The past six months have been a windfall for Helmerich & Payne’s shareholders. The company’s stock price has jumped 47.9%, setting a new 52-week high of $39.33 per share. This performance may have investors wondering how to approach the situation.

Is now still a good time to buy HP? Or are investors being too optimistic? Find out in our full research report, it’s free.

Why Does Helmerich & Payne Spark Debate?

Operating the largest fleet of super-spec rigs in North America with technology that can drill horizontal wells over two miles long, Helmerich & Payne (NYSE: HP) provides drilling rigs and crews to oil and gas companies that need wells drilled to extract hydrocarbons from underground.

Two Positive Attributes:

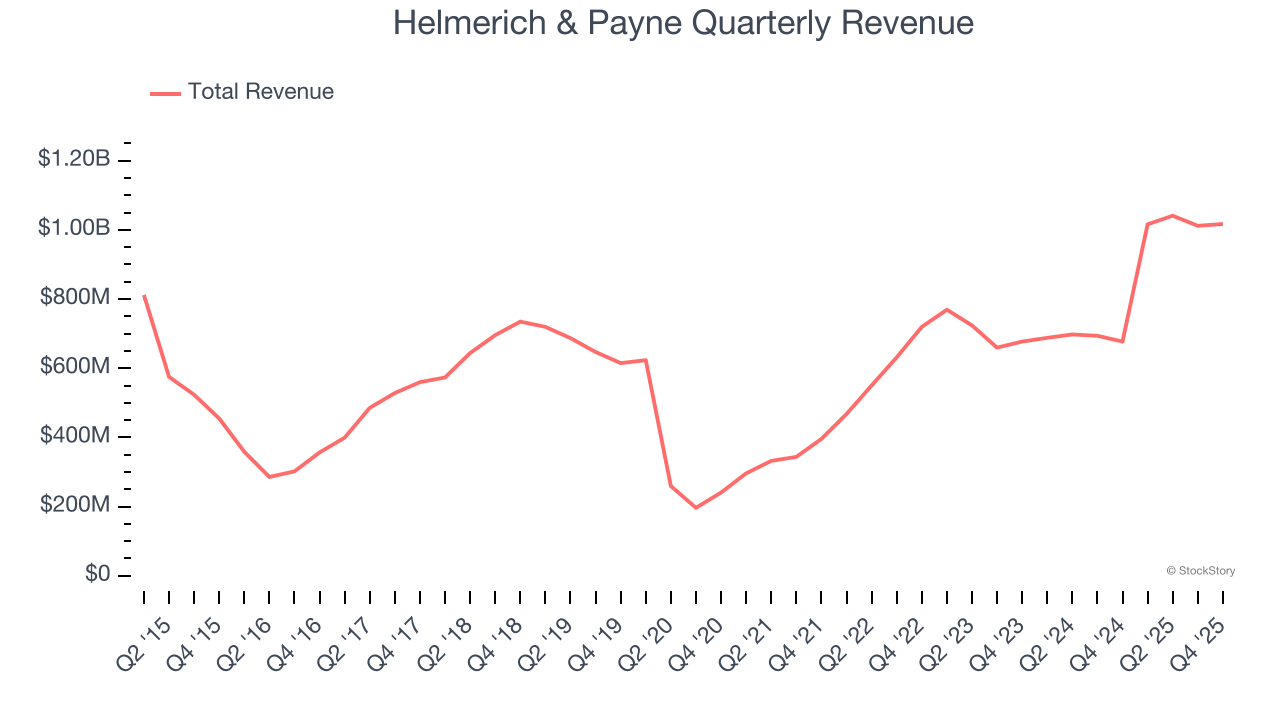

1. Skyrocketing Revenue Shows Strong Momentum

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Luckily, Helmerich & Payne’s sales grew at an incredible 25.4% compounded annual growth rate over the last five years. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

