Over the past six months, Caesars Entertainment’s stock price fell to $25.75. Shareholders have lost 6.6% of their capital, which is disappointing considering the S&P 500 has climbed by 17.5%. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Caesars Entertainment, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Caesars Entertainment Not Exciting?

Even though the stock has become cheaper, we don't have much confidence in Caesars Entertainment. Here are three reasons why CZR doesn't excite us and a stock we'd rather own.

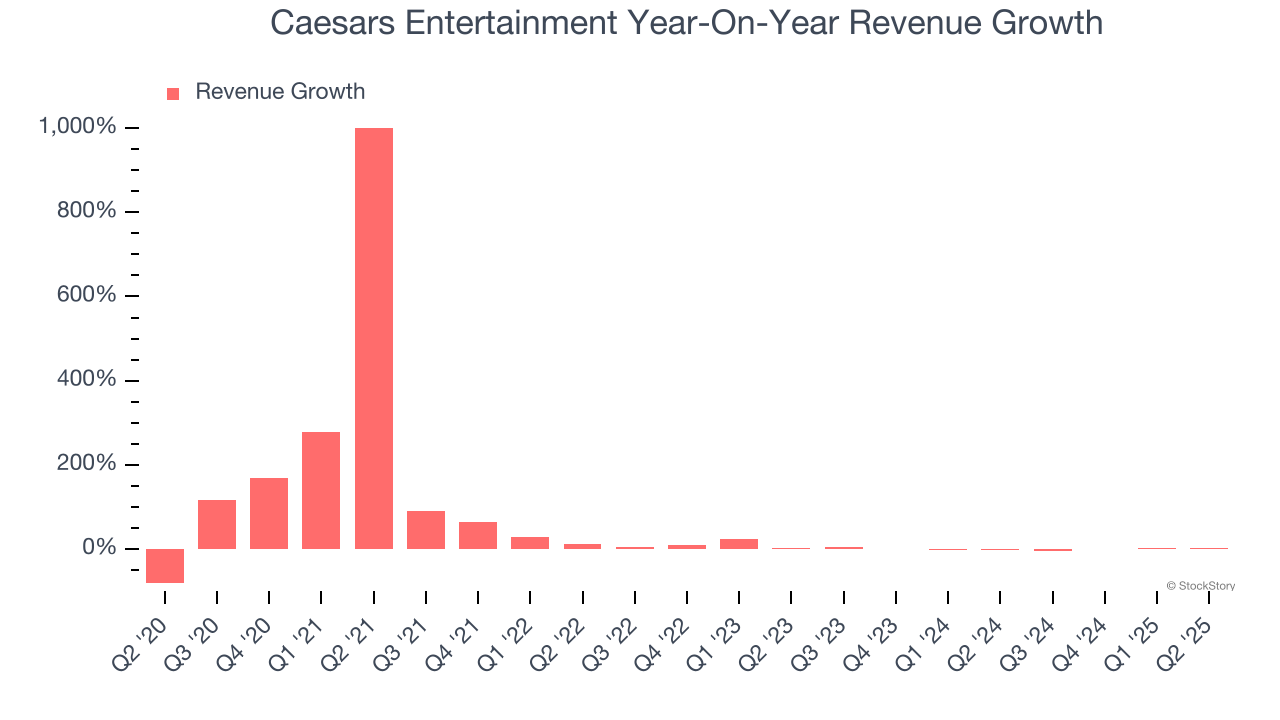

1. Revenue Growth Flatlining

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Caesars Entertainment’s recent performance shows its demand has slowed significantly as its revenue was flat over the last two years. Note that COVID hurt Caesars Entertainment’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

