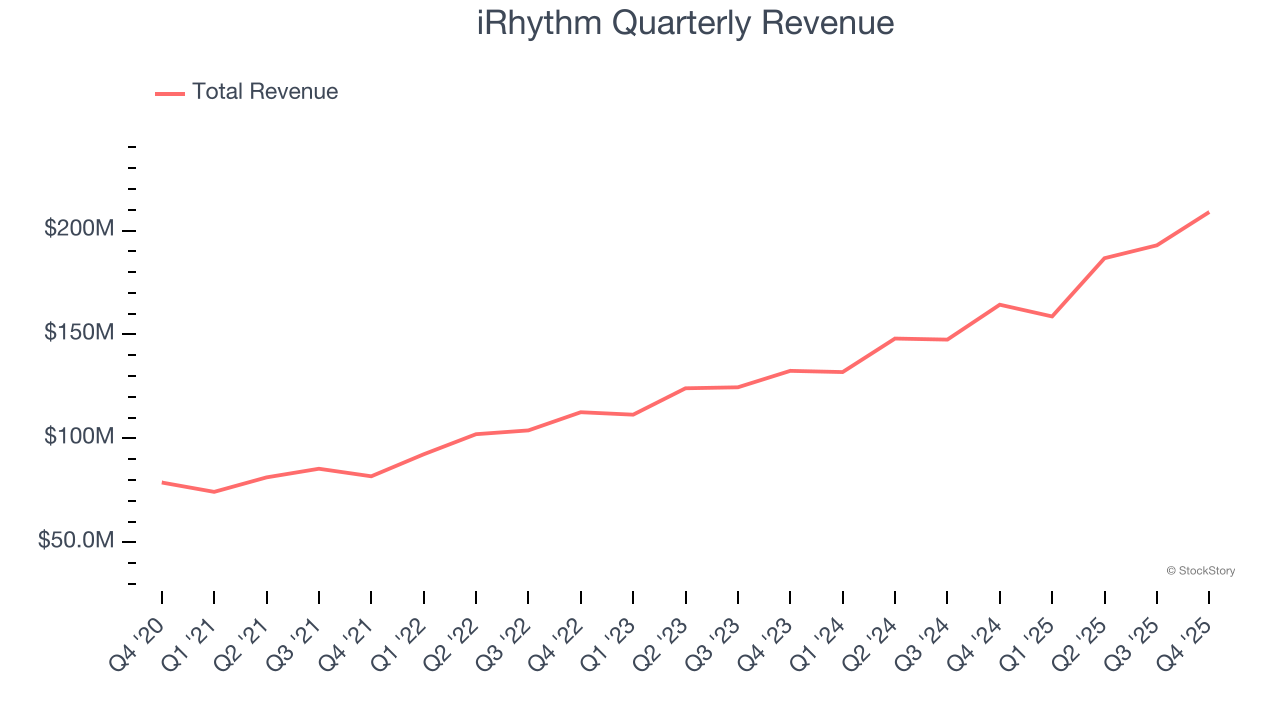

Medical technology company iRhythm Technologies (NASDAQ: IRTC) announced better-than-expected revenue in Q4 CY2025, with sales up 27.1% year on year to $208.9 million. The company’s full-year revenue guidance of $875 million at the midpoint came in 0.6% above analysts’ estimates. Its non-GAAP profit of $0.29 per share was significantly above analysts’ consensus estimates.

Is now the time to buy iRhythm? Find out by accessing our full research report, it’s free.

iRhythm (IRTC) Q4 CY2025 Highlights:

- Revenue: $208.9 million vs analyst estimates of $202 million (27.1% year-on-year growth, 3.4% beat)

