The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how heavy machinery stocks fared in Q4, starting with Terex (NYSE: TEX).

Automation that increases efficiencies and connected equipment that collects analyzable data have been trending, creating new demand for heavy machinery and equipment companies. The gradual transition to clean energy also allows companies to innovate around emissions, potentially spurring replacement cycles that can accelerate revenue growth. On the other hand, heavy machinery companies are at the whim of economic cycles. Interest rates, for example, can greatly impact the commercial and residential construction that drives demand for these companies’ offerings.

The 21 heavy machinery stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 3.8% while next quarter’s revenue guidance was in line.

While some heavy machinery stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.1% since the latest earnings results.

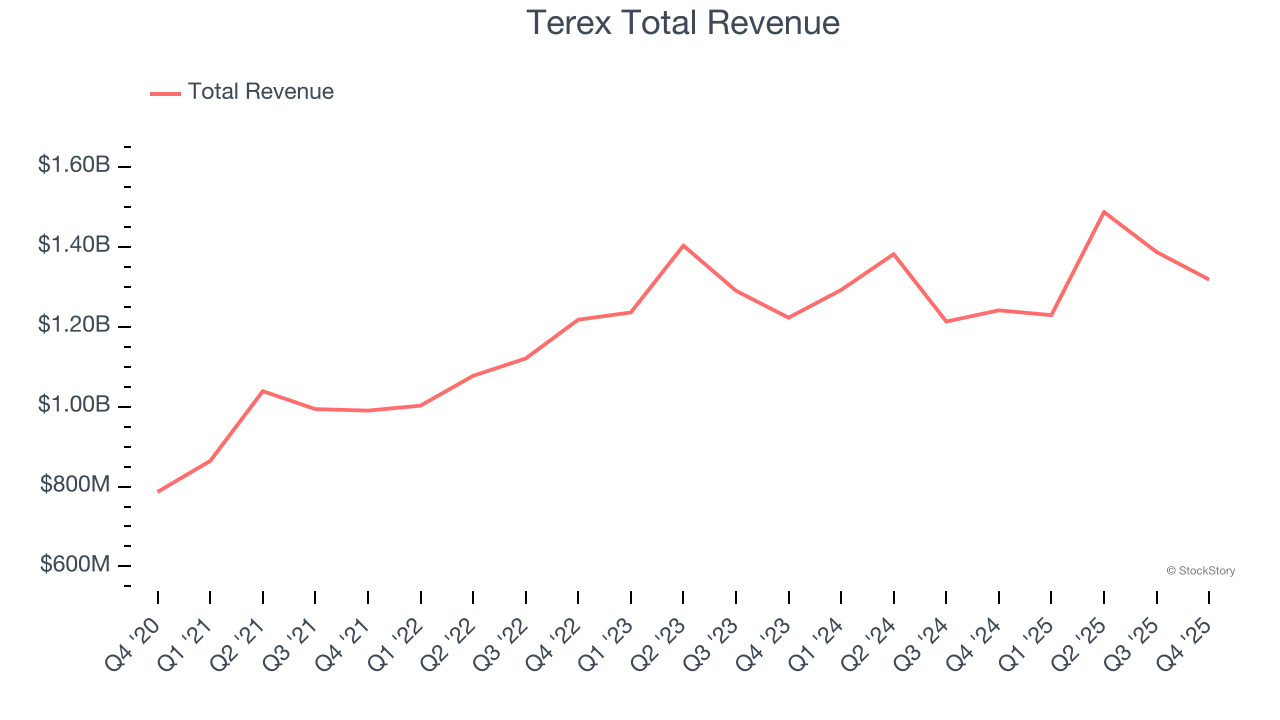

Terex (NYSE: TEX)

With humble beginnings as a dump truck company, Terex (NYSE: TEX) today manufactures lifting and material handling equipment designed to move and hoist heavy goods and materials.

Terex reported revenues of $1.32 billion, up 6.2% year on year. This print exceeded analysts’ expectations by 0.8%. Despite the top-line beat, it was still a mixed quarter for the company with full-year EBITDA guidance exceeding analysts’ expectations but a significant miss of analysts’ EBITDA estimates.

Jennifer Kong-Picarello, Senior Vice President and Chief Financial Officer, said, "I am very pleased that we delivered on all our key 2025 financial expectations, including $325 million of free cash flow reflecting 147% cash conversion. By completing the REV merger, we enter 2026 with even more opportunities to create value for our shareholders. "

Terex delivered the weakest full-year guidance update of the whole group. The market was likely pricing in the results, and the stock is flat since reporting. It currently trades at $59.55.

Is now the time to buy Terex? Access our full analysis of the earnings results here, it’s free.

