Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Papa John's (NASDAQ: PZZA) and the best and worst performers in the traditional fast food industry.

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

The 13 traditional fast food stocks we track reported a satisfactory Q3. As a group, revenues were in line with analysts’ consensus estimates.

Thankfully, share prices of the companies have been resilient as they are up 9.1% on average since the latest earnings results.

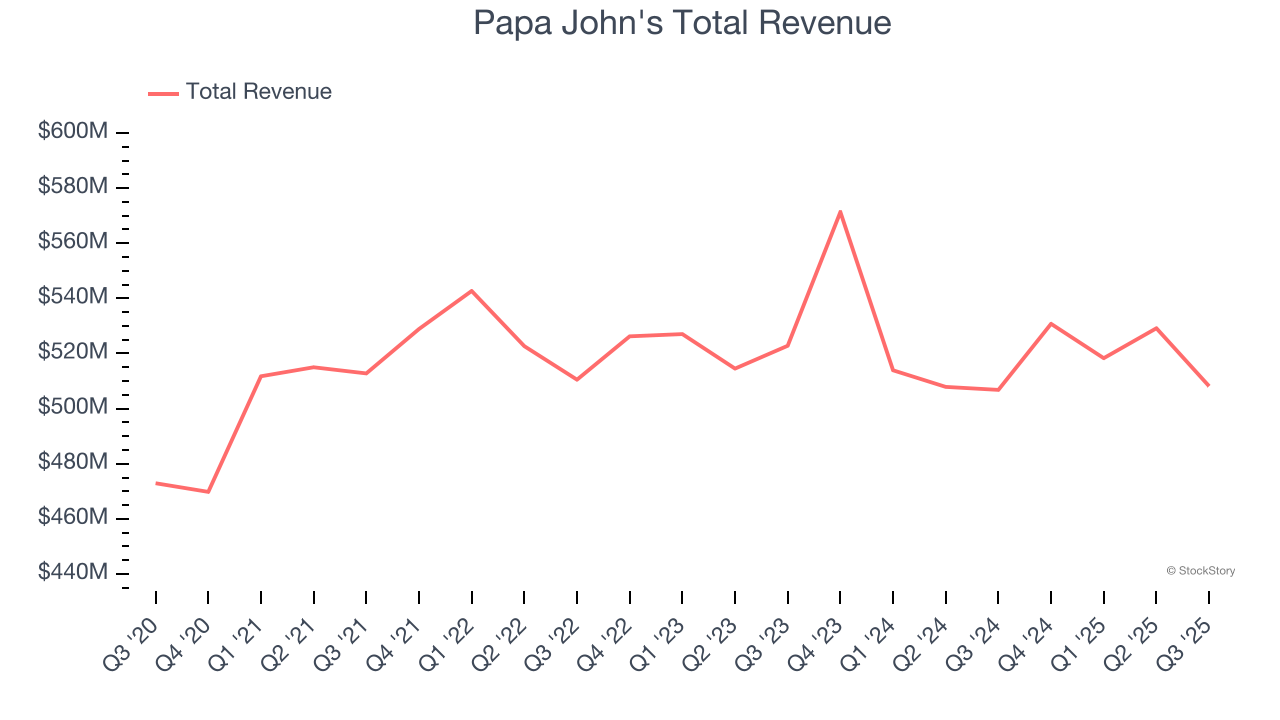

Weakest Q3: Papa John's (NASDAQ: PZZA)

Founded by the eclectic John “Papa John” Schnatter, Papa John’s (NASDAQ: PZZA) is a globally recognized pizza delivery and carryout chain known for “better ingredients” and “better pizza”.

Papa John's reported revenues of $508.2 million, flat year on year. This print fell short of analysts’ expectations by 2.9%. Overall, it was a disappointing quarter for the company with full-year EBITDA guidance missing analysts’ expectations and a miss of analysts’ revenue estimates.

Unsurprisingly, the stock is down 12.2% since reporting and currently trades at $36.24.

Read our full report on Papa John's here, it’s free.

