Over the last six months, Radian Group shares have sunk to $32.86, producing a disappointing 9.6% loss - worse than the S&P 500’s 1.9% drop. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Radian Group, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Radian Group Not Exciting?

Despite the more favorable entry price, we're swiping left on Radian Group for now. Here are three reasons we avoid RDN and a stock we'd rather own.

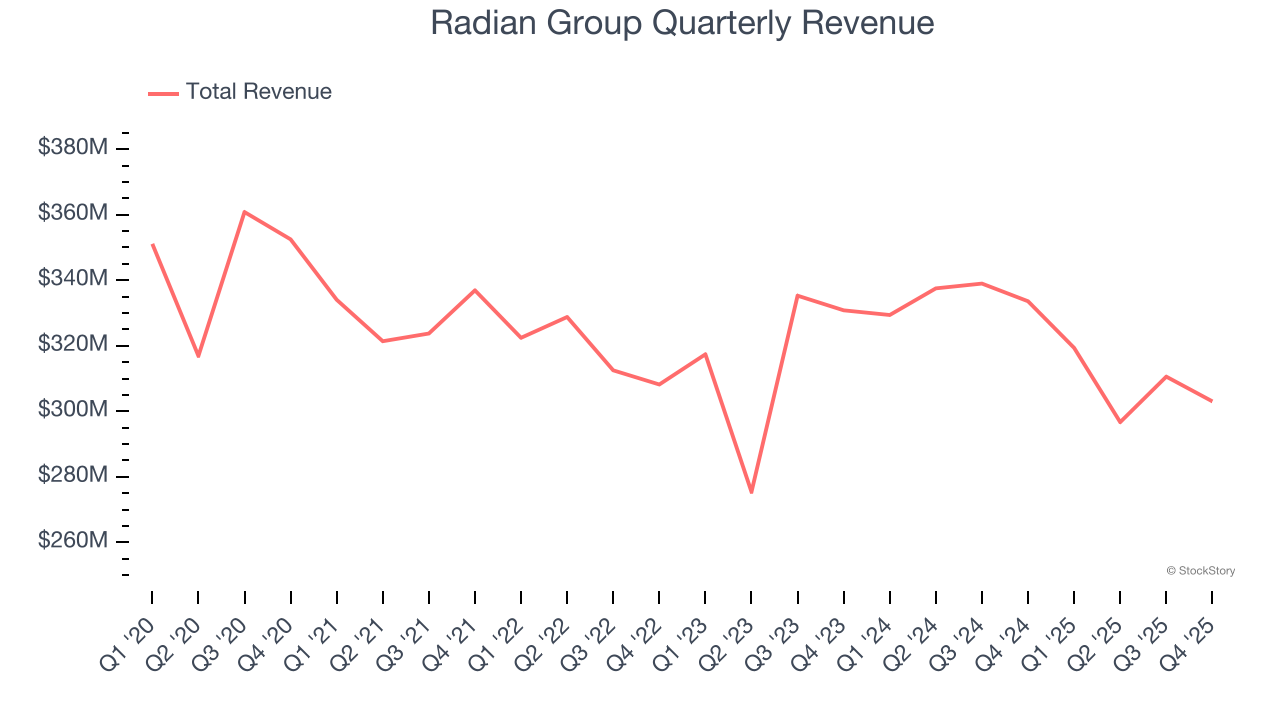

1. Revenue Spiraling Downwards

Big picture, insurers generate revenue from three key sources. The first is the core business of underwriting policies. The second source is income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services.

Radian Group’s demand was weak over the last five years as its revenue fell at a 2.3% annual rate. This was below our standards and is a sign of lacking business quality.

