Since May 2021, the S&P 500 has delivered a total return of 76.6%. But one standout stock has more than doubled the market - over the past five years, Baker Hughes has surged 160% to $64.55 per share. Its momentum hasn’t stopped as it’s also gained 31.9% in the last six months thanks to its solid quarterly results, beating the S&P by 24.8%.

Is there a buying opportunity in Baker Hughes, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Baker Hughes Not Exciting?

We’re glad investors have benefited from the price increase, but we're cautious about Baker Hughes. Here are two reasons there are better opportunities than BKR and a stock we'd rather own.

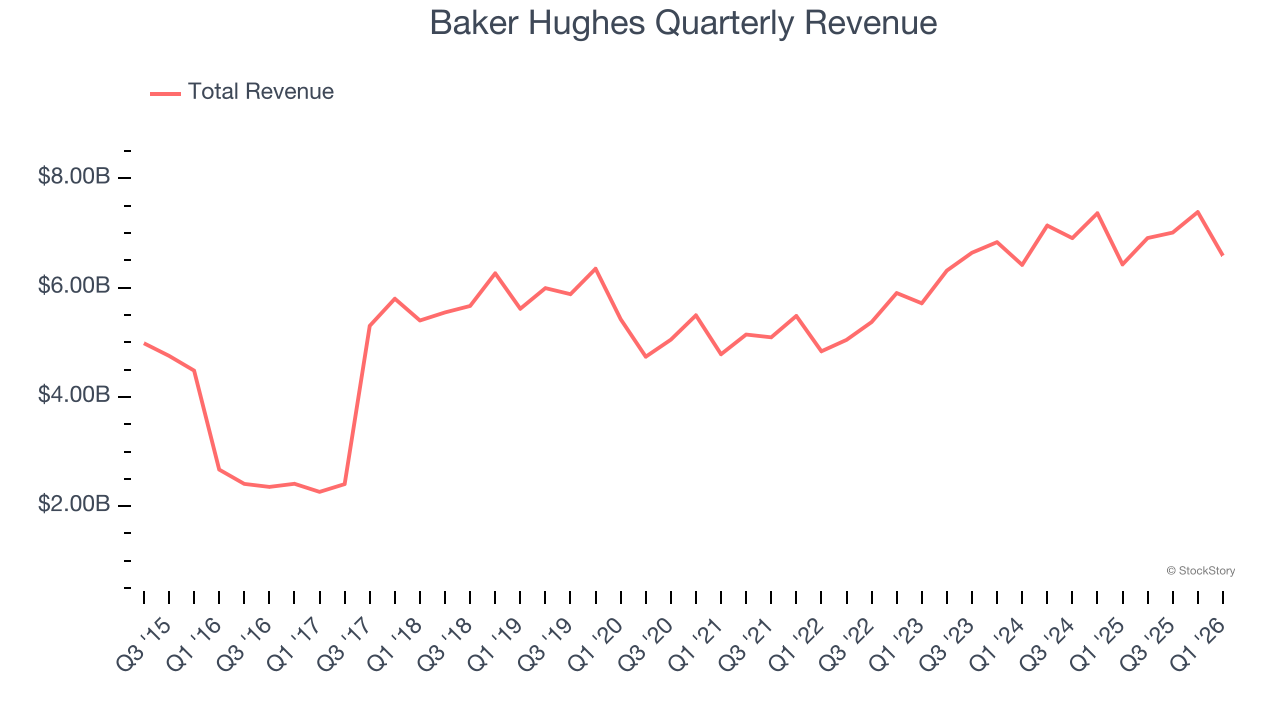

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Unfortunately, Baker Hughes’s 6.8% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the energy upstream and integrated energy sector.

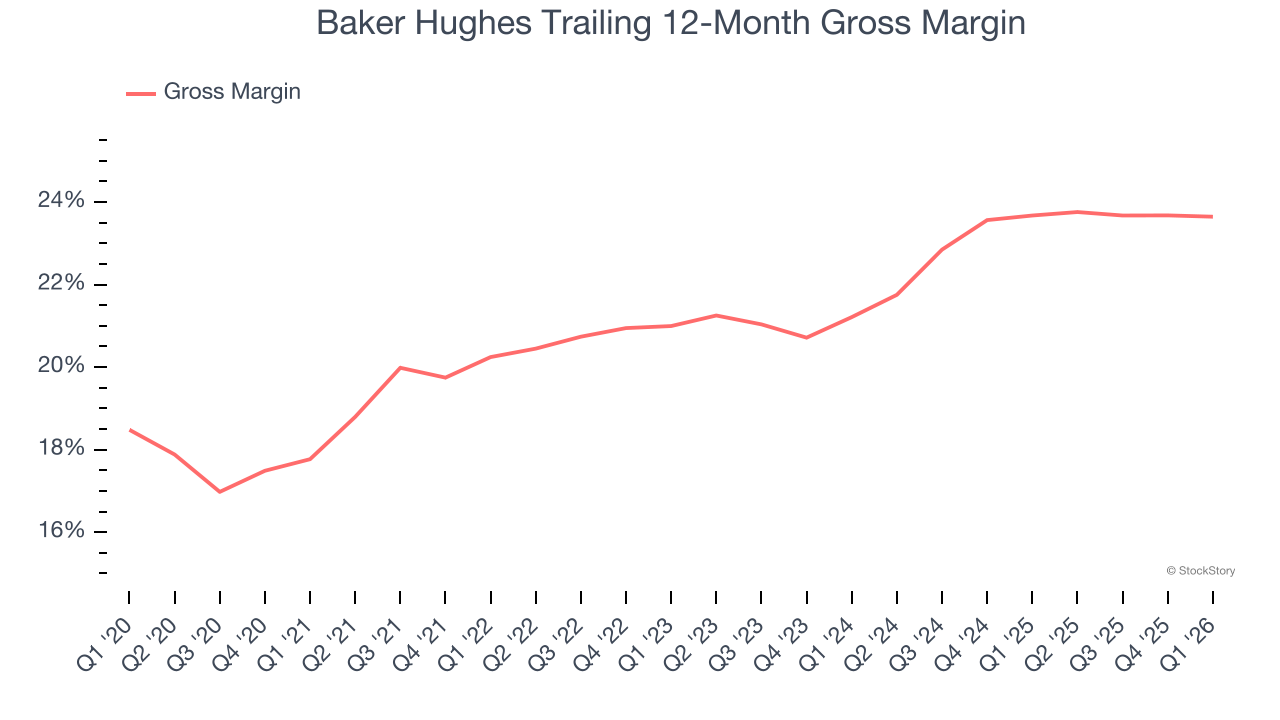

2. Low Gross Margin Reveals Weak Structural Profitability

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Baker Hughes, which averaged 22.1% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

Final Judgment

Baker Hughes’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 27× forward P/E (or $64.55 per share). This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere. Let us point you toward the Amazon and PayPal of Latin America.

Stocks We Like More Than Baker Hughes

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum - both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks - FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.