Cable news and media network Fox (NASDAQ: FOXA) reported Q1 CY2026 results exceeding the market’s revenue expectations, but sales fell by 8.6% year on year to $3.99 billion. Its non-GAAP profit of $1.32 per share was 36.4% above analysts’ consensus estimates.

Is now the time to buy FOX? Find out by accessing our full research report, it’s free.

FOX (FOXA) Q1 CY2026 Highlights:

- Revenue: $3.99 billion vs analyst estimates of $3.81 billion (8.6% year-on-year decline, 4.7% beat)

- Adjusted EPS: $1.32 vs analyst estimates of $0.97 (36.4% beat)

- Adjusted EBITDA: $954 million vs analyst estimates of $741.9 million (23.9% margin, 28.6% beat)

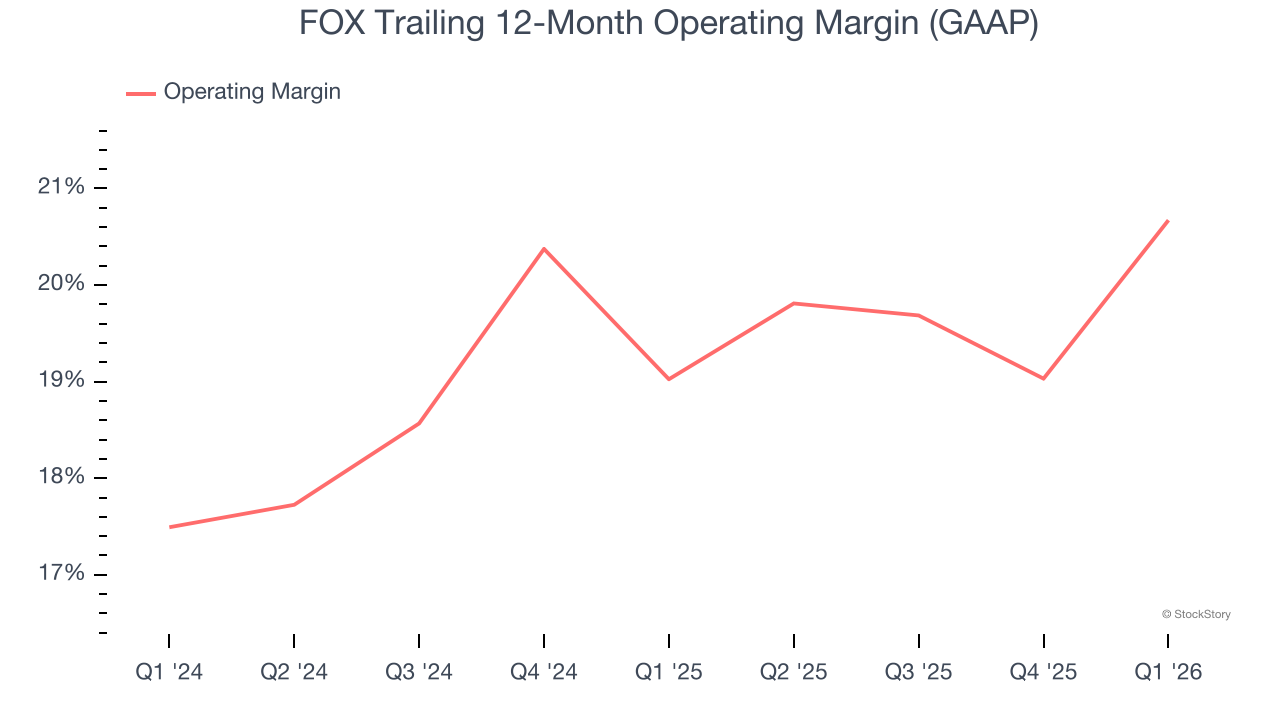

- Operating Margin: 23.9%, up from 17.4% in the same quarter last year

- Free Cash Flow Margin: 44.2%, similar to the same quarter last year

- Market Capitalization: $25.35 billion

Company Overview

Founded in 1915, Fox (NASDAQ: FOXA) is a diversified media company, operating prominent cable news, television broadcasting, and digital media platforms.

