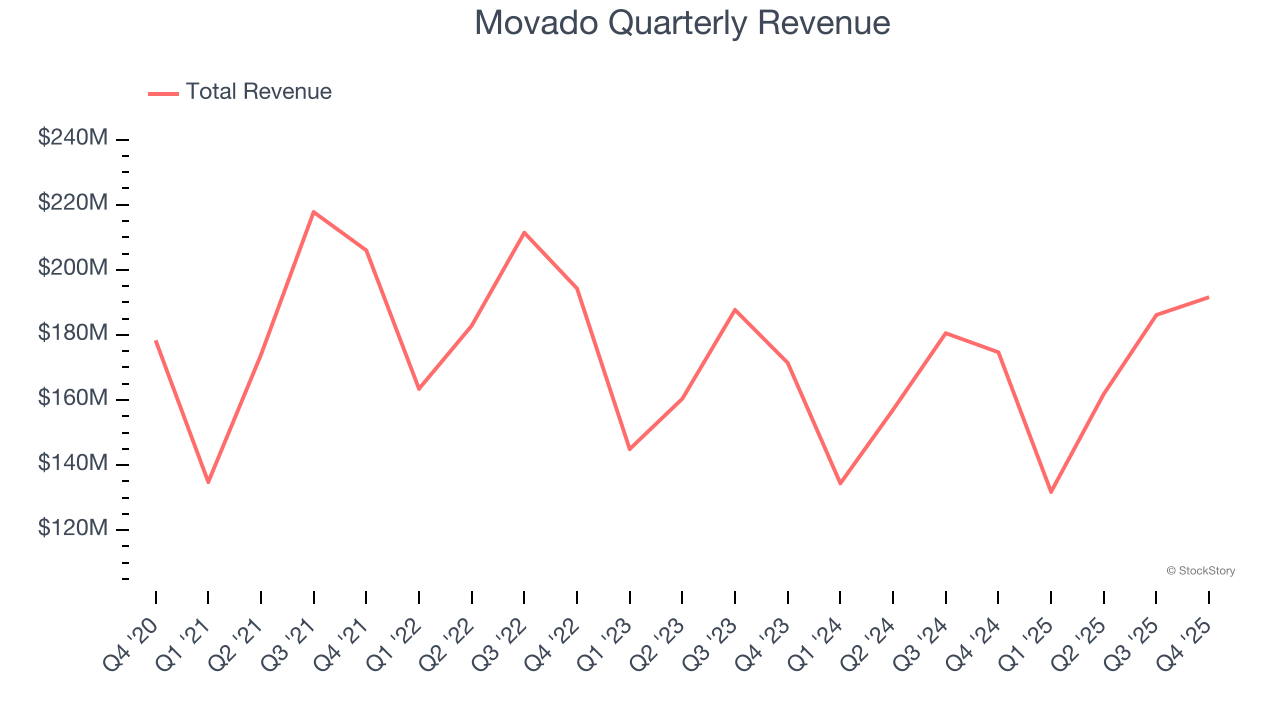

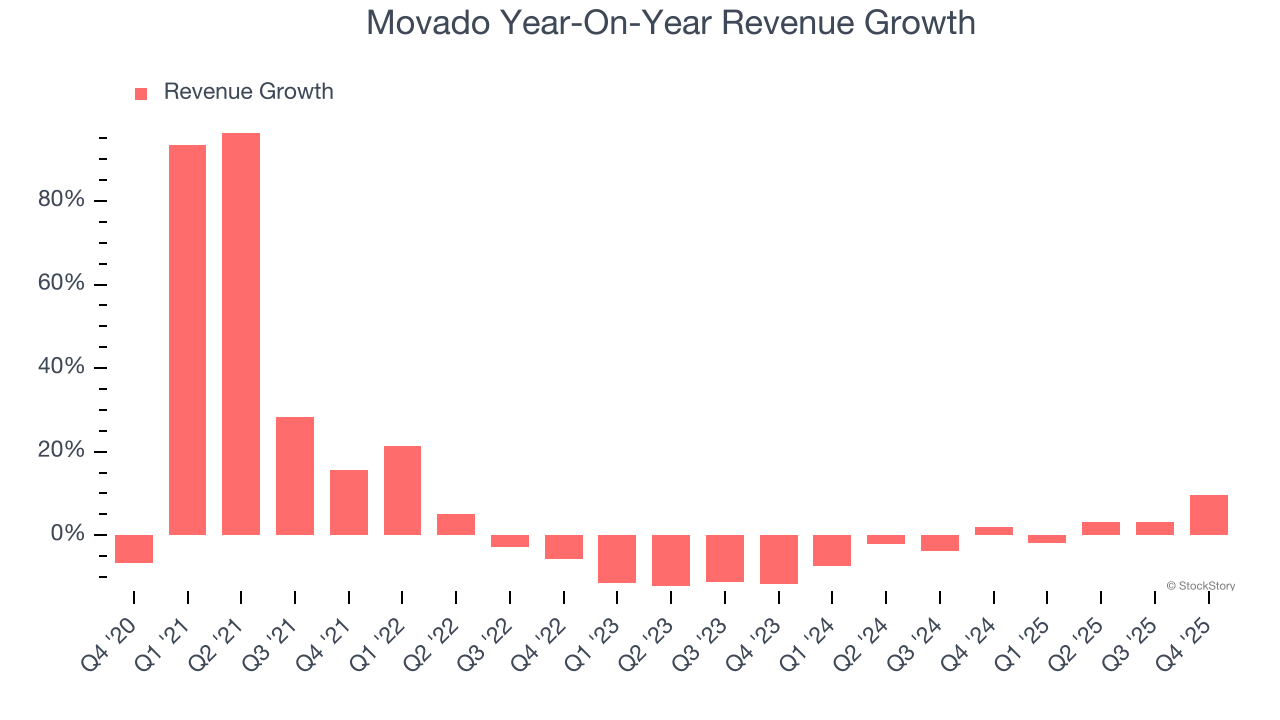

Luxury watch company Movado (NYSE: MOV) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 9.7% year on year to $191.6 million. Its non-GAAP profit of $0.57 per share was 5.6% above analysts’ consensus estimates.

Is now the time to buy Movado? Find out by accessing our full research report, it’s free.

Movado (MOV) Q4 CY2025 Highlights:

- Revenue: $191.6 million vs analyst estimates of $182 million (9.7% year-on-year growth, 5.3% beat)

- Adjusted EPS: $0.57 vs analyst estimates of $0.54 (5.6% beat)

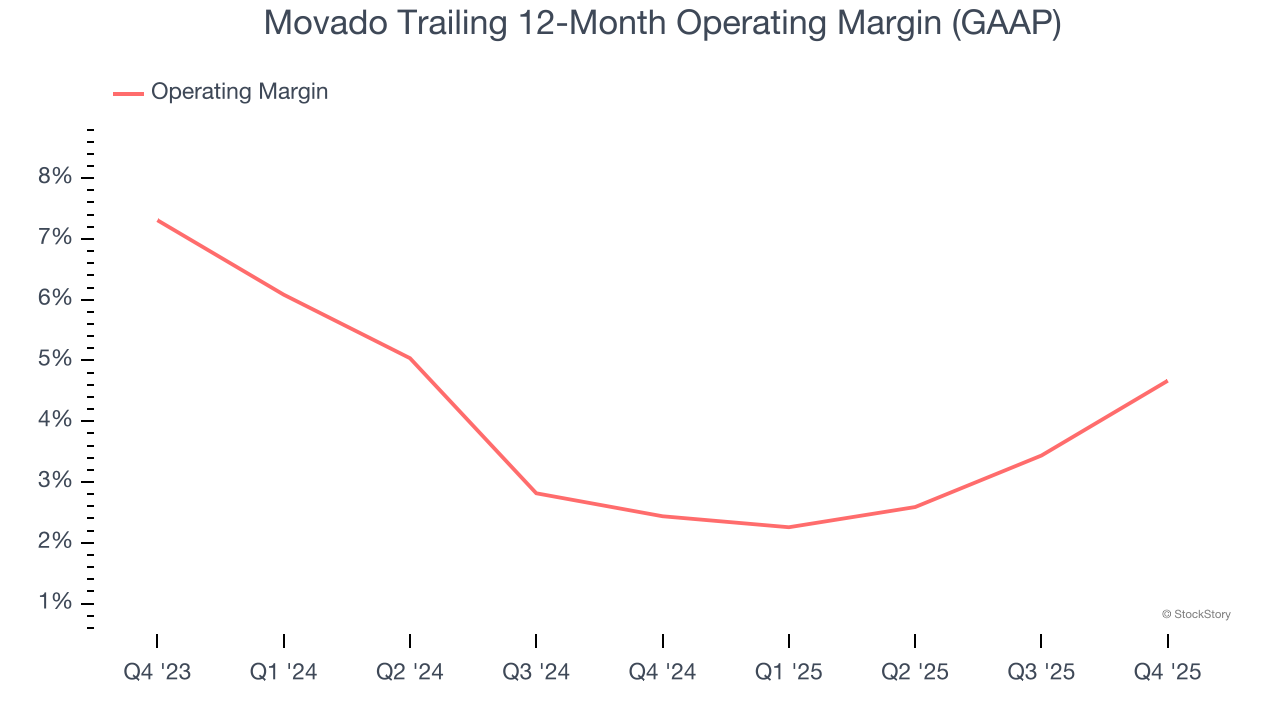

- Operating Margin: 7.2%, up from 2.8% in the same quarter last year

- Free Cash Flow Margin: 29.1%, up from 21.5% in the same quarter last year

- Market Capitalization: $510.3 million

Efraim Grinberg, Chairman and Chief Executive Officer, stated: “Our strong performance in the 4th quarter allowed us to close fiscal 2026 on a high note, delivering strong growth in net sales, a significant increase in profitability and strong positive cash flow generation. Total net sales grew by 5.6%, leading to full-year growth of 2.7% – demonstrating accelerating momentum as the year progressed. These results reflect the power of our global brands, the strength of our innovation, and the successful execution of our strategy by our team.”