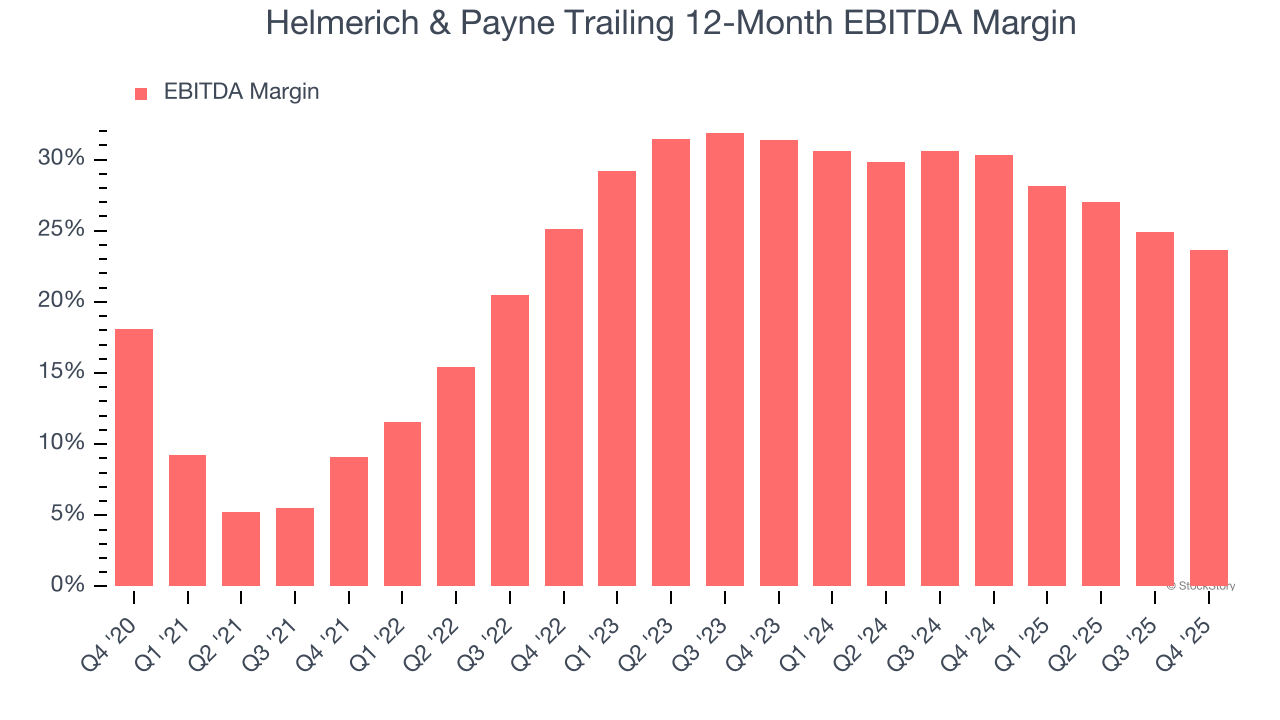

2. EBITDA Margin Rising, Profits Up

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Helmerich & Payne’s EBITDA margin rose by 14.5 percentage points over the last year, as its sales growth gave it immense operating leverage. Its EBITDA margin for the trailing 12 months was 23.6%.

One Reason to be Careful:

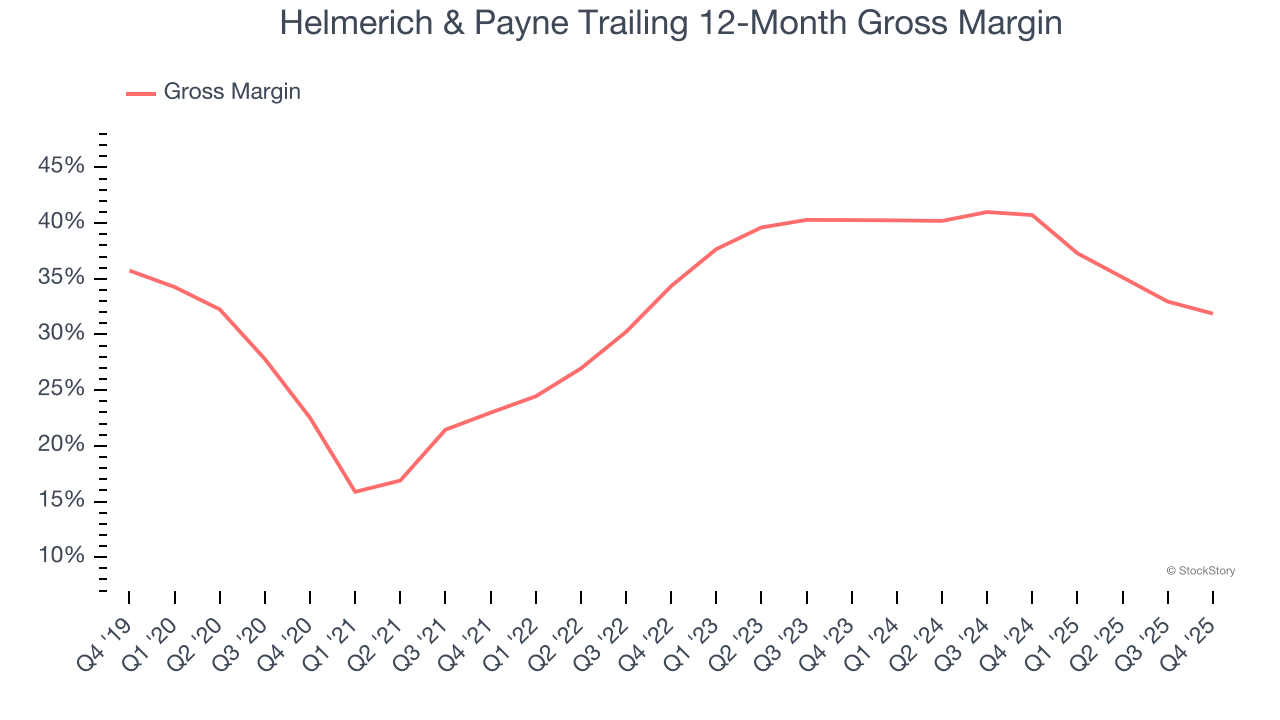

Low Gross Margin Reveals Weak Structural Profitability

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Helmerich & Payne, which averaged 35% gross margin over the last five years, exhibits poor unit economics in the sector. It means the company will struggle more at lower commodity prices than peers with better gross margins.

Final Judgment

Helmerich & Payne’s positive characteristics outweigh the negatives, and with the recent surge, the stock trades at 81.4× forward P/E (or $39.33 per share). Is now a good time to buy despite the apparent froth? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Helmerich & Payne

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.