Since September 2025, Republic Services has been in a holding pattern, posting a small loss of 4.7% while floating around $216.72.

Is now the time to buy Republic Services, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is Republic Services Not Exciting?

We're sitting this one out for now. Here are three reasons there are better opportunities than RSG and a stock we'd rather own.

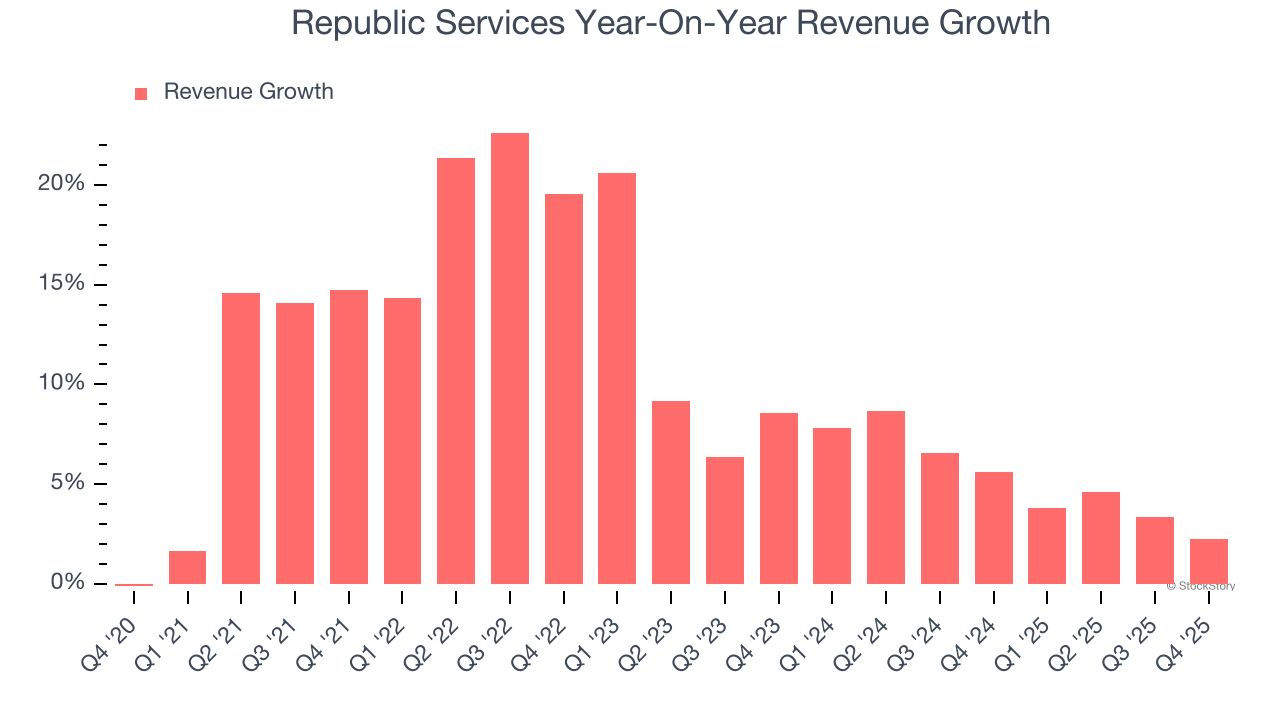

1. Lackluster Revenue Growth

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Republic Services’s recent performance shows its demand has slowed as its annualized revenue growth of 5.3% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

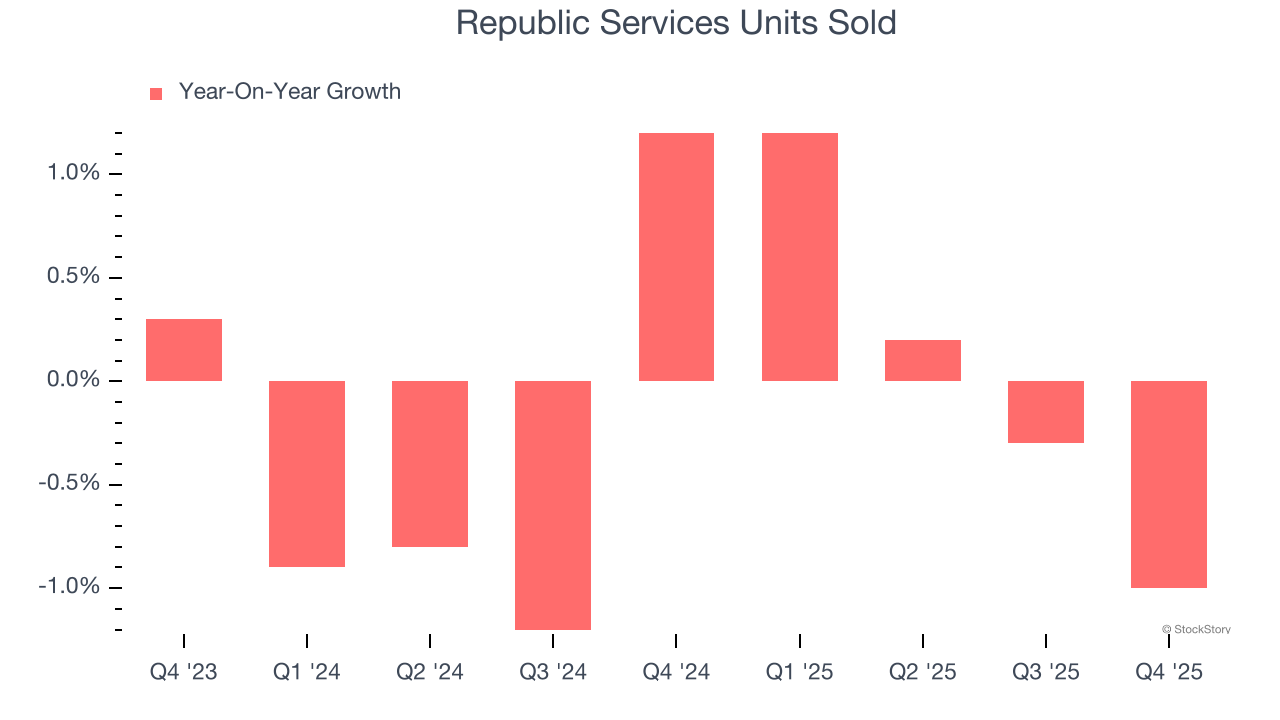

2. Sales Volumes Stall, Demand Waning

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Waste Management company because there’s a ceiling to what customers will pay.

Over the last two years, Republic Services failed to grow its units sold. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Republic Services might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

3. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Republic Services’s revenue to rise by 3.2%, a slight deceleration versus its 10.3% annualized growth for the past five years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

Final Judgment

Republic Services isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 30.3× forward P/E (or $216.72 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the Amazon and PayPal of Latin America.

Stocks We Would Buy Instead of Republic Services

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.