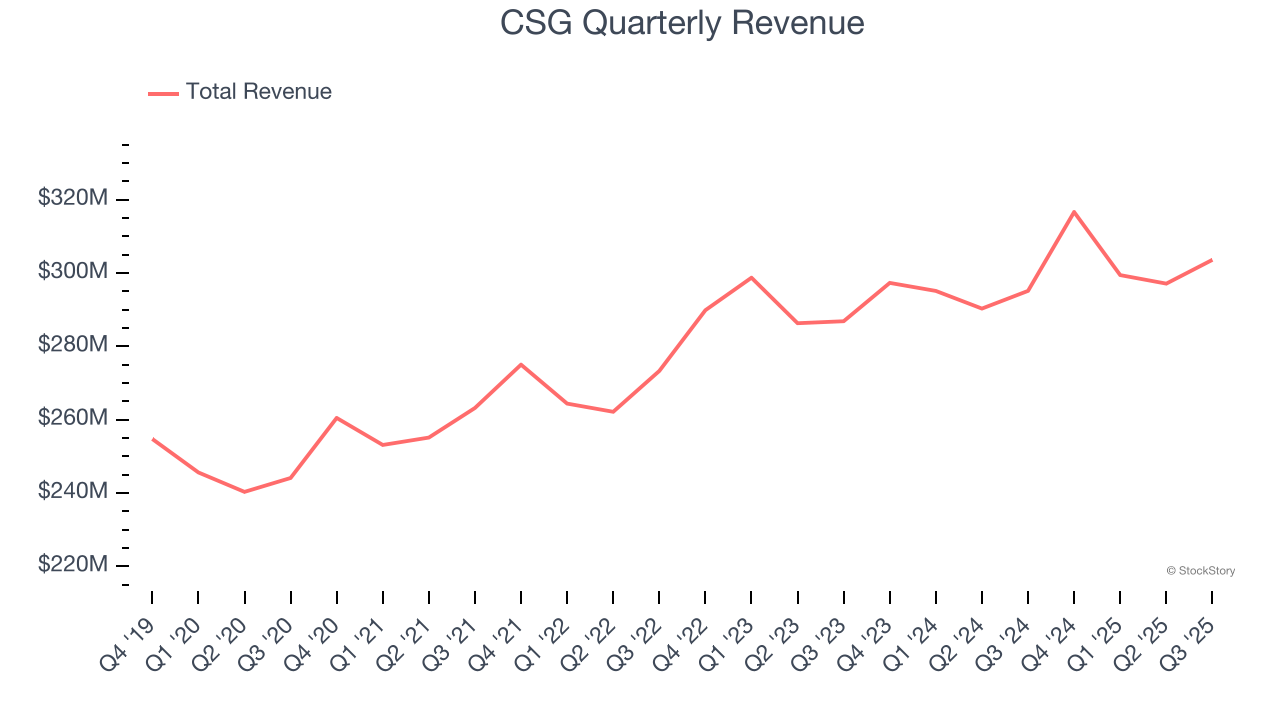

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, CSG’s sales grew at a mediocre 4.3% compounded annual growth rate over the last five years. This fell short of our benchmark for the business services sector.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect CSG’s revenue to stall, a slight deceleration versus its 4.3% annualized growth for the past five years. This projection is underwhelming and suggests its products and services will face some demand challenges.

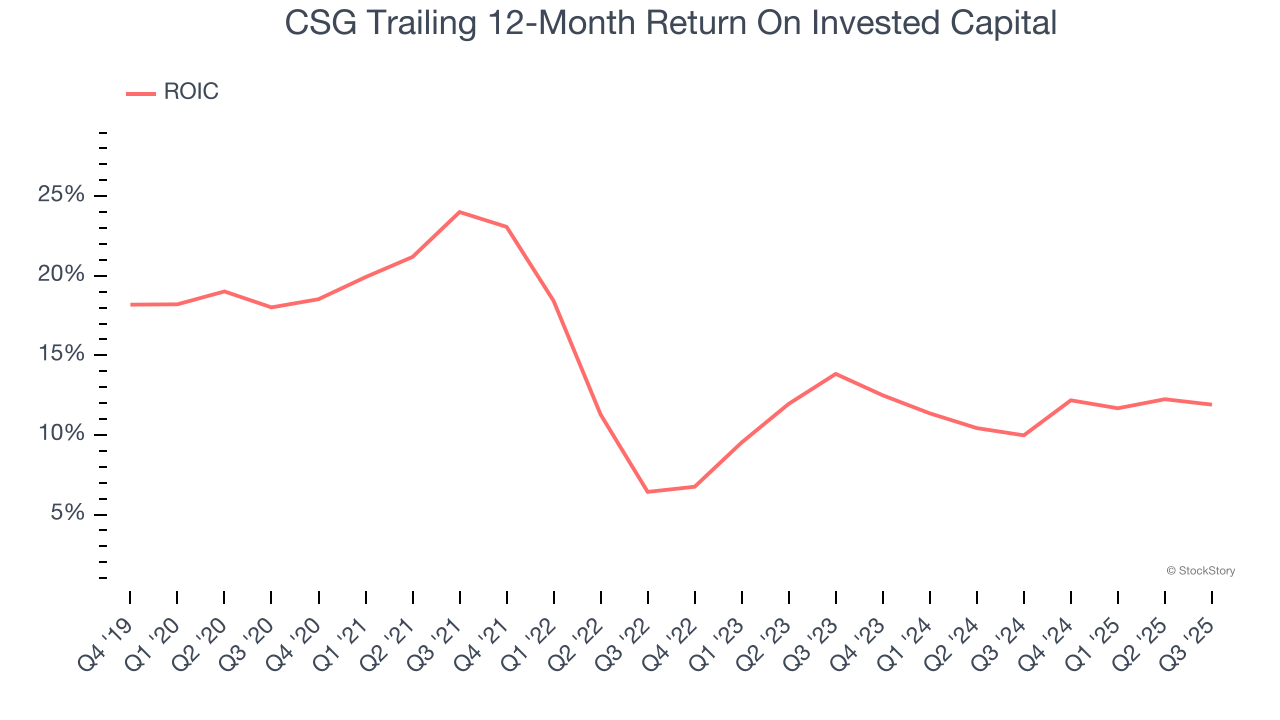

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, CSG’s ROIC averaged 4.3 percentage point decreases each year over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

CSG’s business quality ultimately falls short of our standards. That said, the stock currently trades at 16.5× forward P/E (or $80.34 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d suggest looking at the Amazon and PayPal of Latin America.

Stocks We Like More Than CSG

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.