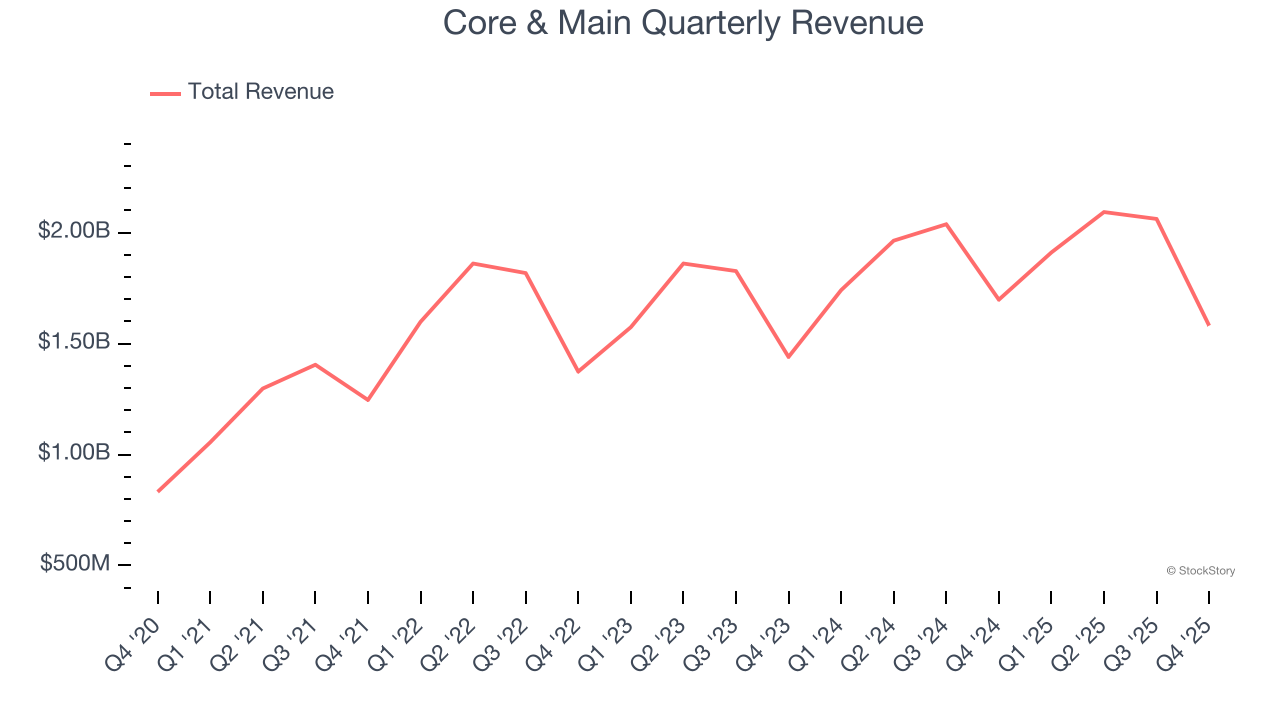

Water and fire protection solutions company Core & Main (NYSE: CNM) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 6.9% year on year to $1.58 billion. The company’s full-year revenue guidance of $7.85 billion at the midpoint came in 1% below analysts’ estimates. Its non-GAAP profit of $0.52 per share was 57.8% above analysts’ consensus estimates.

Is now the time to buy Core & Main? Find out by accessing our full research report, it’s free.

Core & Main (CNM) Q4 CY2025 Highlights:

- Revenue: $1.58 billion vs analyst estimates of $1.59 billion (6.9% year-on-year decline, 0.7% miss)

- Adjusted EPS: $0.52 vs analyst estimates of $0.33 (57.8% beat)

- Adjusted EBITDA: $167 million vs analyst estimates of $165.2 million (10.6% margin, 1.1% beat)

- EBITDA guidance for the upcoming financial year 2026 is $965 million at the midpoint, below analyst estimates of $987.4 million