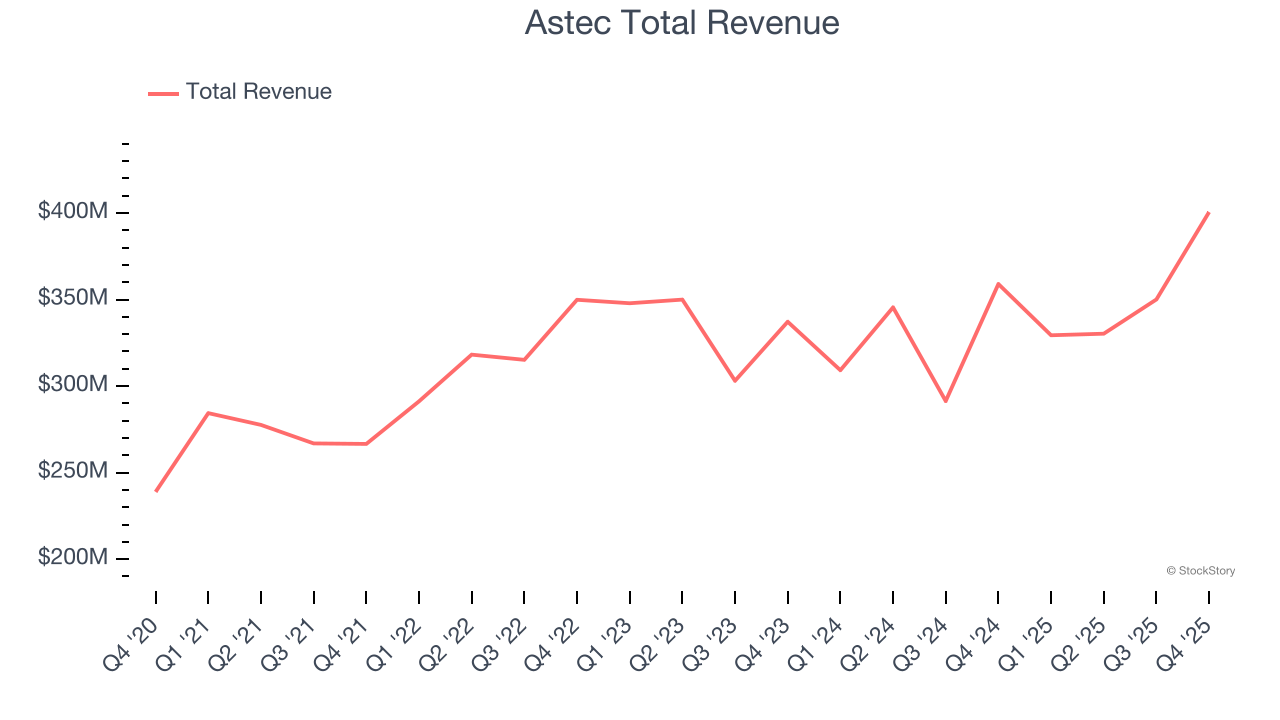

Best Q4: Astec (NASDAQ: ASTE)

Inventing the first ever double-barrel hot-mix asphalt plant, Astec (NASDAQ: ASTE) provides machines and equipment for building roads, processing raw materials, and producing concrete.

Astec reported revenues of $400.6 million, up 11.6% year on year, outperforming analysts’ expectations by 7.1%. The business had an incredible quarter with a beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 9.2% since reporting. It currently trades at $53.12.

Is now the time to buy Astec? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Alamo (NYSE: ALG)

Expanding its markets through acquisitions since its founding, Alamo (NYSE: ALG) designs, manufactures, and services vegetation management and infrastructure maintenance equipment for governmental, industrial, and agricultural use.

Alamo reported revenues of $373.7 million, down 3% year on year, falling short of analysts’ expectations by 7.8%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EBITDA estimates.

Alamo delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 23.6% since the results and currently trades at $166.93.

Read our full analysis of Alamo’s results here.

Deere (NYSE: DE)

Revolutionizing agriculture with the first self-polishing cast-steel plow in the 1800s, Deere (NYSE: DE) manufactures and distributes advanced agricultural, construction, forestry, and turf care equipment.

Deere reported revenues of $9.61 billion, up 13% year on year. This result beat analysts’ expectations by 5.9%. Overall, it was a stunning quarter as it also put up a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

The stock is down 4.1% since reporting and currently trades at $569.12.

Read our full, actionable report on Deere here, it’s free.

Douglas Dynamics (NYSE: PLOW)

Once manufacturing snowplows designed for the iconic jeep vehicle precursor, Douglas Dynamics (NYSE: PLOW) offers snow and ice equipment for the roads and sidewalks.

Douglas Dynamics reported revenues of $184.5 million, up 28.6% year on year. This number surpassed analysts’ expectations by 8.6%. It was an incredible quarter as it also recorded a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ revenue estimates.

Douglas Dynamics scored the fastest revenue growth among its peers. The stock is down 3.3% since reporting and currently trades at $41.25.

Read our full, actionable report on Douglas Dynamics here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.