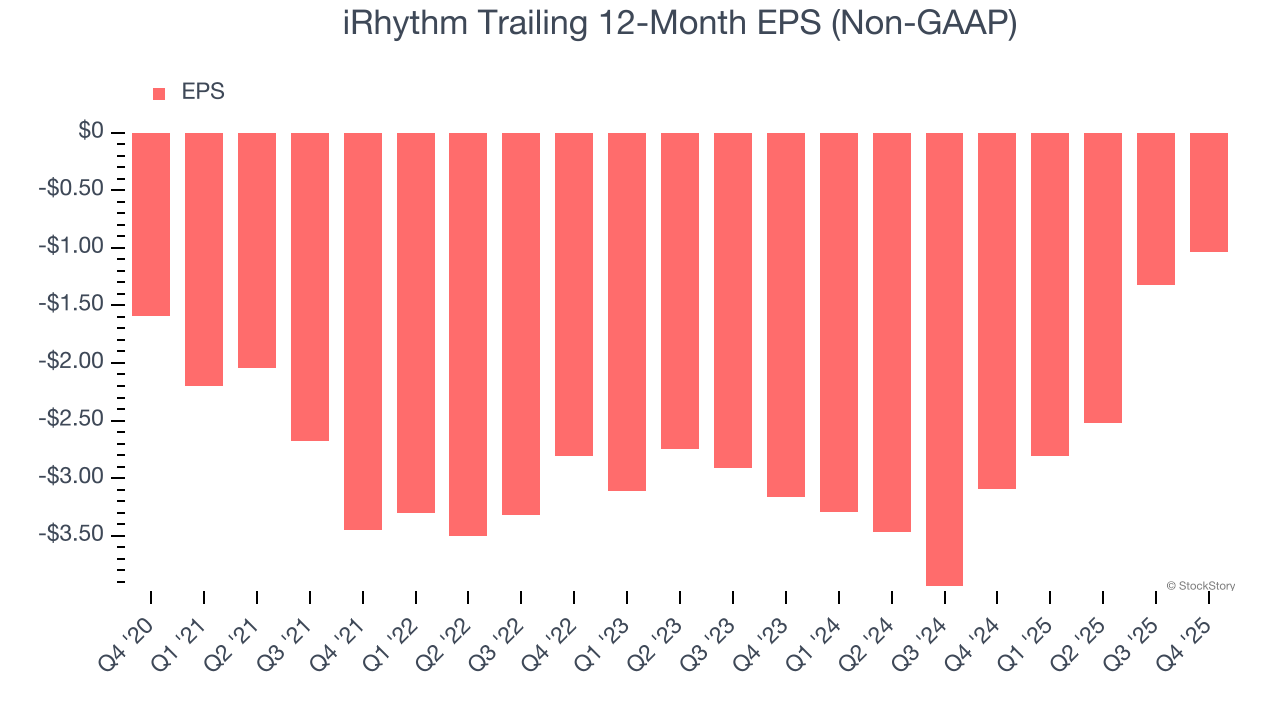

- Adjusted EPS: $0.29 vs analyst estimates of $0.06 (significant beat)

- Adjusted EBITDA: $34.29 million vs analyst estimates of $27.91 million (16.4% margin, 22.9% beat)

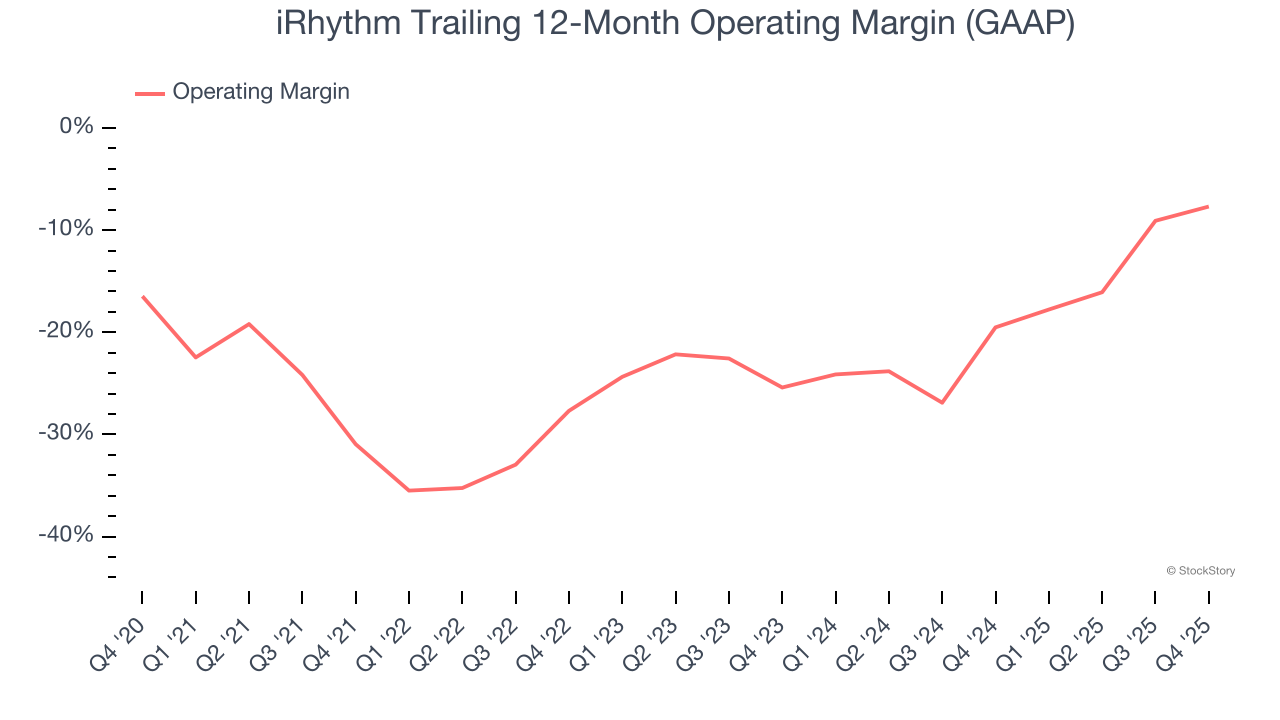

- Operating Margin: 1.1%, up from -2.5% in the same quarter last year

- Market Capitalization: $4.96 billion

“The fourth quarter capped a transformational year for iRhythm,” said Quentin Blackford, President and Chief Executive Officer of iRhythm.