Revenue Growth

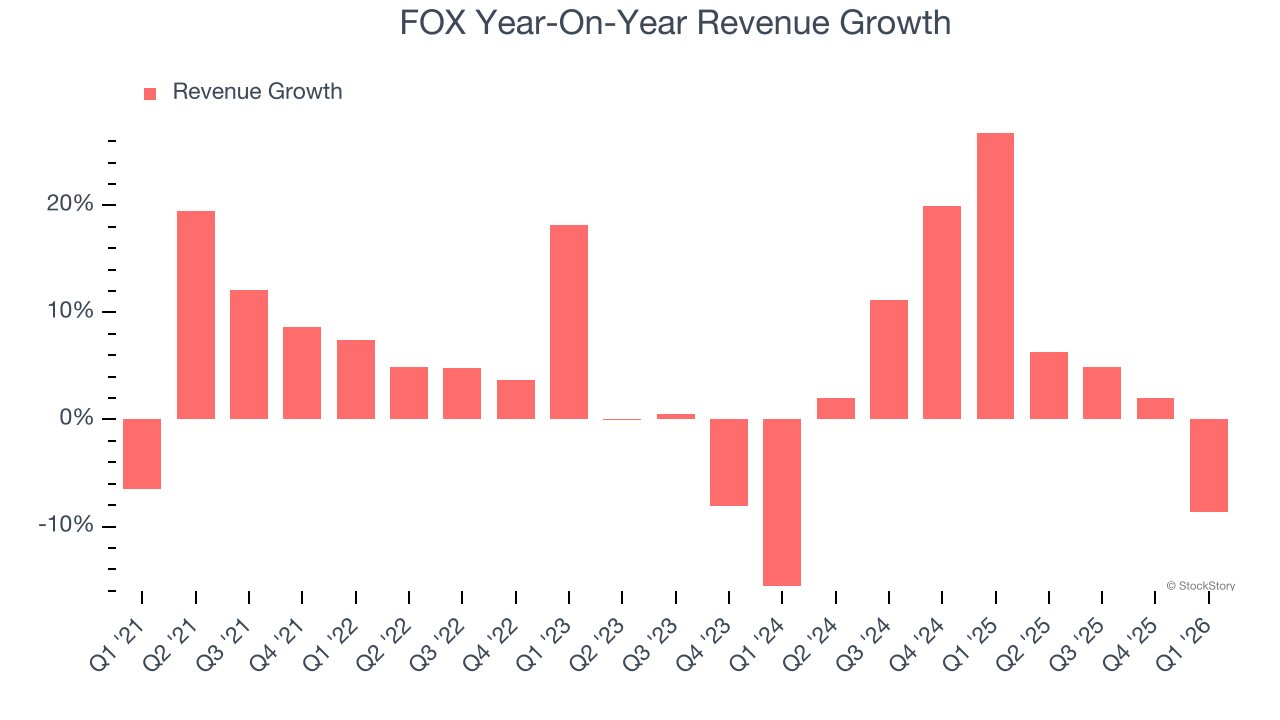

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, FOX’s sales grew at a weak 5.4% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. FOX’s annualized revenue growth of 7.9% over the last two years is above its five-year trend, which is encouraging.

