Since September 2025, Annaly Capital Management has been in a holding pattern, posting a small return of 2.2% while floating around $21.25.

Is now the time to buy Annaly Capital Management, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Annaly Capital Management Will Underperform?

We're swiping left on Annaly Capital Management for now. Here are three reasons there are better opportunities than NLY and a stock we'd rather own.

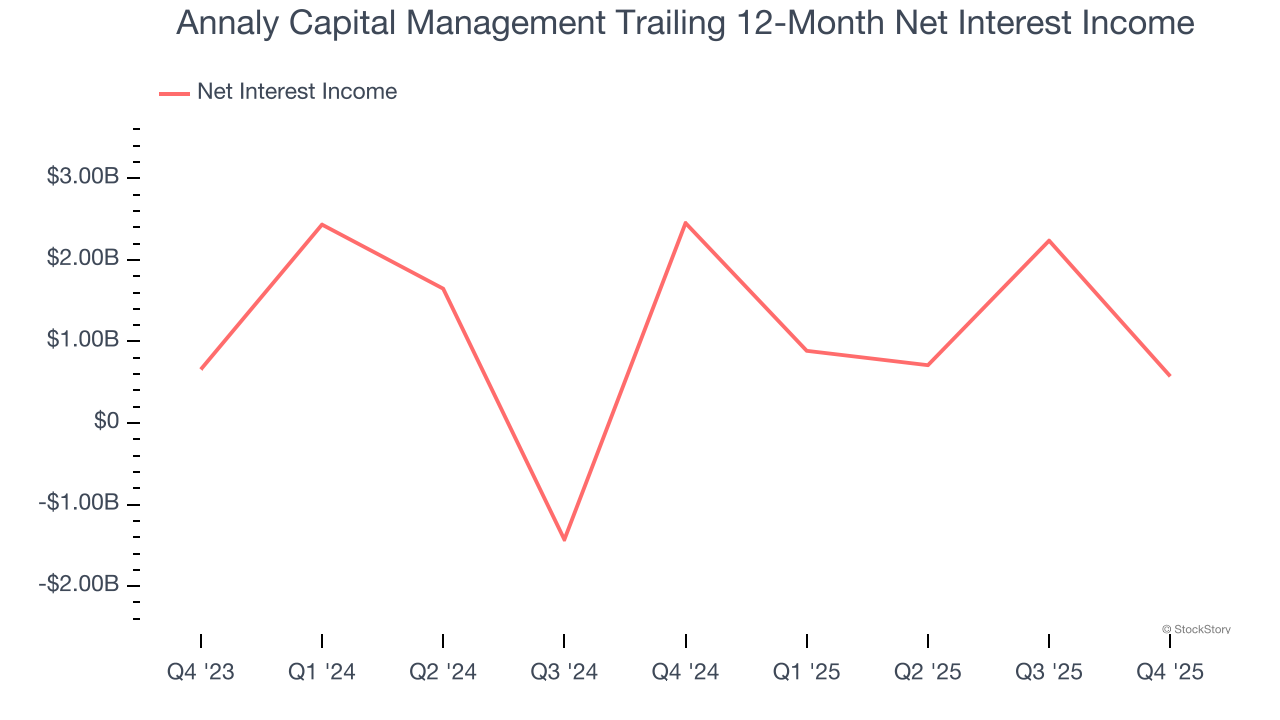

1. Declining Net Interest Income Reflects Weakness

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Annaly Capital Management’s net interest income has declined by 11.4% annually over the last five years, much worse than the broader banking industry. A silver lining is that lending outperformed its other business lines.

