Origin Bancorp has had an impressive run over the past six months as its shares have beaten the S&P 500 by 13.6%. The stock now trades at $41.28, marking a 16.7% gain. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Origin Bancorp, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Origin Bancorp Not Exciting?

Despite the momentum, we're swiping left on Origin Bancorp for now. Here are three reasons you should be careful with OBK and a stock we'd rather own.

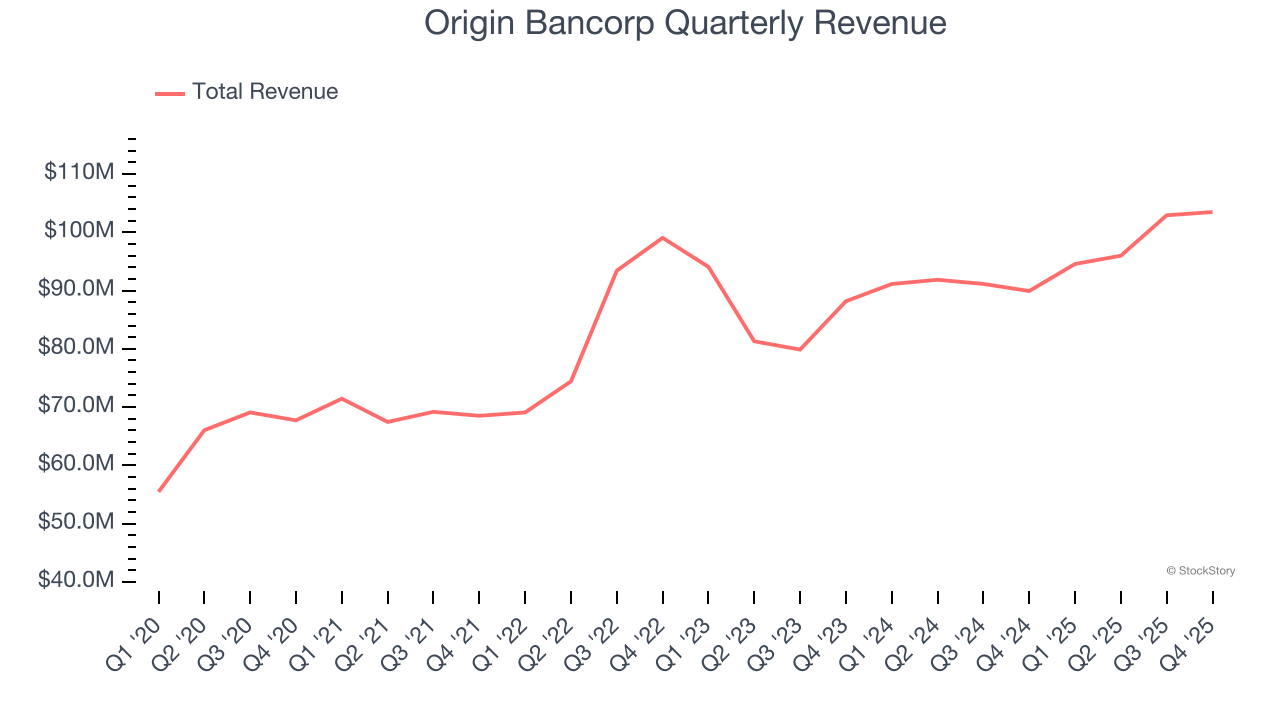

1. Long-Term Revenue Growth Disappoints

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income.

Over the last five years, Origin Bancorp grew its revenue at a mediocre 9% compounded annual growth rate. This was below our standard for the banking sector.