Company Overview

Pioneering the shift from bulky, short-term heart monitors to sleek, wire-free patches, iRhythm Technologies (NASDAQ: IRTC) provides wearable cardiac monitoring devices and AI-powered analysis services that help physicians detect and diagnose heart rhythm disorders.

Revenue Growth

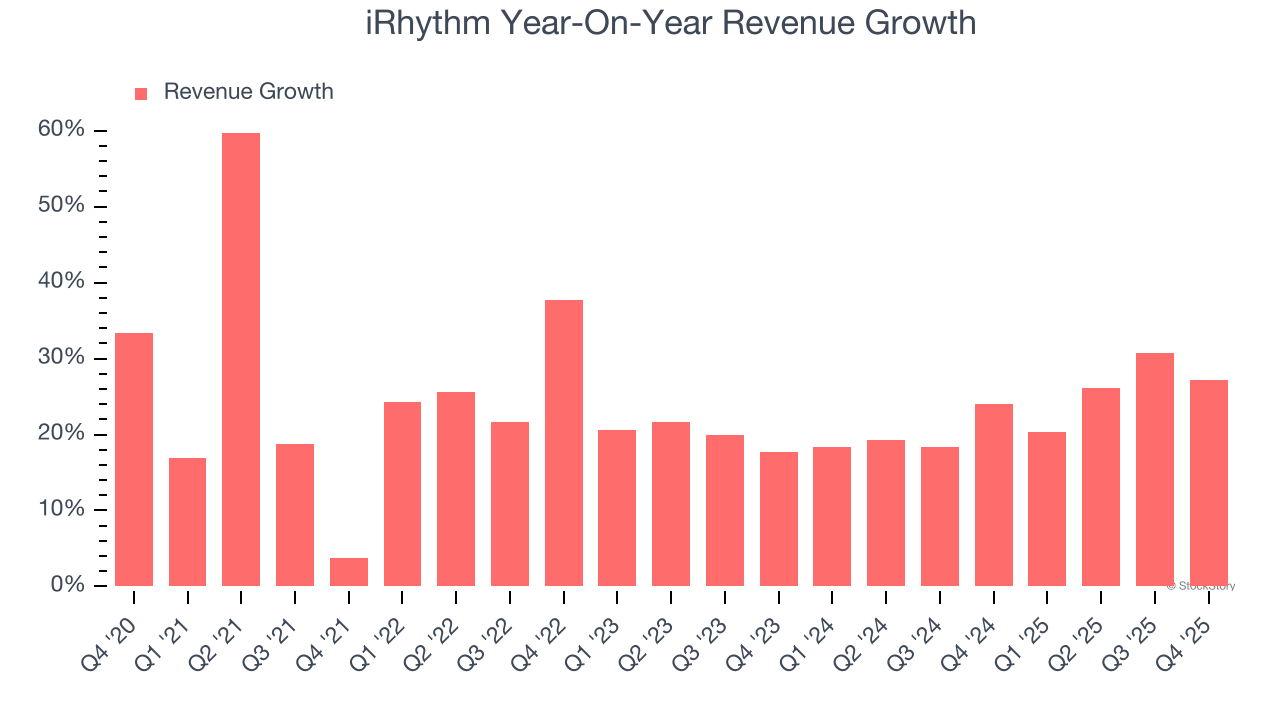

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, iRhythm’s 23% annualized revenue growth over the last five years was excellent. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. iRhythm’s annualized revenue growth of 23.1% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, iRhythm reported robust year-on-year revenue growth of 27.1%, and its $208.9 million of revenue topped Wall Street estimates by 3.4%.

Looking ahead, sell-side analysts expect revenue to grow 15.9% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and implies the market sees success for its products and services.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Although iRhythm was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 20% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, iRhythm’s operating margin rose by 23.3 percentage points over the last five years, as its sales growth gave it operating leverage. Zooming in on its more recent performance, we can see the company’s trajectory is intact as its margin has also increased by 17.7 percentage points on a two-year basis. These data points are very encouraging and show momentum is on its side.

This quarter, iRhythm generated an operating margin profit margin of 1.1%, up 3.6 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although iRhythm’s full-year earnings are still negative, it reduced its losses and improved its EPS by 8.1% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

In Q4, iRhythm reported adjusted EPS of $0.29, up from $0.01 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects iRhythm to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.04 will advance to negative $0.29.

Key Takeaways from iRhythm’s Q4 Results

It was good to see iRhythm beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 1.4% to $160.95 immediately after reporting.

iRhythm may have had a good quarter, but does that mean you should invest right now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).