Since April 2021, the S&P 500 has delivered a total return of 57.8%. But one standout stock has more than doubled the market - over the past five years, TJX has surged 142% to $159.51 per share. Its momentum hasn’t stopped as it’s also gained 10.5% in the last six months, beating the S&P by 16%.

Is now still a good time to buy TJX? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Does TJX Spark Debate?

Initially based on a strategy of buying excess inventory from manufacturers or other retailers, TJX (NYSE: TJX) is an off-price retailer that sells brand-name apparel and other goods at prices much lower than department stores.

Two Positive Attributes:

1. Surging Same-Store Sales Show Increasing Demand

Same-store sales is an industry measure of whether revenue is growing at existing stores, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

TJX’s demand has been spectacular for a retailer over the last two years. On average, the company has increased its same-store sales by an impressive 3.9% per year.

2. Economies of Scale Give It Negotiating Leverage with Suppliers

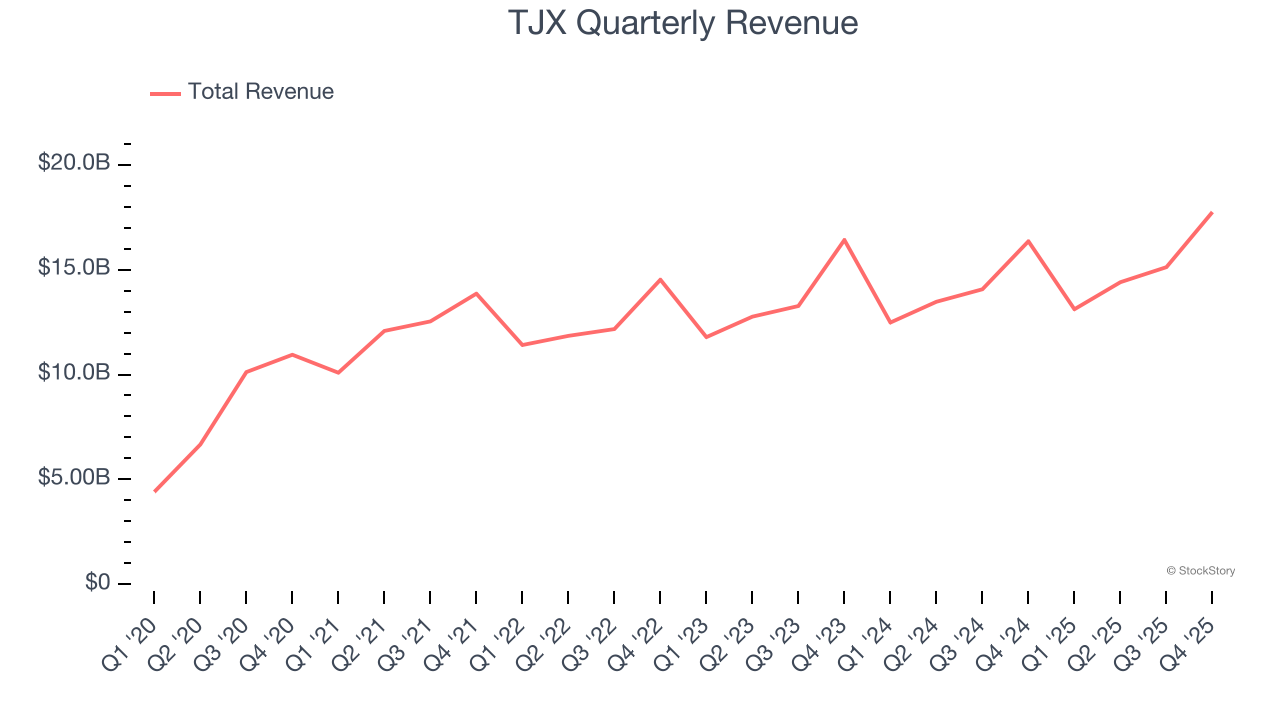

With $60.37 billion in revenue over the past 12 months, TJX is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To accelerate sales, TJX likely needs to optimize its pricing or lean into international expansion.

One Reason to be Careful:

Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, TJX’s 6.5% annualized revenue growth over the last three years was tepid. This wasn’t a great result compared to the rest of the consumer retail sector, but there are still things to like about TJX.

Final Judgment

TJX has huge potential even though it has some open questions, and with its shares outperforming the market lately, the stock trades at 30.5× forward P/E (or $159.51 per share). Is now the time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.