Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at RTX (NYSE: RTX) and the best and worst performers in the defense contractors industry.

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

The 14 defense contractors stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 2.1% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

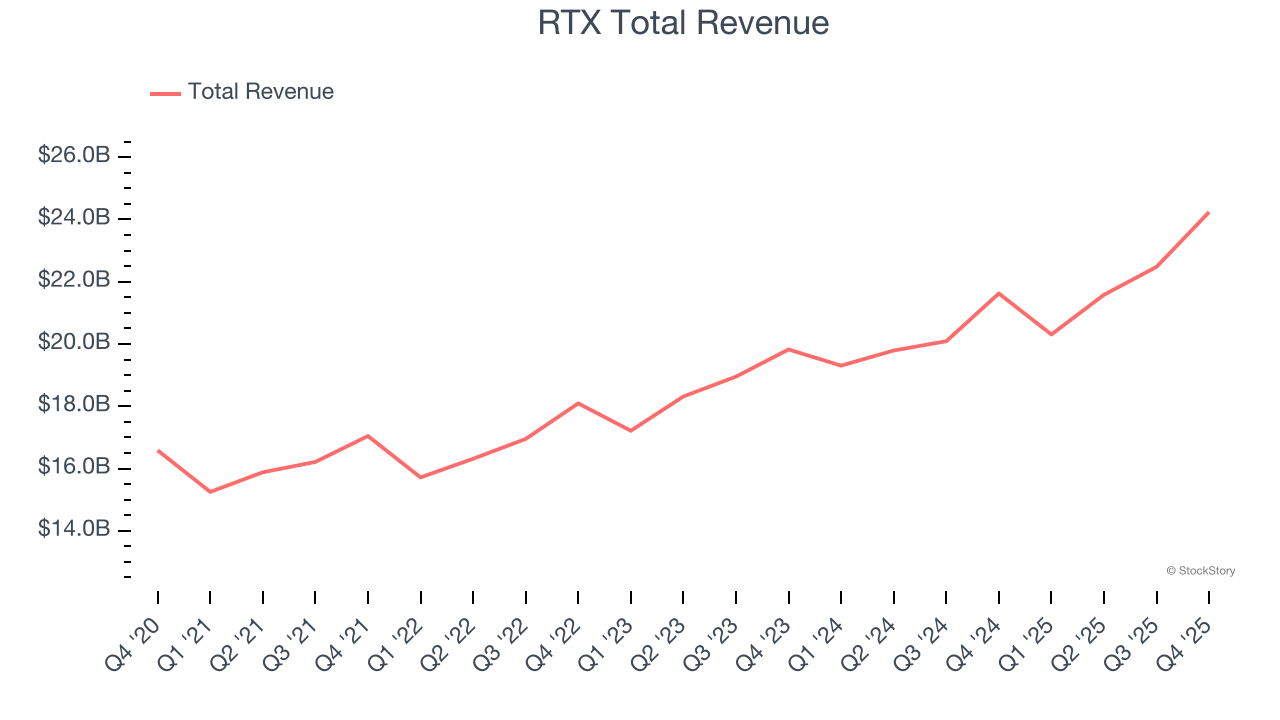

RTX (NYSE: RTX)

Originally focused on refrigeration technology, Raytheon (NSYE:RTX) provides a a variety of products and services to the aerospace and defense industries.

RTX reported revenues of $24.24 billion, up 12.1% year on year. This print exceeded analysts’ expectations by 7%. Overall, it was a very strong quarter for the company with an impressive beat of analysts’ organic revenue estimates and a solid beat of analysts’ EBITDA estimates.

"RTX delivered strong sales, adjusted EPS* and free cash flow* in 2025, enabled by our continued focus on operational performance and execution," said RTX Chairman and CEO Chris Calio.

Interestingly, the stock is up 4.6% since reporting and currently trades at $203.07.

Is now the time to buy RTX? Access our full analysis of the earnings results here, it’s free.