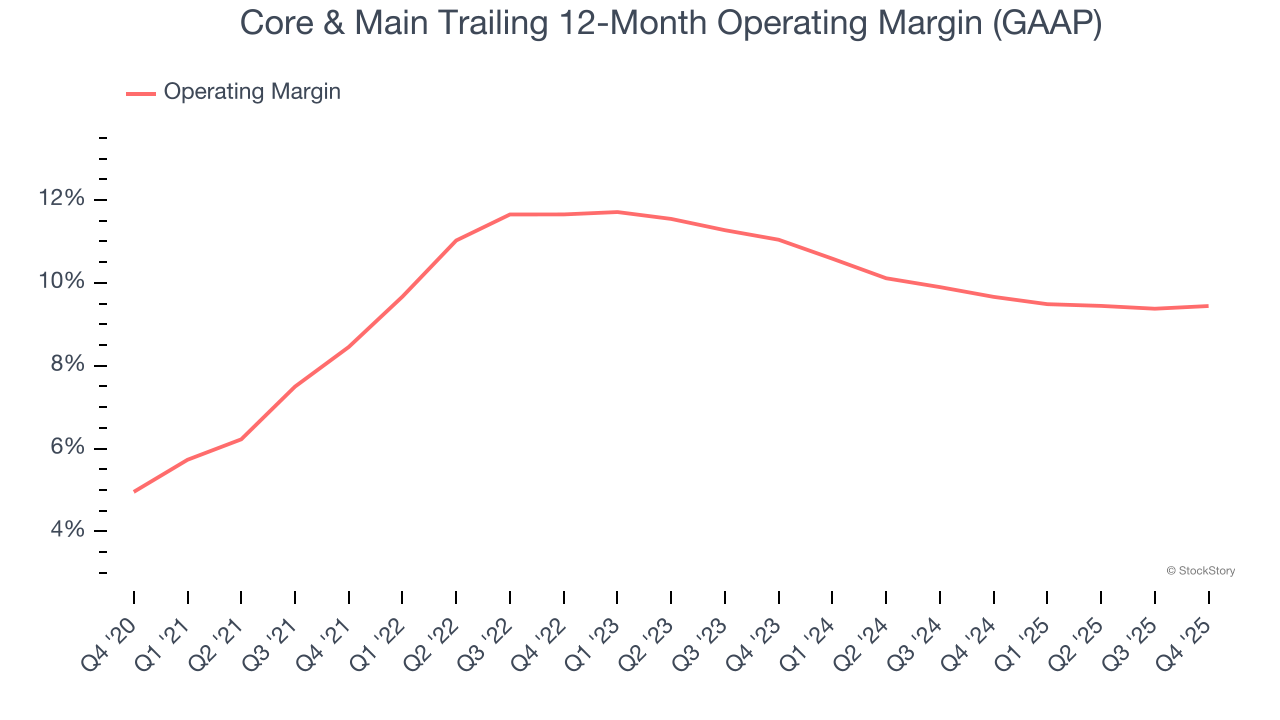

- Operating Margin: 7.5%, in line with the same quarter last year

- Free Cash Flow Margin: 16%, up from 13.2% in the same quarter last year

- Market Capitalization: $9.14 billion

“Fiscal 2025 marked our 16th consecutive year of sales growth, a result that reflects the resilience of our business, the long-term strength of our end markets and the disciplined execution by our teams across the country," said Mark Witkowski, CEO of Core & Main.

Company Overview

Formerly a division of industrial distributor HD Supply, Core & Main (NYSE: CNM) is a provider of water, wastewater, and fire protection products and services.

