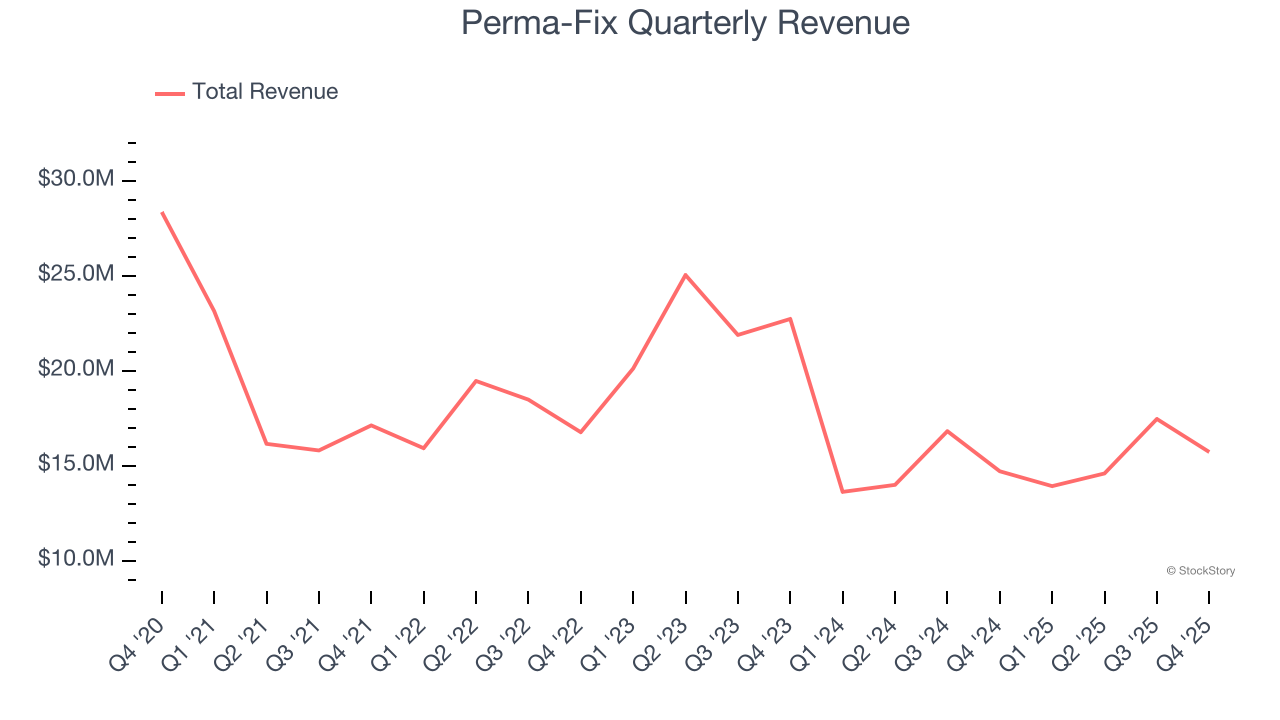

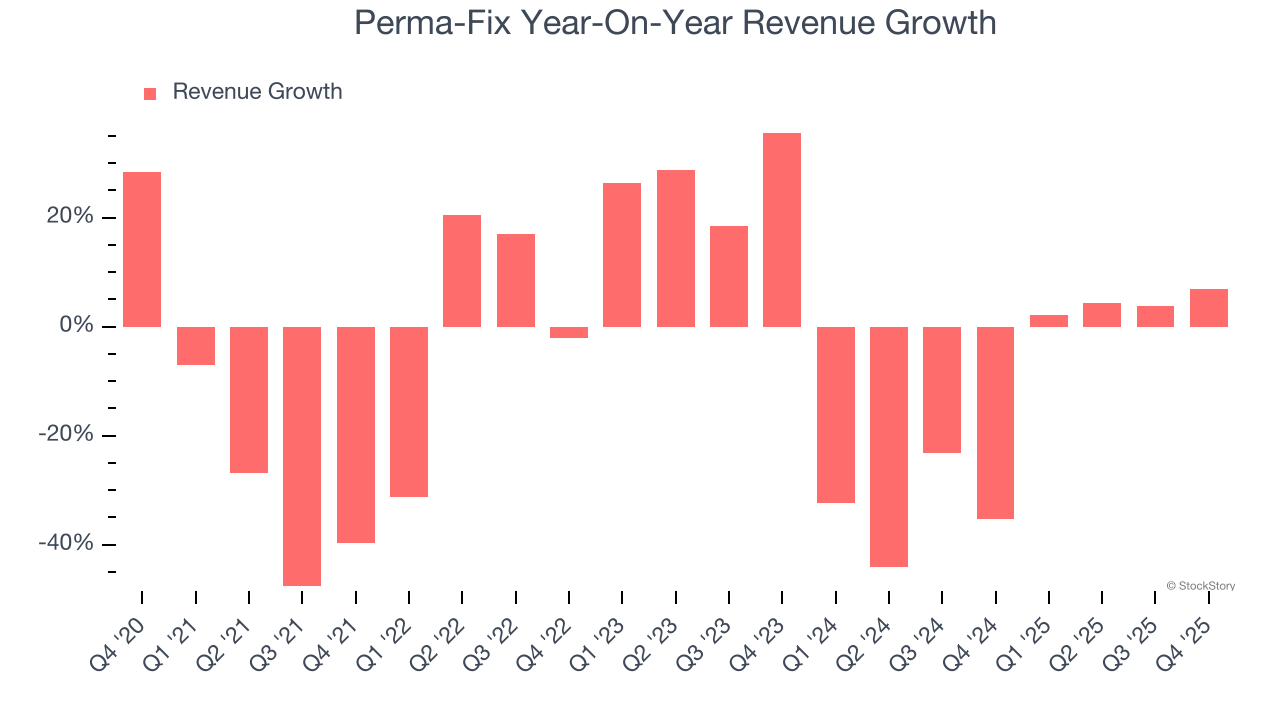

Environmental waste treatment and services provider Perma-Fix (NASDAQ: PESI) fell short of the market’s revenue expectations in Q4 CY2025, but sales rose 6.9% year on year to $15.72 million. Its GAAP loss of $0.31 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Perma-Fix? Find out by accessing our full research report, it’s free.

Perma-Fix (PESI) Q4 CY2025 Highlights:

- Revenue: $15.72 million vs analyst estimates of $17.7 million (6.9% year-on-year growth, 11.2% miss)

- EPS (GAAP): -$0.31 vs analyst estimates of -$0.09 (significant miss)

- Adjusted EBITDA: -$2.68 million (-17.1% margin, 11% year-on-year growth)

- Adjusted EBITDA Margin: -17.1%, up from -20.5% in the same quarter last year

- Market Capitalization: $223.1 million

Mark Duff, President and Chief Executive Officer of the Company, commented, “During 2025, we focused on strengthening Perma-Fix’s operational foundation and positioning the Company for the next phase of growth tied to the U.S. Department of Energy’s (“DOE”) Hanford cleanup mission.

Company Overview

Tackling hazardous waste challenges since 1990, Perma-Fix (NASDAQ: PESI) provides environmental waste treatment services.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Perma-Fix’s demand was weak over the last five years as its sales fell at a 10.2% annual rate. This wasn’t a great result and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Perma-Fix’s recent performance shows its demand remained suppressed as its revenue has declined by 17.1% annually over the last two years.

This quarter, Perma-Fix’s revenue grew by 6.9% year on year to $15.72 million, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 68% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will spur better top-line performance.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