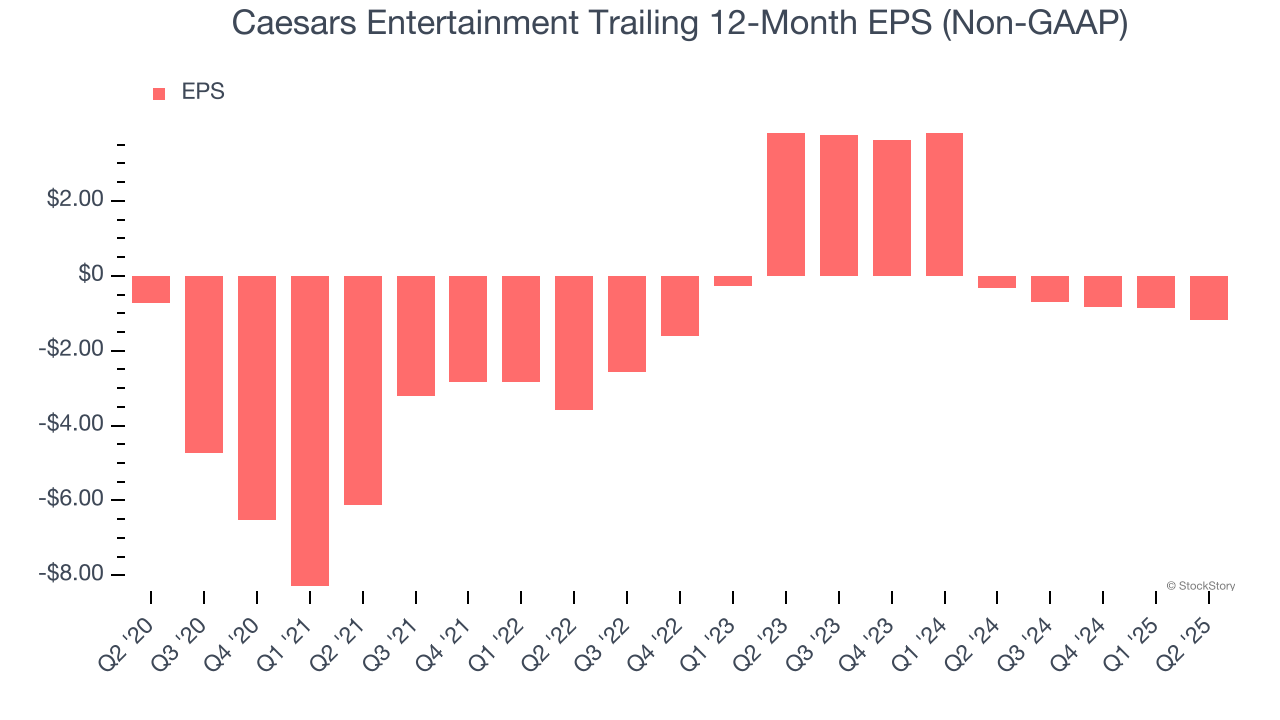

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Caesars Entertainment’s earnings losses deepened over the last five years as its EPS dropped 10% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, Caesars Entertainment’s low margin of safety could leave its stock price susceptible to large downswings.

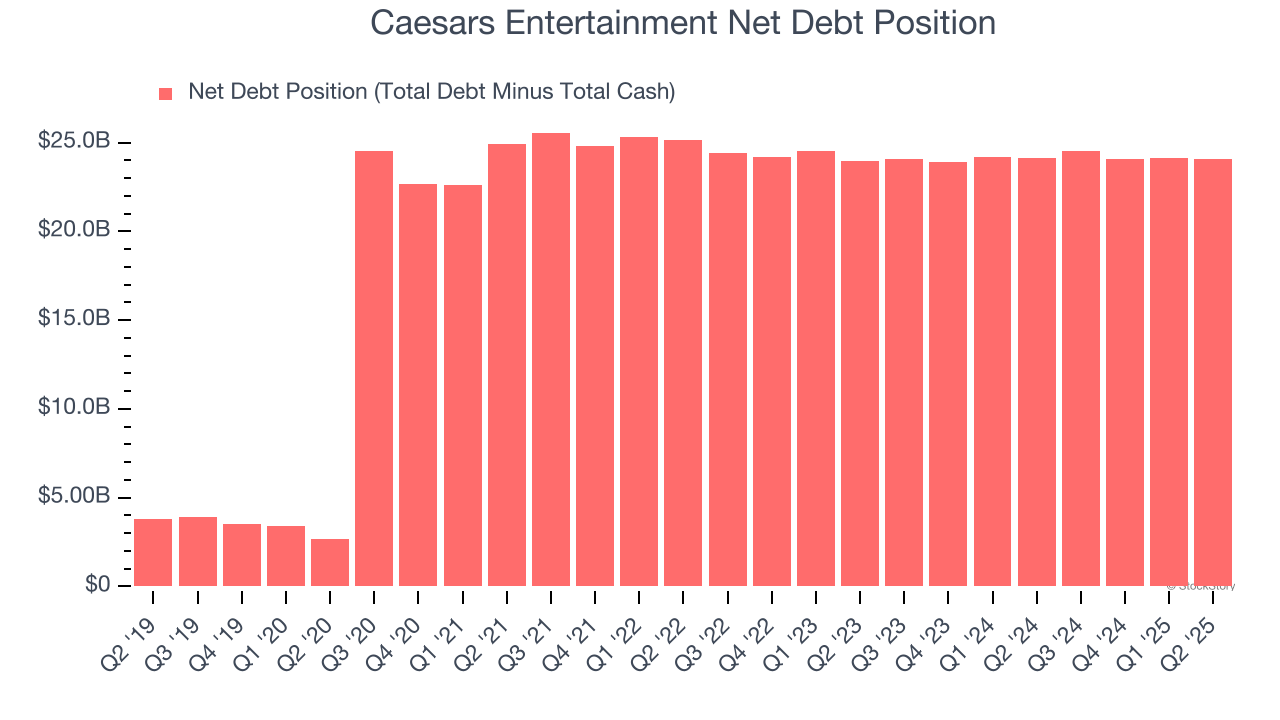

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Caesars Entertainment’s $25.16 billion of debt exceeds the $1.07 billion of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $3.72 billion over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Caesars Entertainment could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Caesars Entertainment can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

Caesars Entertainment’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 31× forward P/E (or $25.75 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward an all-weather company that owns household favorite Taco Bell.

High-Quality Stocks for All Market Conditions

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.