Bedding manufacturer and retailer Sleep Number (NASDAQ: SNBR) missed Wall Street’s revenue expectations in Q1 CY2026, with sales falling 18.9% year on year to $319 million. Its GAAP loss of $2.19 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Sleep Number? Find out by accessing our full research report, it’s free.

Sleep Number (SNBR) Q1 CY2026 Highlights:

- "Q1 came in as expected given the soft start to the year, but year-over-year demand improved steadily throughout the quarter, ending with growth in March over last year"

- "We believe this [new product launches, refreshed marketing], combined with the full realization of our cost savings actions, puts us in line with the financial indications we highlighted in the previous earnings call"

- Revenue: $319 million vs analyst estimates of $320.7 million (18.9% year-on-year decline, 0.5% miss)

- EPS (GAAP): -$2.19 vs analyst estimates of -$0.47 (significant miss)

- Adjusted EBITDA: $5.75 million vs analyst estimates of $11.35 million (1.8% margin, 49.3% miss)

- Operating Margin: -11.6%, down from 0.5% in the same quarter last year

- Free Cash Flow was -$13.19 million compared to -$7.23 million in the same quarter last year

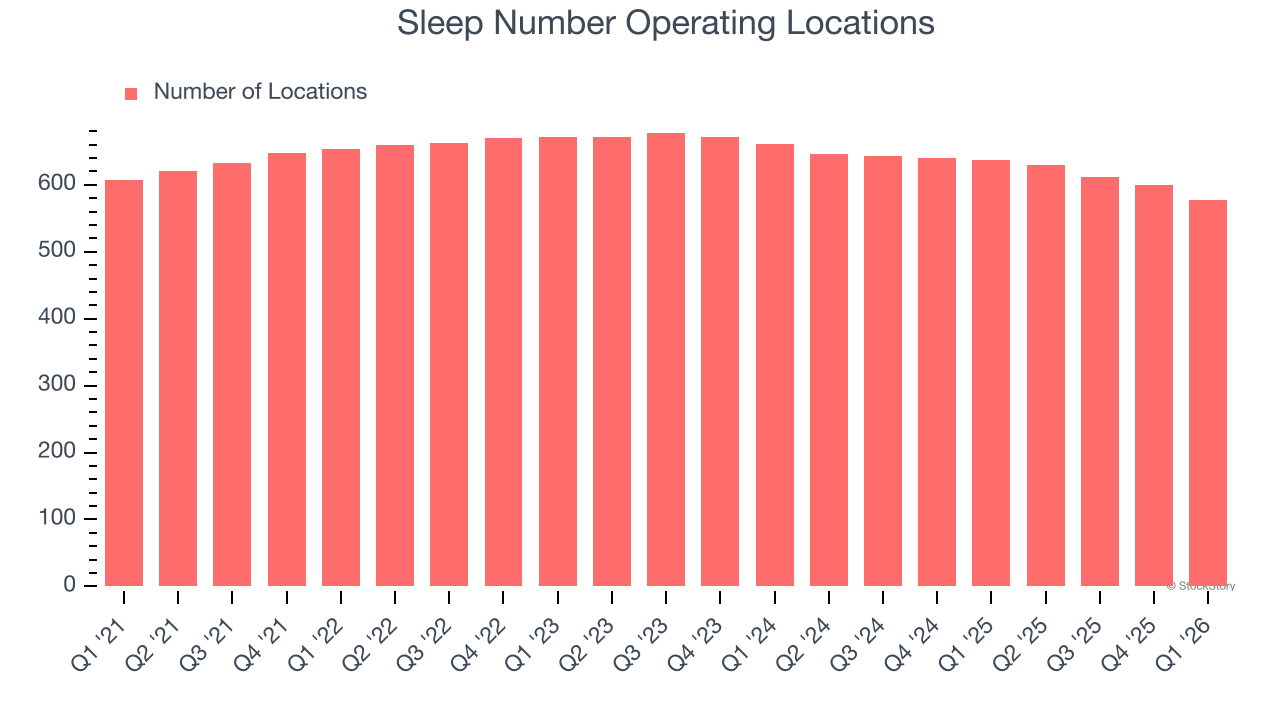

- Locations: 577 at quarter end, down from 637 in the same quarter last year

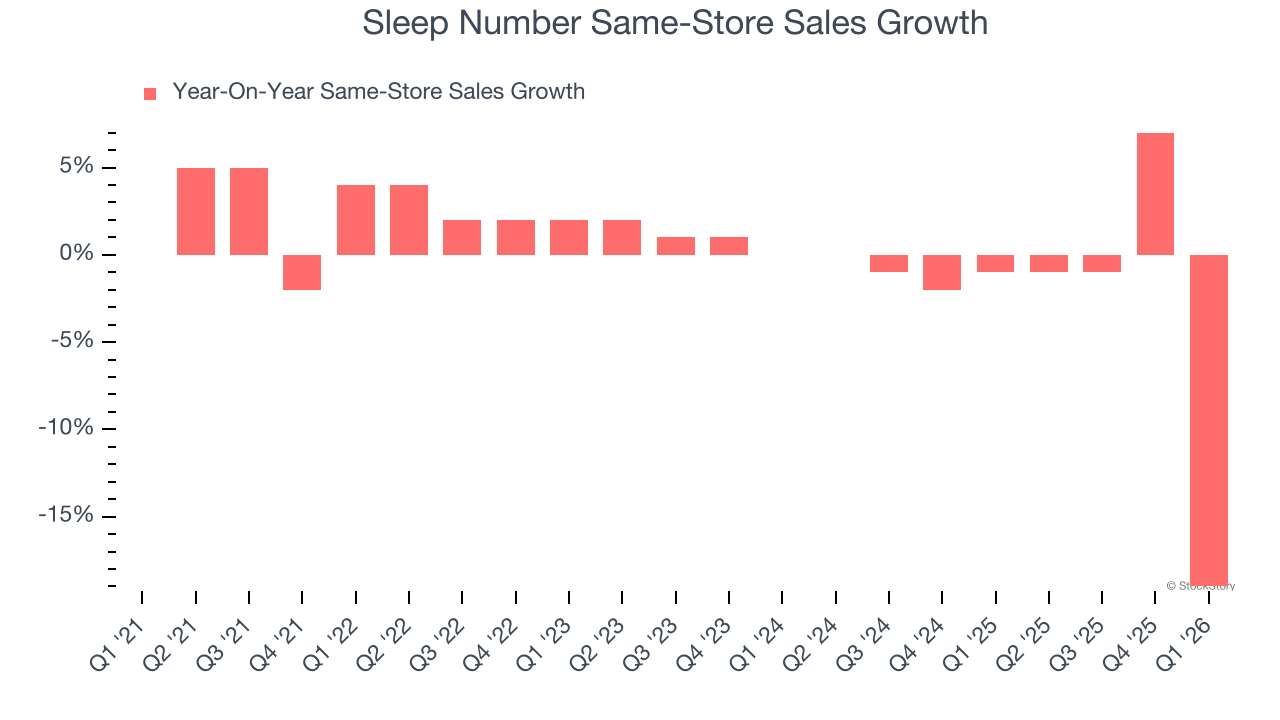

- Same-Store Sales fell 19% year on year (-1% in the same quarter last year)

- Market Capitalization: $56.45 million

Company Overview

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ: SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.34 billion in revenue over the past 12 months, Sleep Number is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Sleep Number’s demand was weak over the last three years. Its sales fell by 14.2% annually as it closed stores and observed lower sales at existing, established locations.

This quarter, Sleep Number missed Wall Street’s estimates and reported a rather uninspiring 18.9% year-on-year revenue decline, generating $319 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months, an acceleration versus the last three years. This projection is noteworthy and implies its newer products will catalyze better top-line performance.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Sleep Number listed 577 locations in the latest quarter and has generally closed its stores over the last two years, averaging 5.1% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Sleep Number’s demand has been shrinking over the last two years as its same-store sales have averaged 2.3% annual declines. This performance isn’t ideal, and Sleep Number is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Sleep Number’s same-store sales fell by 19% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

Key Takeaways from Sleep Number’s Q1 Results

The results were not good, but management commentary was positive. Revenue missed slightly on negative same-store sales. However, management mentioned that new product launches and refreshed marketing, "combined with the full realization of our cost savings actions, puts us in line with the financial indications we highlighted in the previous earnings call." Overall, the numbers weren't great, but it seems like there has been sequential improvement in the business as of late. The stock traded up 2.2% to $2.51 immediately after reporting.

So do we think Sleep Number is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).