Revenue Growth

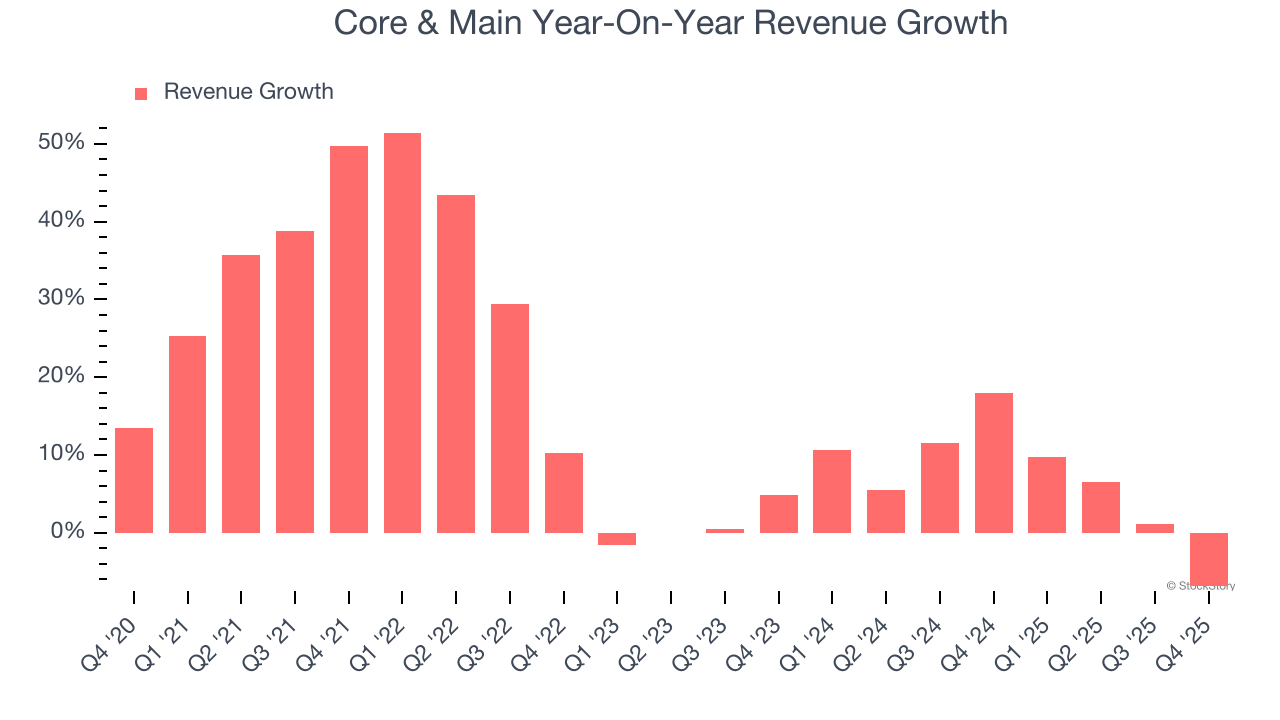

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Core & Main’s sales grew at an incredible 16% compounded annual growth rate over the last five years. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Core & Main’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 6.8% over the last two years was well below its five-year trend.

This quarter, Core & Main missed Wall Street’s estimates and reported a rather uninspiring 6.9% year-on-year revenue decline, generating $1.58 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4% over the next 12 months, a slight deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Core & Main’s operating margin has generally stayed the same over the last 12 months, averaging 10.1% over the last five years. This profitability was solid for an industrials business and shows it’s an efficient company that manages its expenses well. This was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Core & Main’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but Core & Main’s performance still shows it’s one of the better Infrastructure Distributors companies as most peers saw their margins plummet.

In Q4, Core & Main generated an operating margin profit margin of 7.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