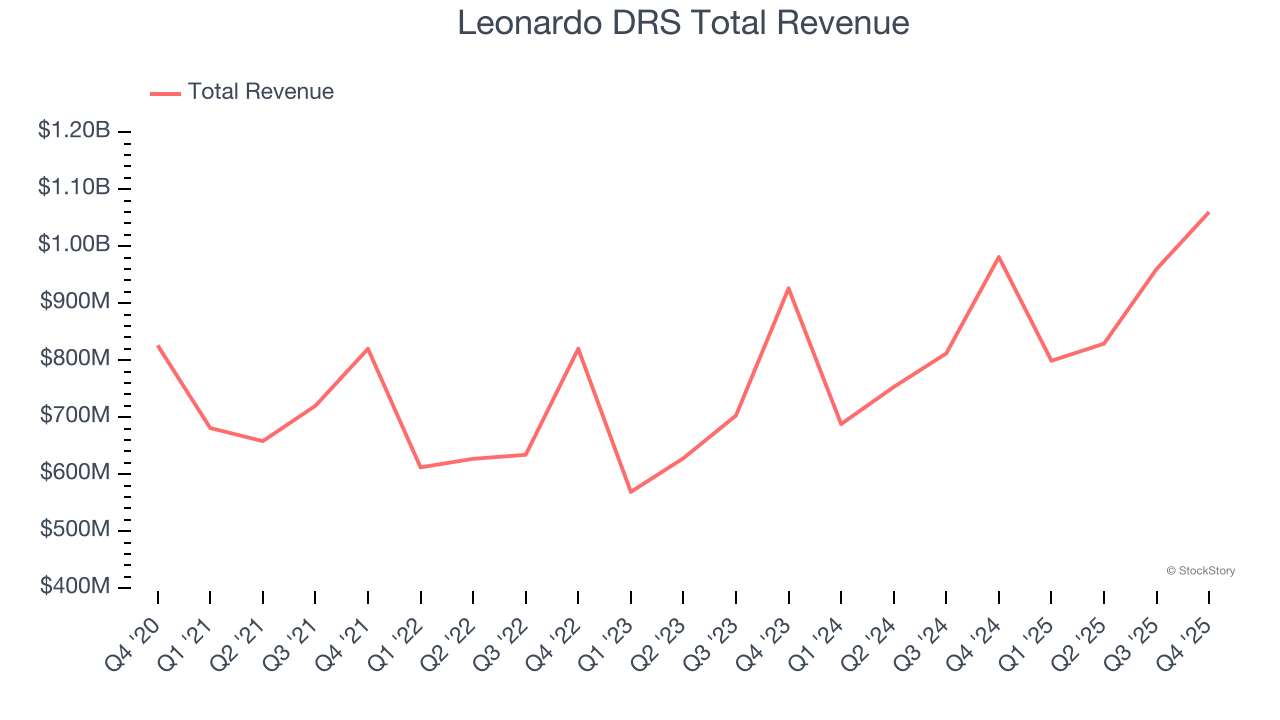

Best Q4: Leonardo DRS (NASDAQ: DRS)

Developing submarine detection systems for the U.S. Navy, Leonardo DRS (NASDAQ: DRS) is a provider of defense systems, electronics, and military support services.

Leonardo DRS reported revenues of $1.06 billion, up 8.1% year on year, outperforming analysts’ expectations by 7%. The business had an exceptional quarter with a solid beat of analysts’ revenue estimates and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 19.4% since reporting. It currently trades at $45.53.

Is now the time to buy Leonardo DRS? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: AeroVironment (NASDAQ: AVAV)

Focused on the future of autonomous military combat, AeroVironment (NASDAQ: AVAV) specializes in advanced unmanned aircraft systems and electric vehicle charging solutions.

AeroVironment reported revenues of $408 million, up 143% year on year, falling short of analysts’ expectations by 14.6%. It was a softer quarter as it posted full-year revenue guidance missing analysts’ expectations significantly and full-year EBITDA guidance missing analysts’ expectations significantly.

AeroVironment delivered the fastest revenue growth but had the weakest performance against analyst estimates in the group. The stock is flat since the results and currently trades at $222.96.

Read our full analysis of AeroVironment’s results here.

Lockheed Martin (NYSE: LMT)

Headquartered in Maryland, Famous for the F-35 aircraft, Lockheed Martin (NYSE: LMT) specializes in defense, space, homeland security, and information technology products.

Lockheed Martin reported revenues of $20.32 billion, up 9.1% year on year. This result topped analysts’ expectations by 2.4%. It was a strong quarter as it also logged an impressive beat of analysts’ revenue estimates and a solid beat of analysts’ adjusted operating income estimates.

The stock is up 6.4% since reporting and currently trades at $635.38.

Read our full, actionable report on Lockheed Martin here, it’s free.

KBR (NYSE: KBR)

Known for projects like the construction of Guantanamo Bay, KBR provides professional services and technologies, specializing in engineering, construction, and government services sectors.

KBR reported revenues of $1.89 billion, down 10.6% year on year. This print missed analysts’ expectations by 2.3%. Taking a step back, it was a mixed quarter as it also produced full-year EBITDA guidance beating analysts’ expectations but a significant miss of analysts’ revenue estimates.

KBR achieved the highest full-year guidance raise but had the slowest revenue growth among its peers. The stock is down 9.2% since reporting and currently trades at $37.06.

Read our full, actionable report on KBR here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.