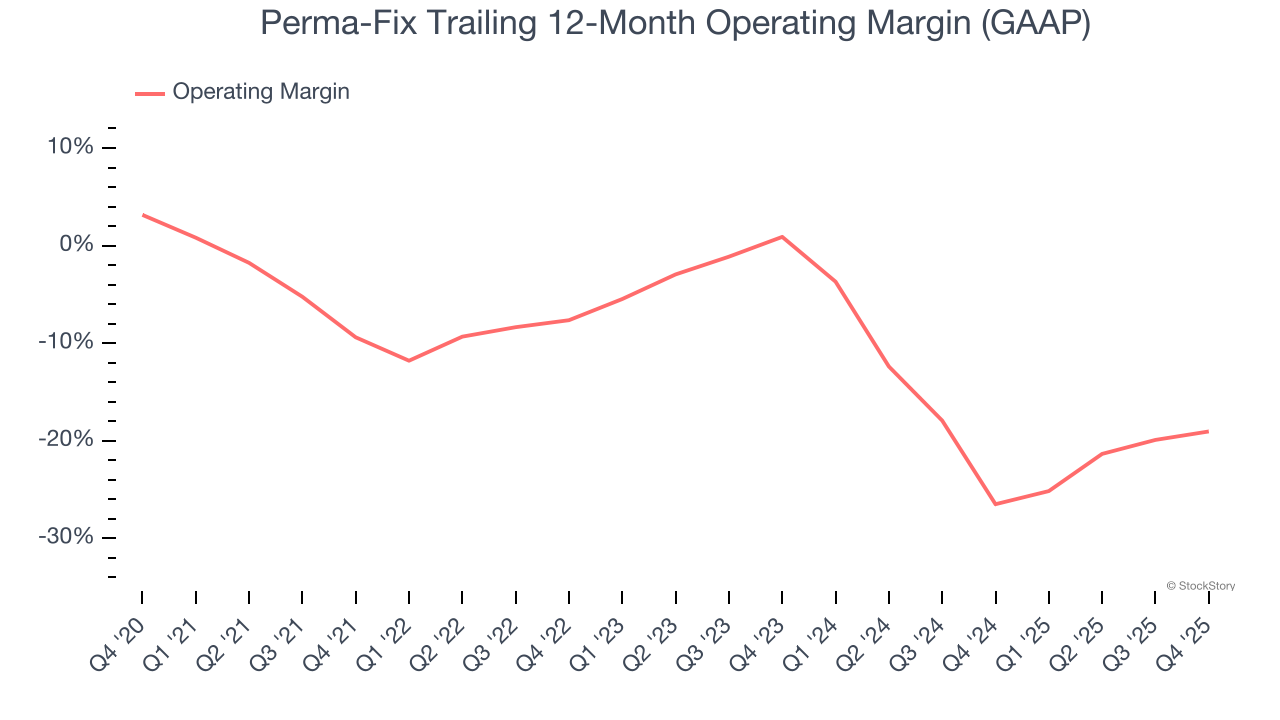

Operating Margin

Perma-Fix’s high expenses have contributed to an average operating margin of negative 11% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, Perma-Fix’s operating margin decreased by 9.7 percentage points over the last five years. Perma-Fix’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Perma-Fix generated a negative 20.6% operating margin. The company's consistent lack of profits raise a flag.

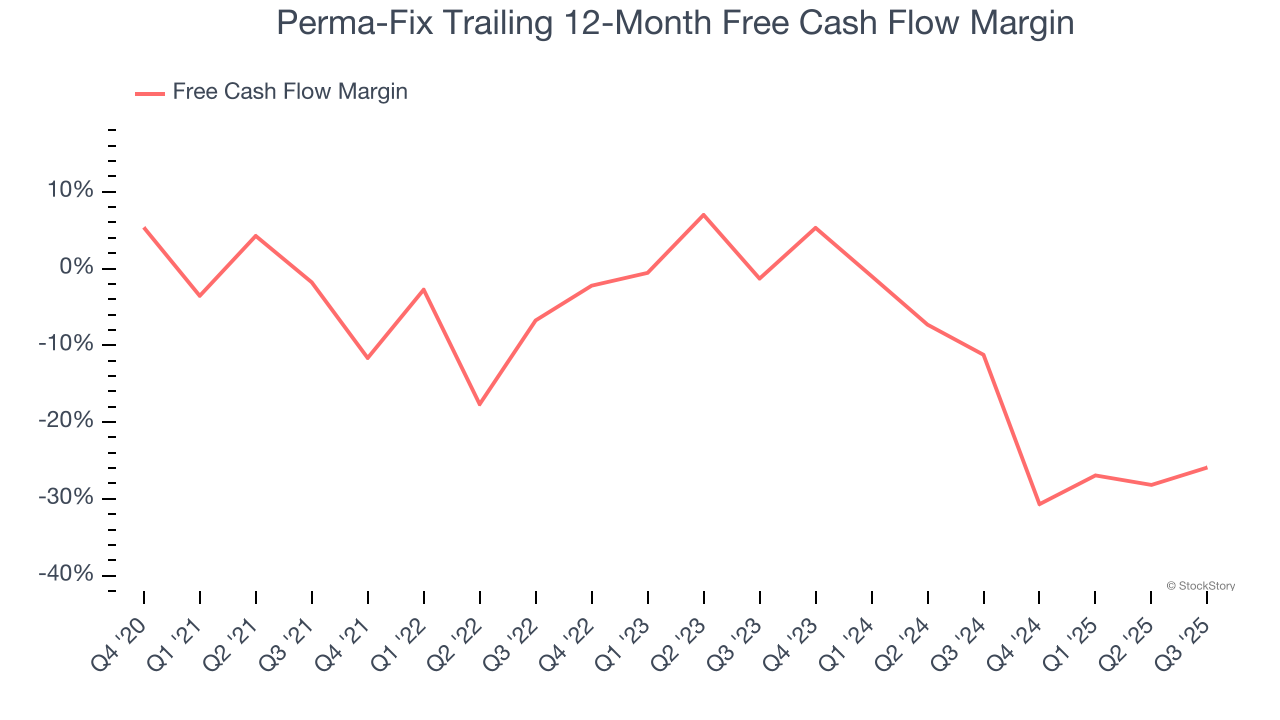

Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Perma-Fix’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 10.3%, meaning it lit $10.25 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Perma-Fix’s margin dropped by 14.5 percentage points during that time. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Key Takeaways from Perma-Fix’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.7% to $11.35 immediately after reporting.

Perma-Fix may have had a tough quarter, but does that actually create an opportunity to invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).