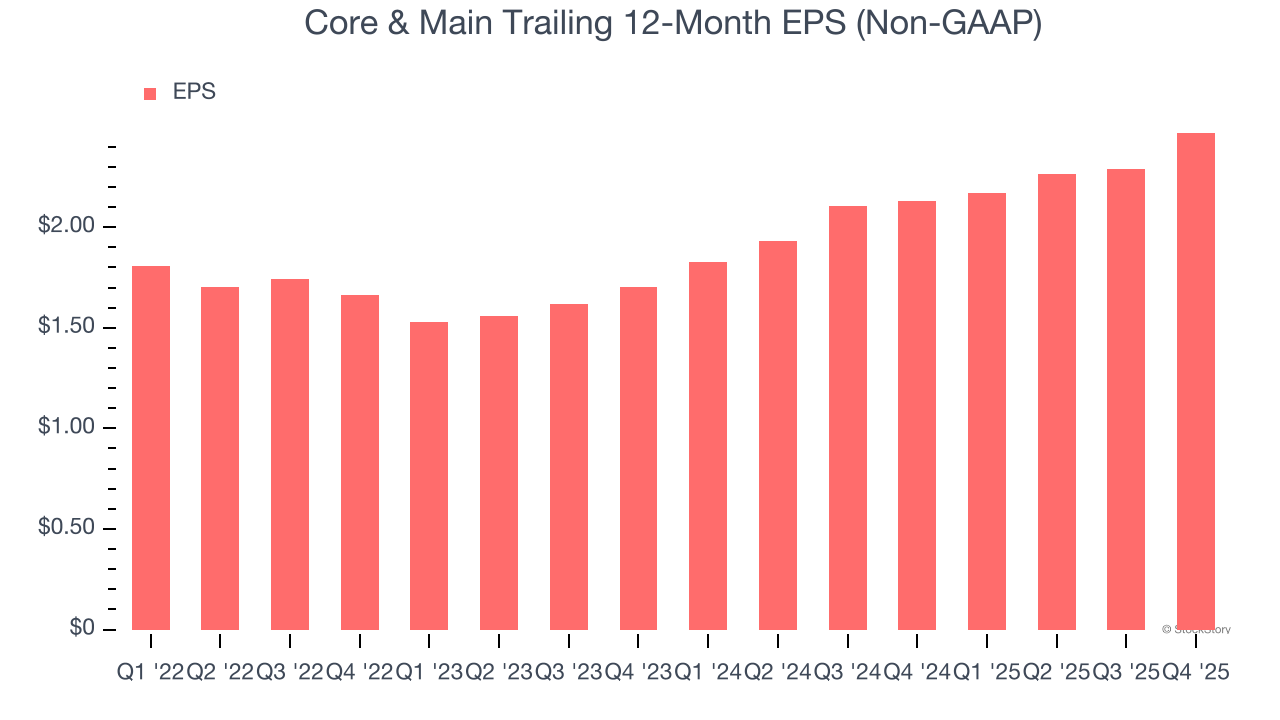

Core & Main’s full-year EPS grew at a solid 10.4% compounded annual growth rate over the last four years, better than the broader industrials sector.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Core & Main’s EPS grew at an astounding 20.4% compounded annual growth rate over the last two years, higher than its 6.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

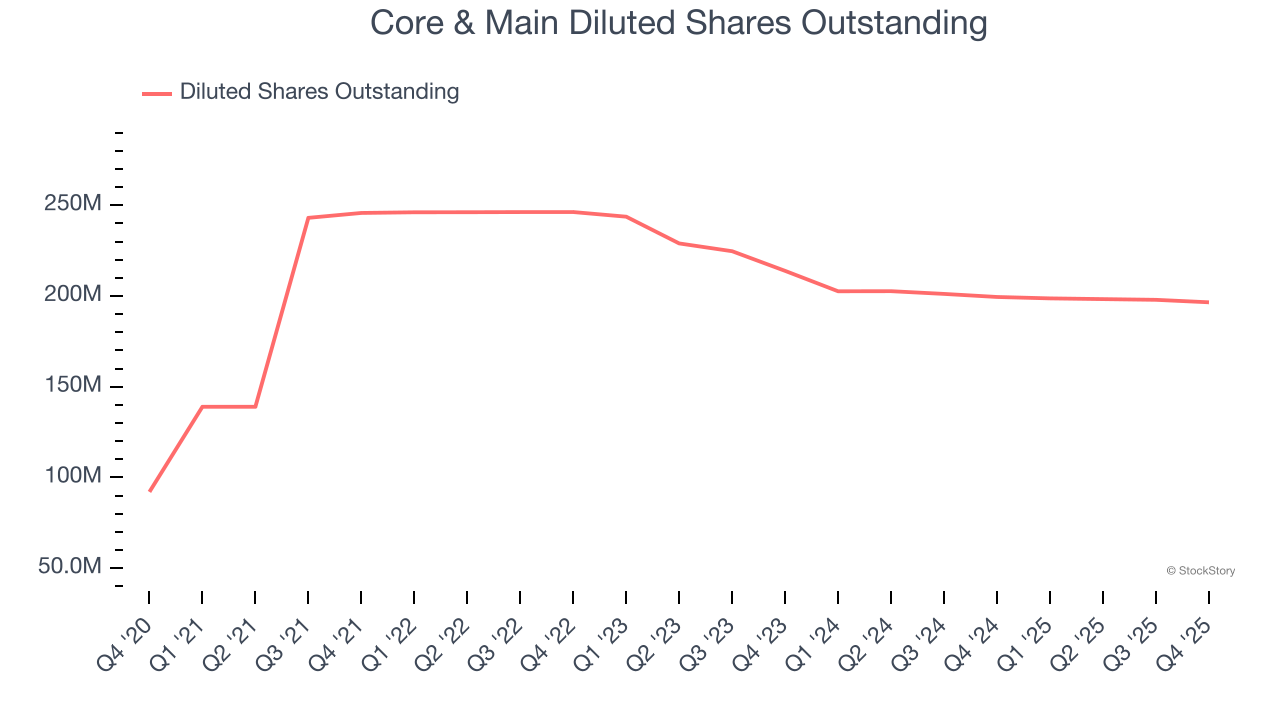

Diving into the nuances of Core & Main’s earnings can give us a better understanding of its performance. A two-year view shows that Core & Main has repurchased its stock, shrinking its share count by 8.1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Core & Main reported adjusted EPS of $0.52, up from $0.34 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Core & Main’s full-year EPS of $2.47 to grow 4.3%.

Key Takeaways from Core & Main’s Q4 Results

It was good to see Core & Main beat analysts’ EPS expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its revenue fell slightly short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 6.3% to $45.37 immediately following the results.

So do we think Core & Main is an attractive buy at the current price? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).