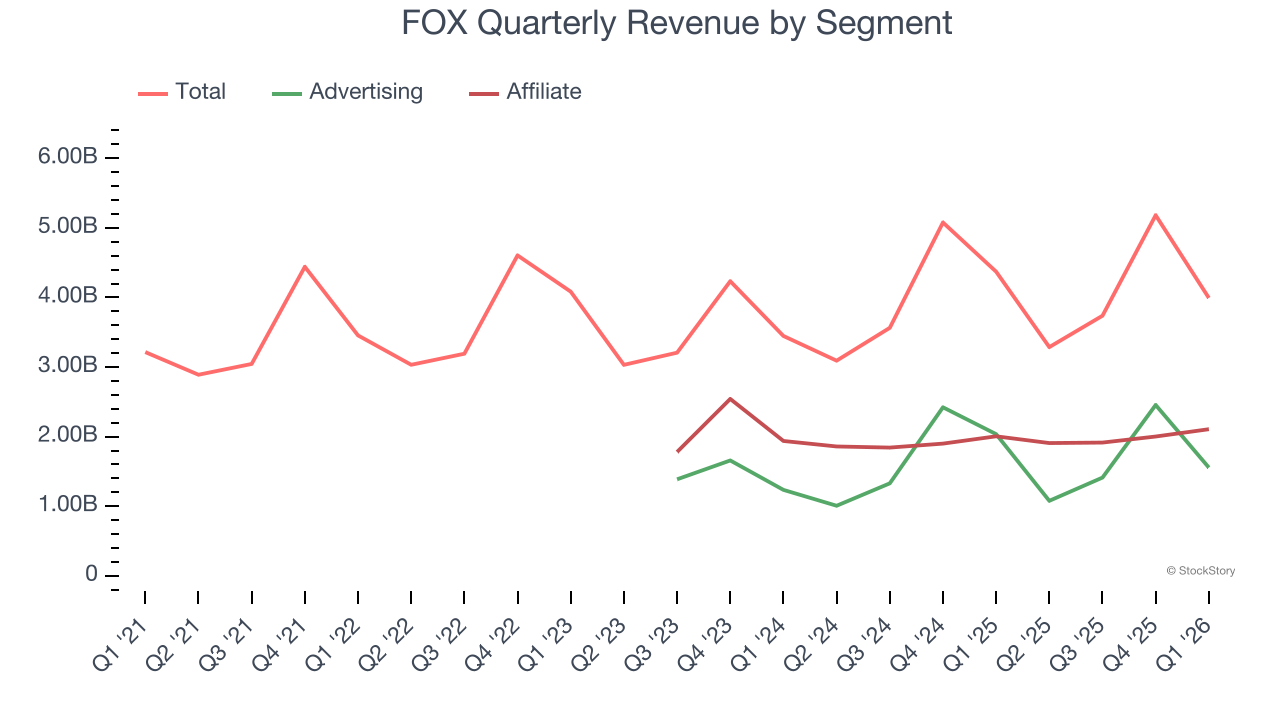

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Advertising and Affiliate, which are 39% and 52.8% of revenue. Over the last two years, FOX’s Advertising revenue (marketing services) averaged 14% year-on-year growth while its Affiliate revenue (licensing and retransmission fees) was flat.

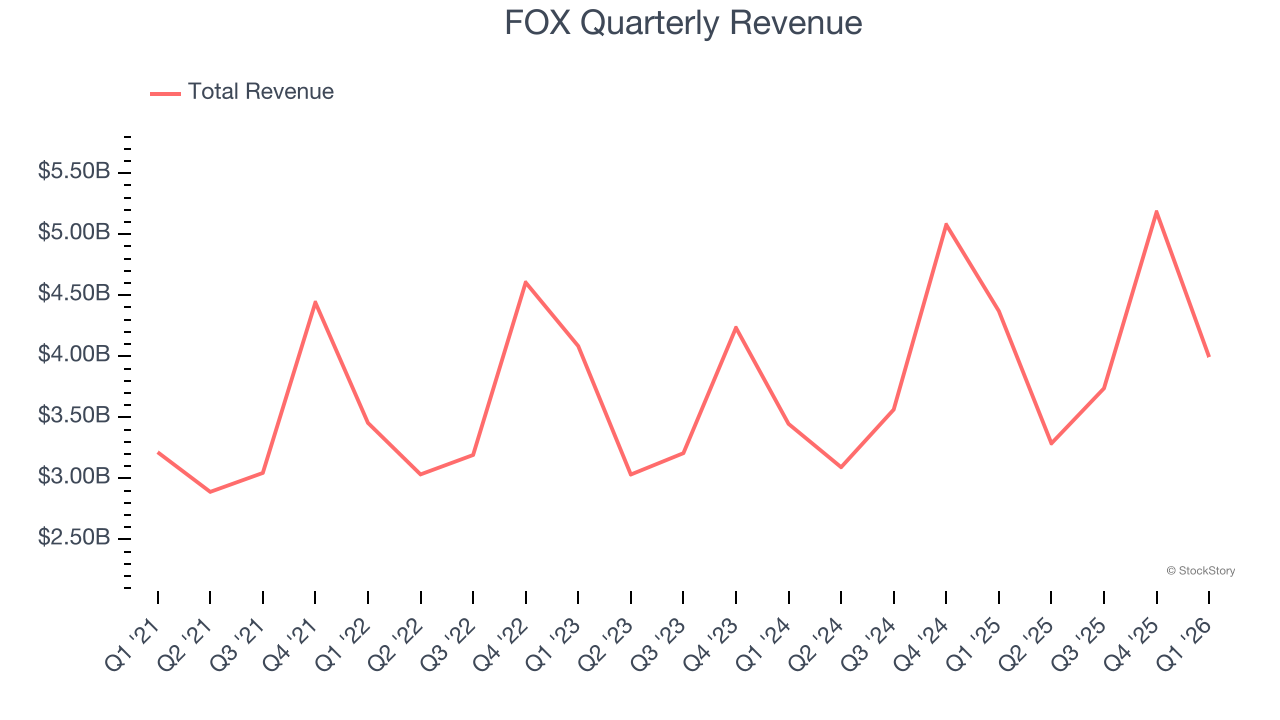

This quarter, FOX’s revenue fell by 8.6% year on year to $3.99 billion but beat Wall Street’s estimates by 4.7%.