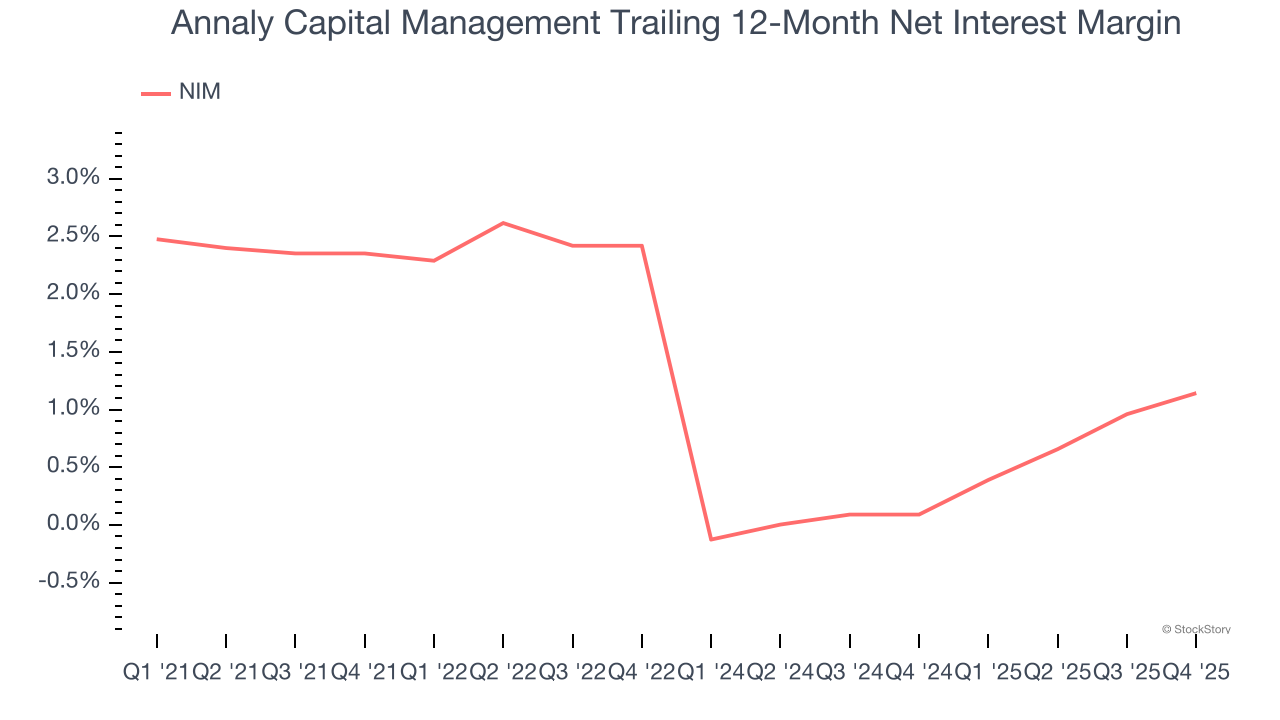

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

The net interest margin (NIM) is a key profitability indicator that measures the difference between what a bank earns on its loans and what it pays on its deposits. This metric measures how efficiently one can generate income from its core lending activities.

Over the past two years, we can see that Annaly Capital Management’s net interest margin averaged a poor breakeven, indicating the company has weak loan book economics.

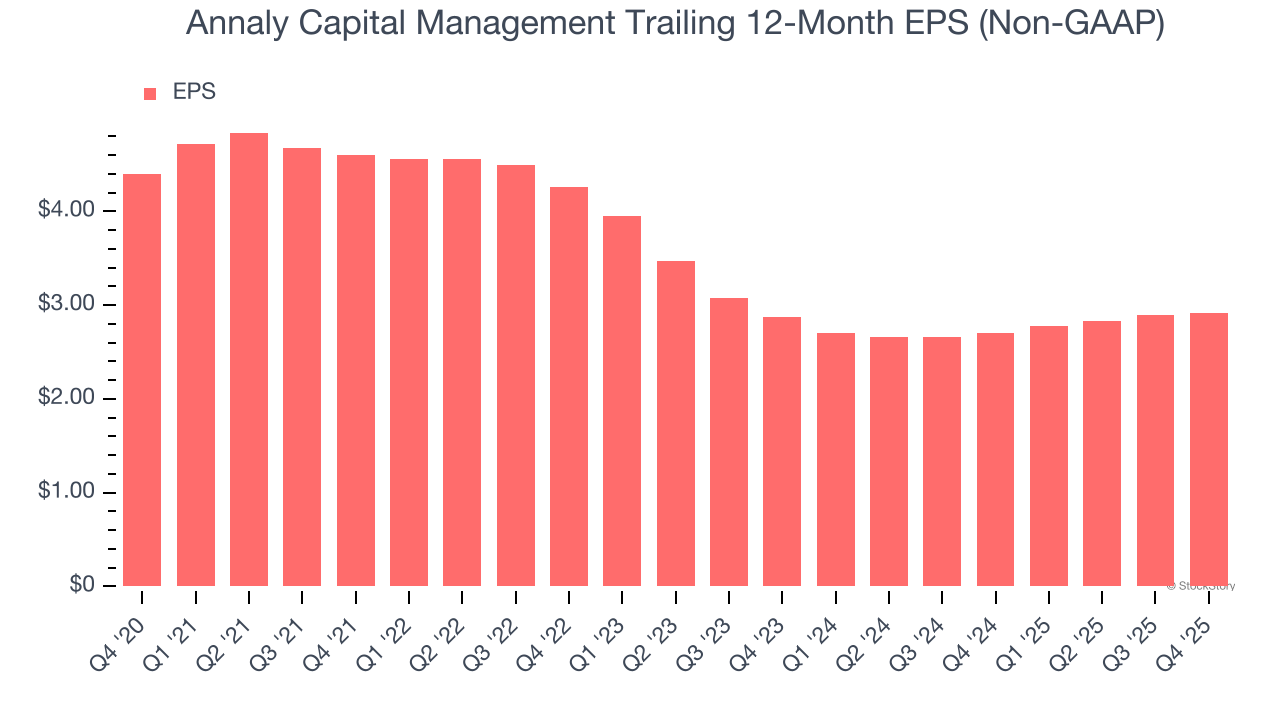

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Annaly Capital Management, its EPS and revenue declined by 7.9% and 12.9% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Annaly Capital Management’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

Annaly Capital Management falls short of our quality standards. That said, the stock currently trades at 1× forward P/B (or $21.25 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Like More Than Annaly Capital Management

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.