Company Overview

With its watches displayed in 20 museums around the world, Movado (NYSE: MOV) is a watchmaking company with a portfolio of watch brands and accessories.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Movado’s 5.8% annualized revenue growth over the last five years was weak. This fell short of our benchmark for the consumer discretionary sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Movado’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Movado reported year-on-year revenue growth of 9.7%, and its $191.6 million of revenue exceeded Wall Street’s estimates by 5.3%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

ONE MORE THING: The $21 AI Application Stock Wall Street Forgot. While Wall Street obsesses over who’s building AI, one company is already using it to print money. And nobody’s paying attention.

AI chip stocks trade at ridiculous valuations. This company processes a trillion consumer signals monthly using AI and trades at a third of the price. The gap won’t last. The institutions will figure it out. You need to see this first. Read the FREE Report Before They Notice.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Movado’s operating margin has risen over the last 12 months and averaged 3.6% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

This quarter, Movado generated an operating margin profit margin of 7.2%, up 4.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

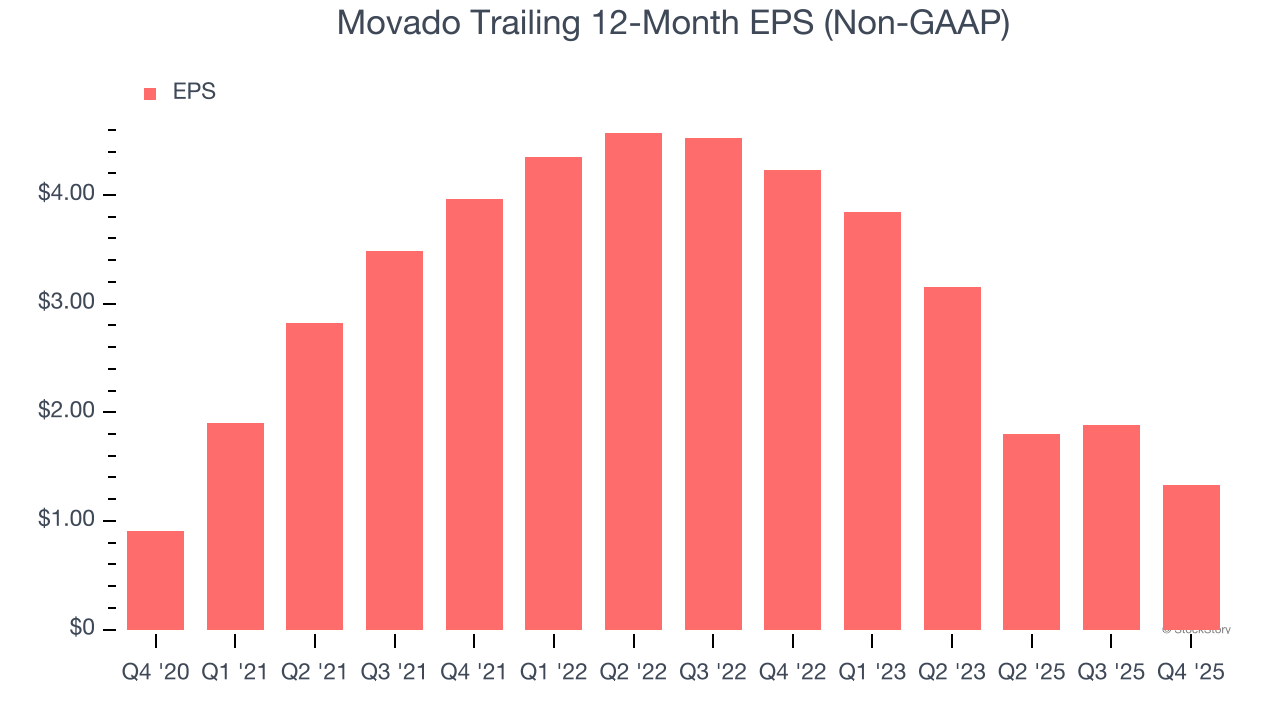

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Movado’s EPS grew at 7.9% compounded annual growth rate over the last five years. This performance was better than its revenue growth but doesn’t tell us much about its business quality because its operating margin improvement was less than peers.

In Q4, Movado reported adjusted EPS of $0.57, down from $1.12 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 5.6%. Over the next 12 months, Wall Street expects Movado’s full-year EPS of $1.33 to grow 15.8%.

Key Takeaways from Movado’s Q4 Results

We enjoyed seeing Movado beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $23.05 immediately after reporting.

So should you invest in Movado right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).