Columbus McKinnon has had an impressive run over the past six months as its shares have beaten the S&P 500 by 9.2%. The stock now trades at $16.72, marking a 12.3% gain. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Columbus McKinnon, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think Columbus McKinnon Will Underperform?

Despite the momentum, we're swiping left on Columbus McKinnon for now. Here are three reasons you should be careful with CMCO and a stock we'd rather own.

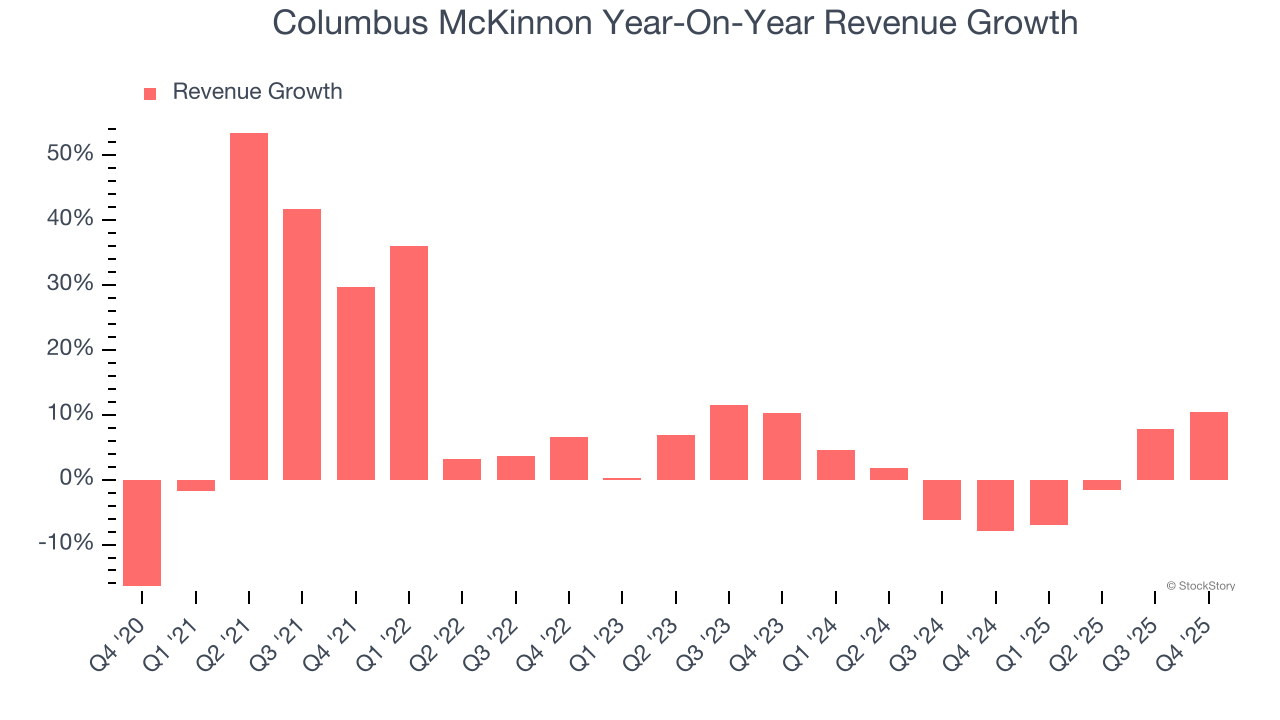

1. Revenue Growth Flatlining

Long-term growth is the most important, but within industrials, a stretched historical view may miss new industry trends or demand cycles. Columbus McKinnon’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