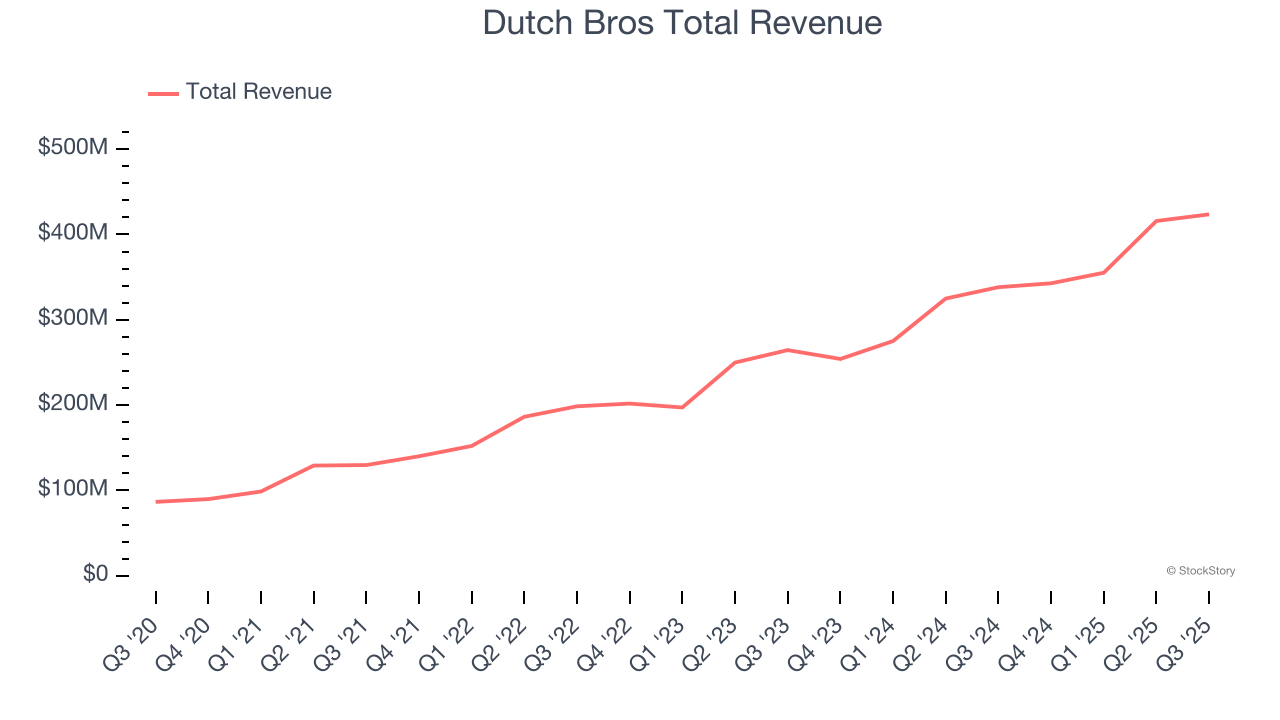

Best Q3: Dutch Bros (NYSE: BROS)

Started in 1992 by two brothers as a single pushcart, Dutch Bros (NYSE: BROS) is a dynamic coffee chain that’s captured the hearts of coffee enthusiasts across the United States.

Dutch Bros reported revenues of $423.6 million, up 25.2% year on year, outperforming analysts’ expectations by 2.3%. The business had an exceptional quarter with an impressive beat of analysts’ same-store sales estimates and a solid beat of analysts’ revenue estimates.

Dutch Bros scored the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 10.5% since reporting. It currently trades at $62.11.

Is now the time to buy Dutch Bros? Access our full analysis of the earnings results here, it’s free.

Jack in the Box (NASDAQ: JACK)

Delighting customers since its inception in 1951, Jack in the Box (NASDAQ: JACK) is a distinctive fast-food chain known for its bold flavors, innovative menu items, and quirky marketing.

Jack in the Box reported revenues of $326.2 million, down 6.6% year on year, exceeding analysts’ expectations by 2.5%. Still, it was a softer quarter as it posted full-year EBITDA guidance missing analysts’ expectations significantly and a significant miss of analysts’ EPS estimates.

Jack in the Box delivered the slowest revenue growth in the group. Interestingly, the stock is up 59.7% since the results and currently trades at $22.97.

Read our full analysis of Jack in the Box’s results here.

Yum China (NYSE: YUMC)

One of China’s largest restaurant companies, Yum China (NYSE: YUMC) is an independent entity spun off from Yum! Brands in 2016.

Yum China reported revenues of $3.21 billion, up 4.4% year on year. This result was in line with analysts’ expectations. More broadly, it was a mixed quarter as it failed to impress in some other areas of the business.

The stock is up 8.7% since reporting and currently trades at $47.80.

Read our full, actionable report on Yum China here, it’s free.

Wendy's (NASDAQ: WEN)

Founded by Dave Thomas in 1969, Wendy’s (NASDAQ: WEN) is a renowned fast-food chain known for its fresh, never-frozen beef burgers, flavorful menu options, and commitment to quality.

Wendy's reported revenues of $549.5 million, down 3% year on year. This print beat analysts’ expectations by 3.1%. Overall, it was an exceptional quarter as it also put up a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ revenue estimates.

Wendy's achieved the biggest analyst estimates beat among its peers. The stock is down 5.3% since reporting and currently trades at $8.36.

Read our full, actionable report on Wendy's here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.