Credit Acceptance has been treading water for the past six months, recording a small loss of 4.6% while holding steady at $465.46. The stock also fell short of the S&P 500’s 2.5% gain during that period.

Is there a buying opportunity in Credit Acceptance, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Credit Acceptance Will Underperform?

We don't have much confidence in Credit Acceptance. Here are three reasons why CACC doesn't excite us and a stock we'd rather own.

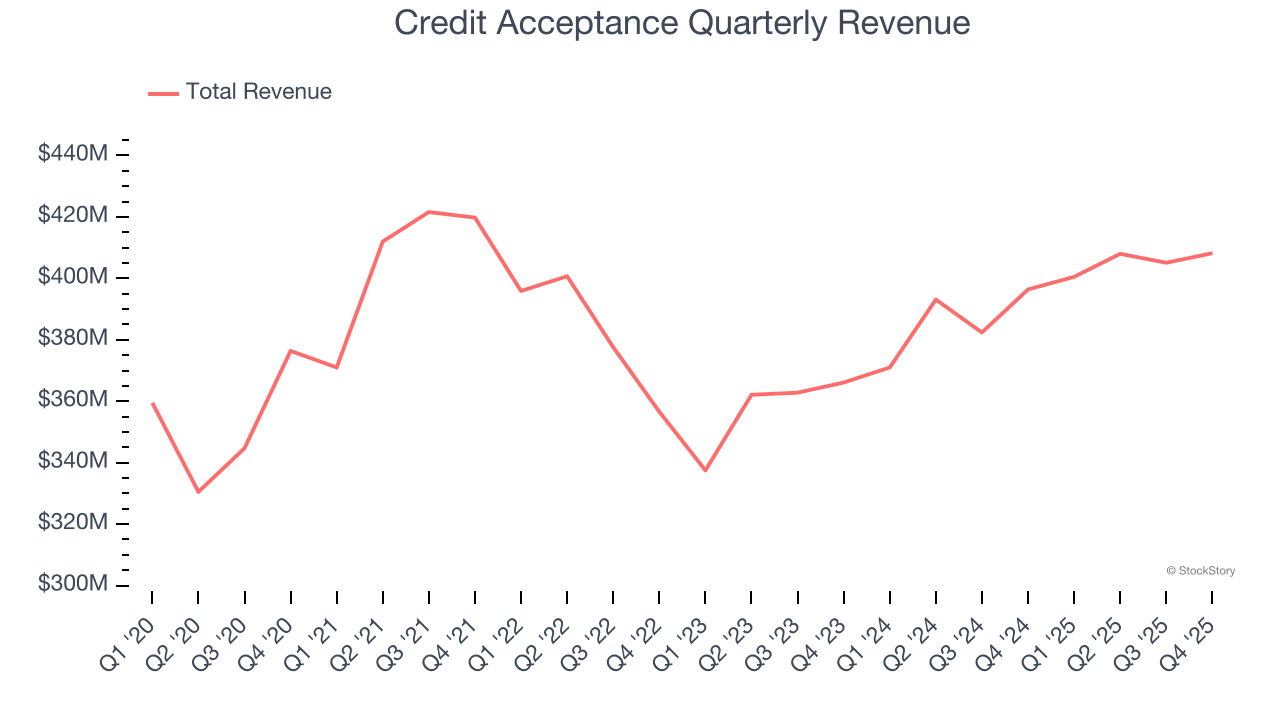

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Unfortunately, Credit Acceptance’s 2.8% annualized revenue growth over the last five years was sluggish. This was below our standards.