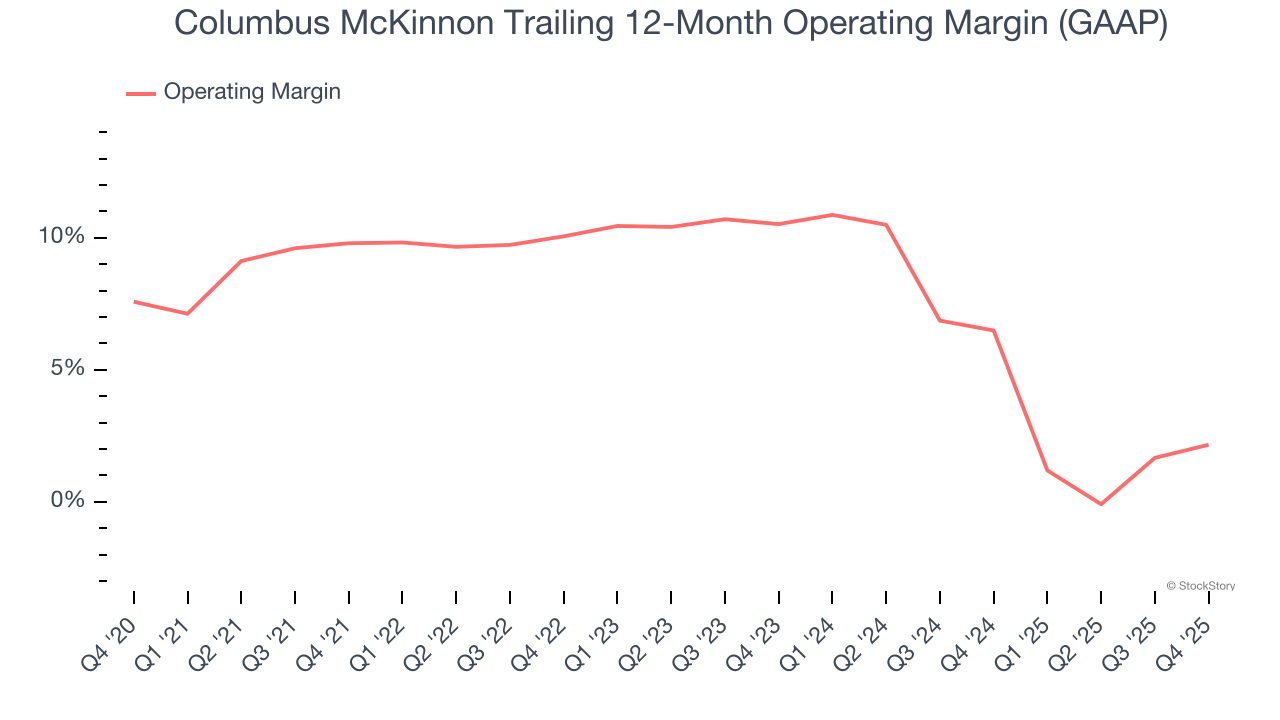

2. Shrinking Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Analyzing the trend in its profitability, Columbus McKinnon’s operating margin decreased by 7.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Columbus McKinnon’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was 2.2%.

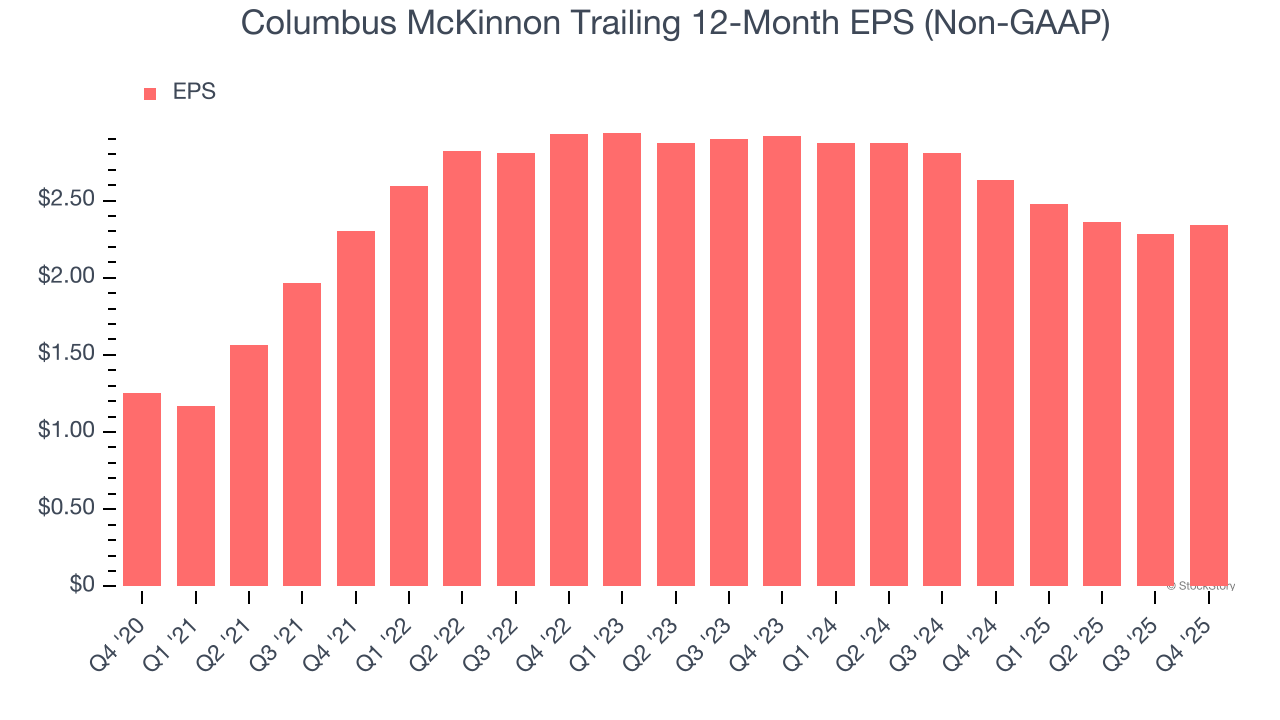

3. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Columbus McKinnon, its EPS declined by 10.5% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

Final Judgment

We see the value of companies helping their customers, but in the case of Columbus McKinnon, we’re out. With its shares beating the market recently, the stock trades at 9.9× forward P/E (or $16.72 per share). While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of Columbus McKinnon

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.