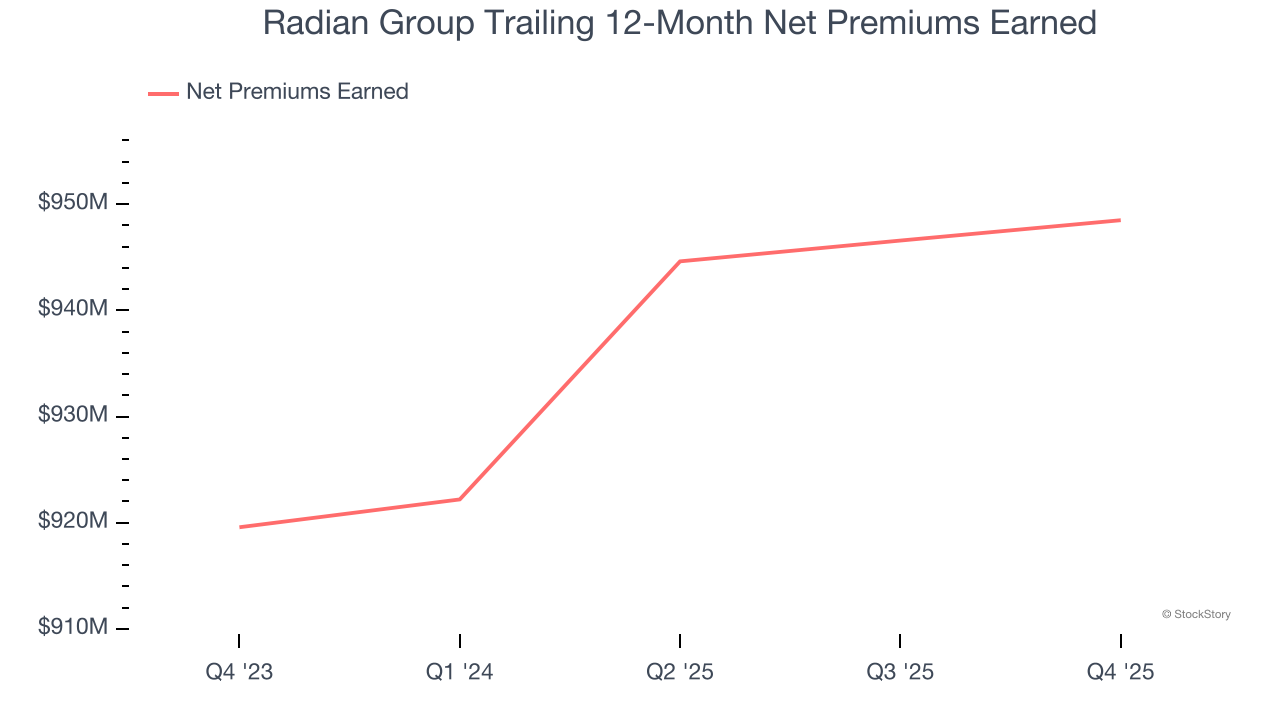

2. Declining Net Premiums Earned Reflect Weakness

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

Radian Group’s net premiums earned has declined by 3.2% annually over the last five years, much worse than the broader insurance industry and in line with its total revenue.

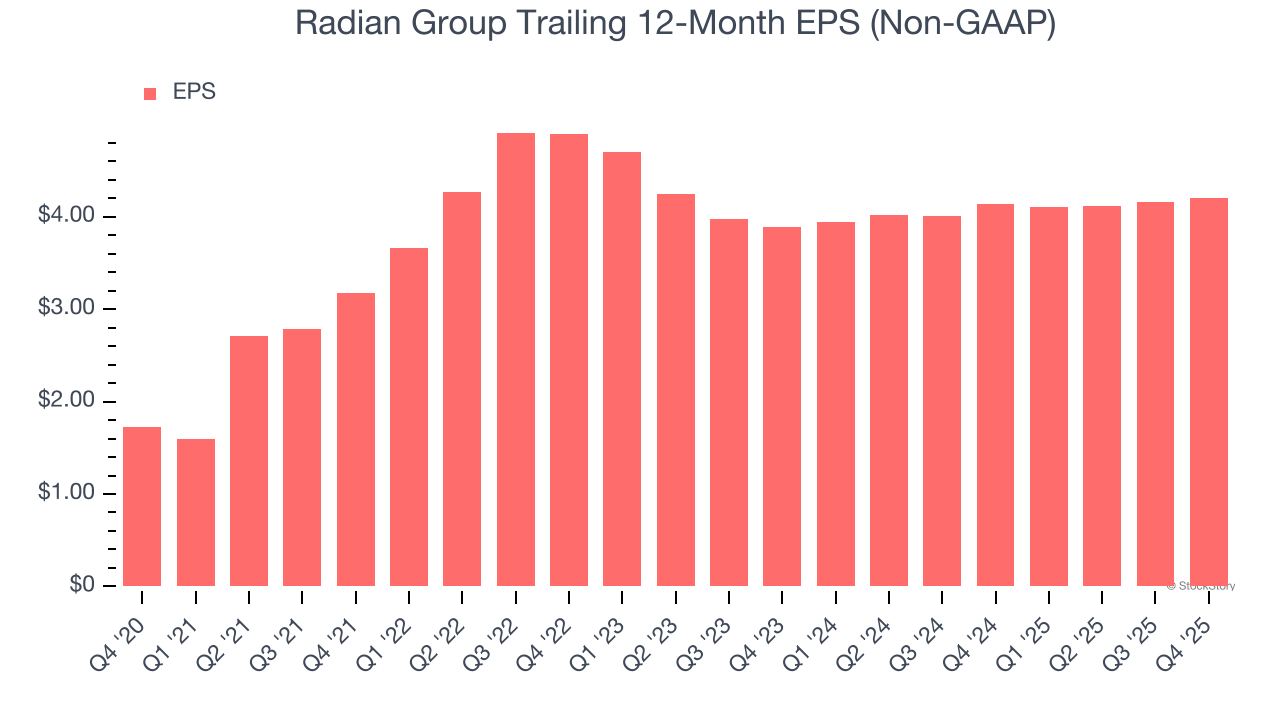

3. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Radian Group’s EPS grew at a weak 3.9% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 1.2% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Final Judgment

Radian Group isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 0.8× forward P/B (or $32.86 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Radian Group

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.