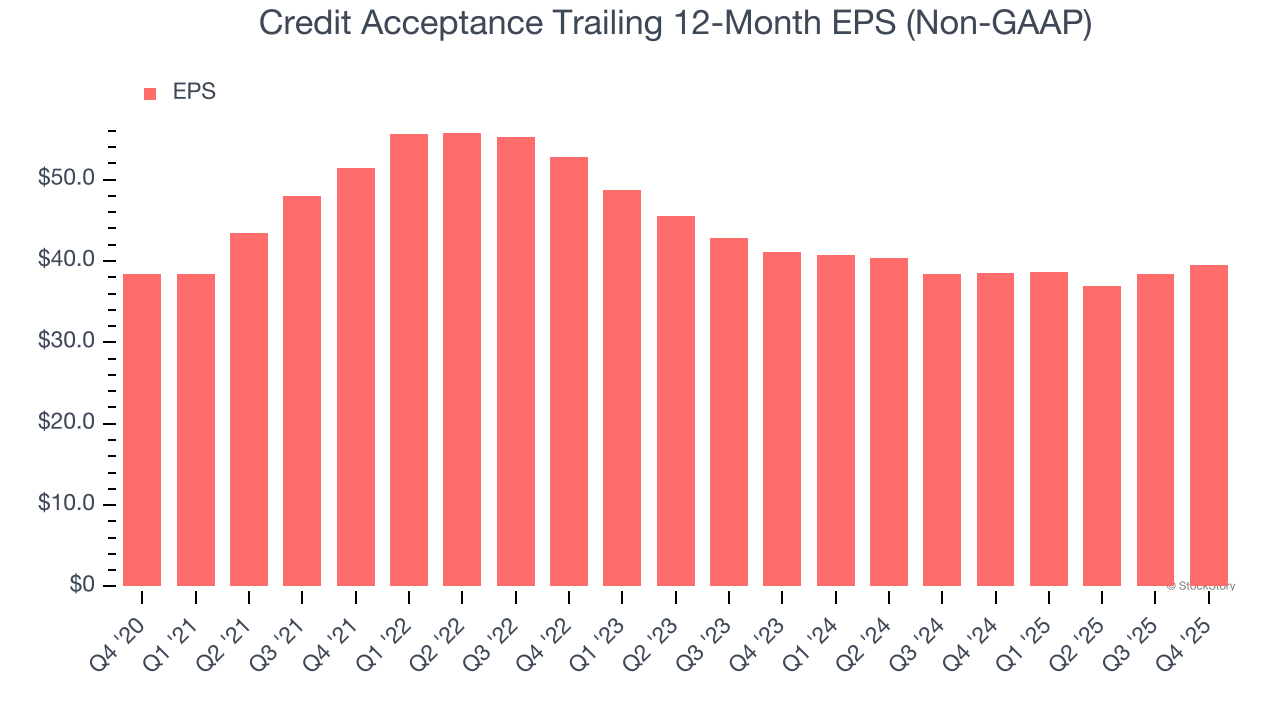

2. EPS Growth Has Stalled

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Credit Acceptance’s flat EPS over the last five years was below its 2.8% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

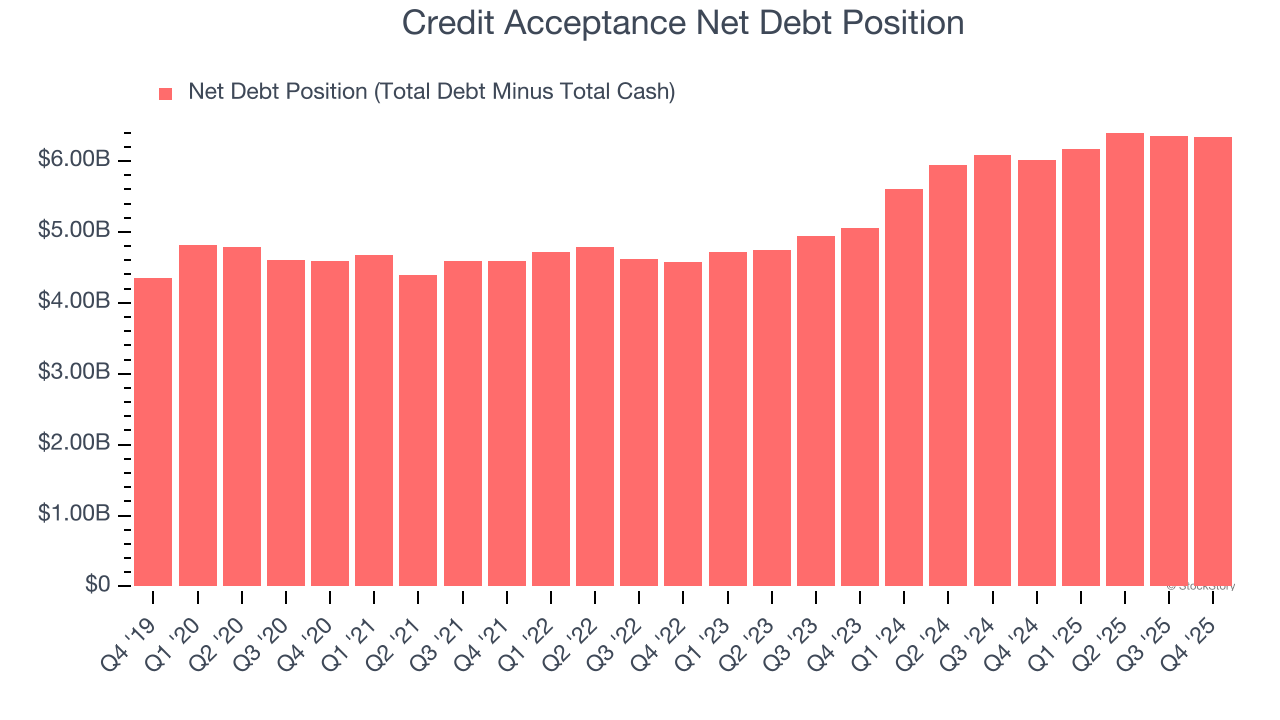

3. High Debt Levels Increase Risk

Credit Acceptance reported $22.8 million of cash and $6.36 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $617.3 million of EBITDA over the last 12 months, we view Credit Acceptance’s 10.3× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

Final Judgment

We cheer for all companies supporting the economy, but in the case of Credit Acceptance, we’ll be cheering from the sidelines. With its shares underperforming the market lately, the stock trades at 11× forward P/E (or $465.46 per share). This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now. We’d suggest looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Credit Acceptance

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.