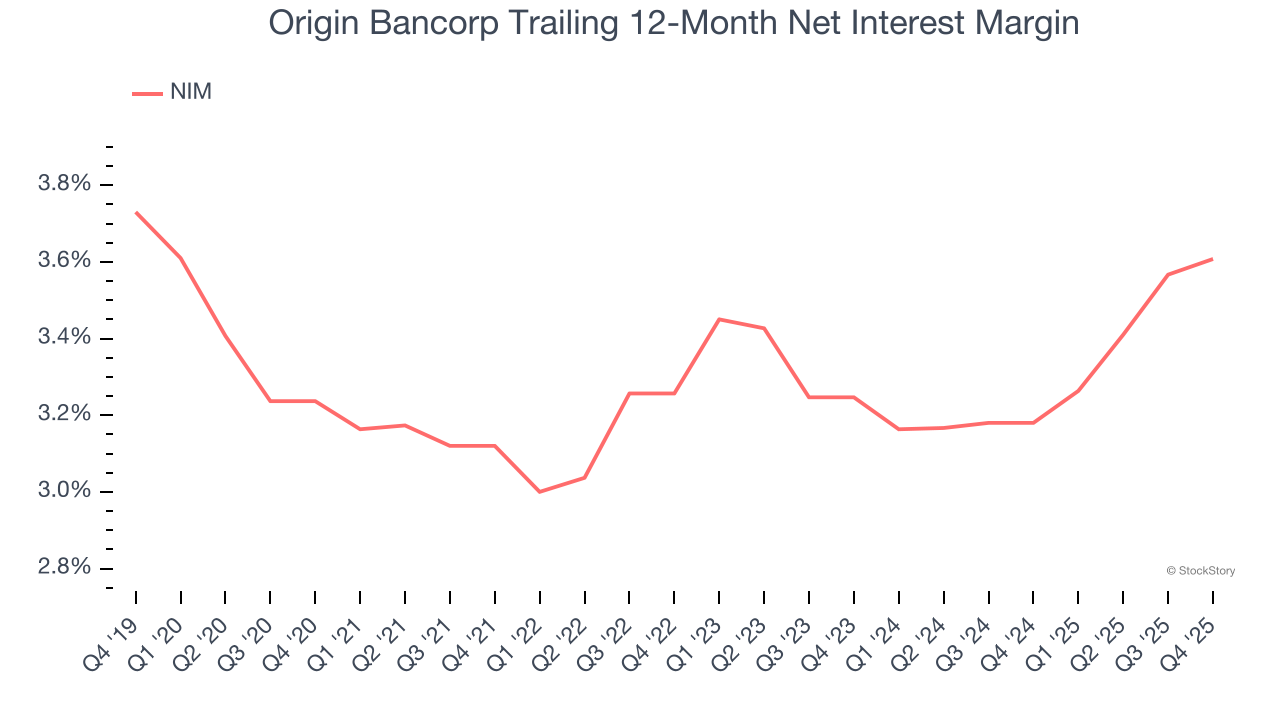

2. Low Net Interest Margin Hinders Flexibility

Net interest margin (NIM) represents how much a bank earns in relation to its outstanding loans. It's one of the most important metrics to track because it shows how a bank's loans are performing and whether it has the ability to command higher premiums for its services.

Over the past two years, we can see that Origin Bancorp’s net interest margin averaged a subpar 3.4%, reflecting its high servicing and capital costs.

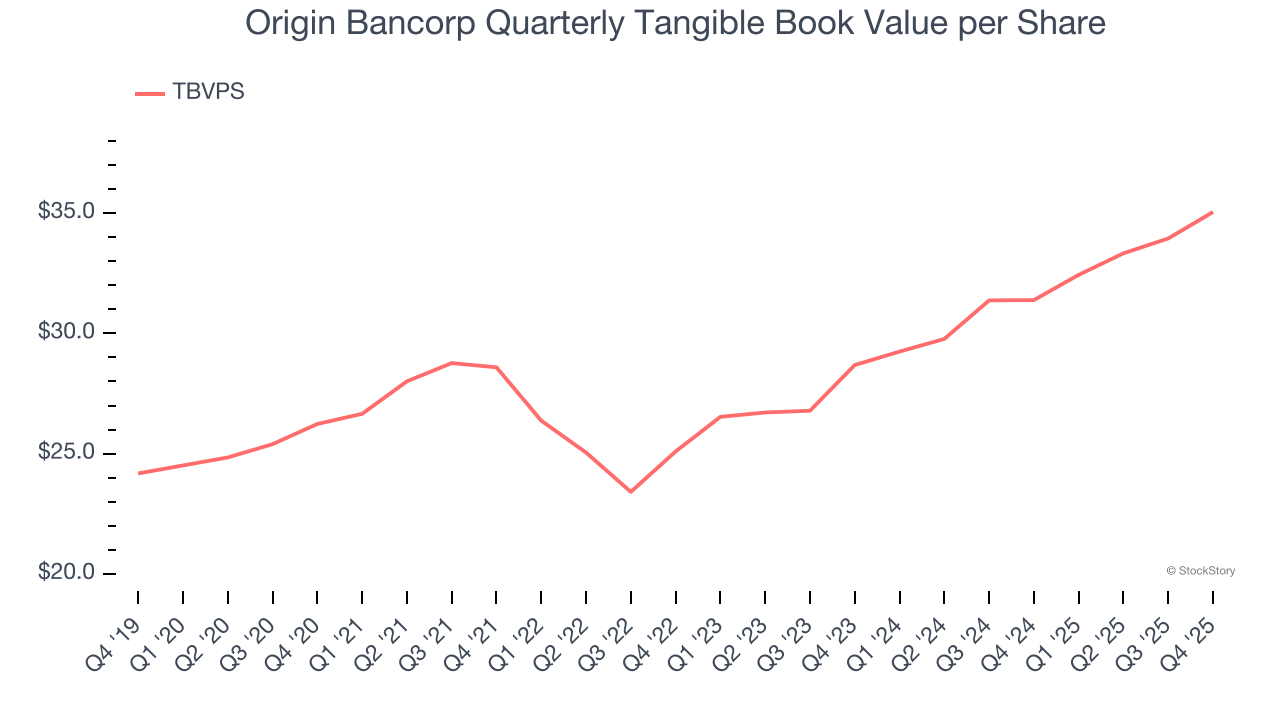

3. Projected TBVPS Growth Is Slim

Tangible book value per share (TBVPS) growth comes from a bank’s ability to profitably lend while maintaining prudent risk management and efficient operations.

Over the next 12 months, Consensus estimates call for Origin Bancorp’s TBVPS to grow by 8.2% to $37.91, paltry growth rate.

Final Judgment

Origin Bancorp isn’t a terrible business, but it doesn’t pass our bar. With its shares beating the market recently, the stock trades at 0.9× forward P/B (or $41.28 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of Origin Bancorp

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.