Looking ahead, sell-side analysts expect revenue to grow 5.5% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

FOX’s operating margin has risen over the last 12 months and averaged 19.9% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports lousy profitability for a consumer discretionary business.

In Q1, FOX generated an operating margin profit margin of 23.9%, up 6.5 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses.

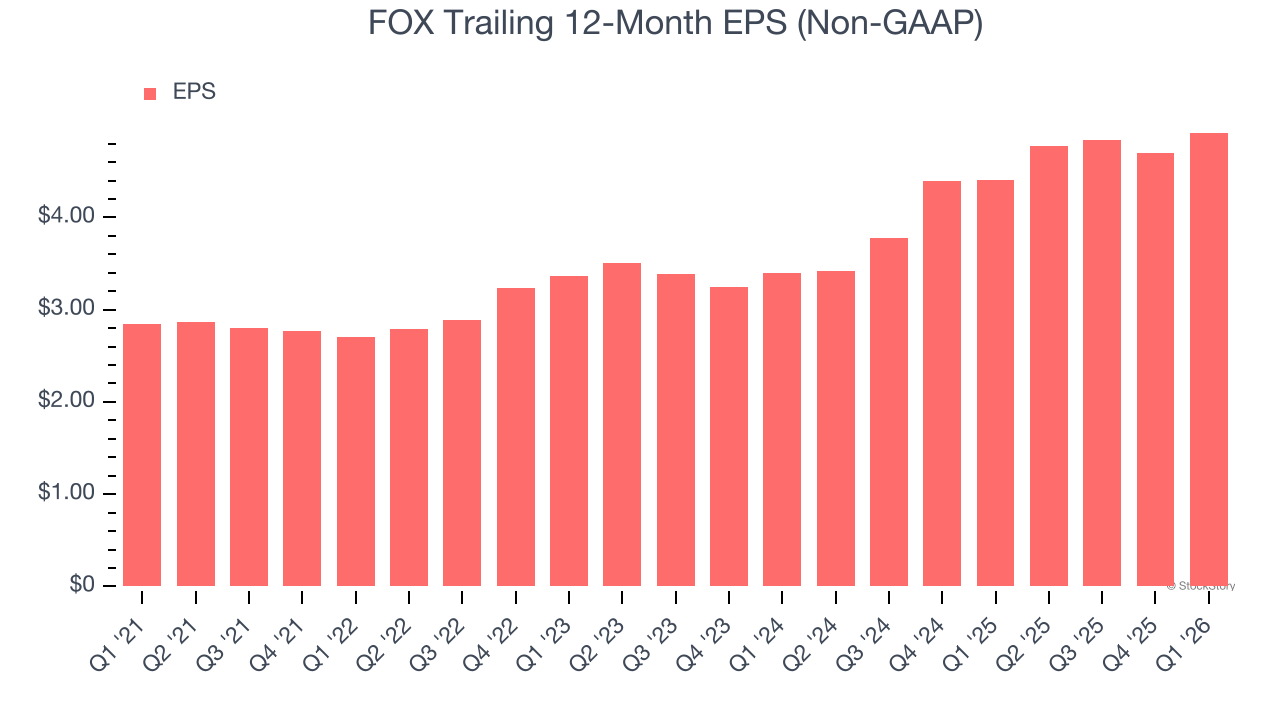

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

FOX’s EPS grew at 11.6% compounded annual growth rate over the last five years. This performance was better than its revenue growth but doesn’t tell us much about its business quality because its operating margin improvement was less than peers.

In Q1, FOX reported adjusted EPS of $1.32, up from $1.10 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects FOX’s full-year EPS of $4.92 to grow 11%.

Key Takeaways from FOX’s Q1 Results

It was good to see FOX beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 4.3% to $65.64 immediately after reporting.

FOX put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).