As the Q1 earnings season wraps, let’s dig into this quarter’s best and worst performers in the beauty and cosmetics retailer industry, including Bath and Body Works (NYSE: BBWI) and its peers.

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

The 4 beauty and cosmetics retailer stocks we track reported a mixed Q1. As a group, revenues along with next quarter’s revenue guidance were in line with analysts’ consensus estimates.

Luckily, beauty and cosmetics retailer stocks have performed well with share prices up 21.4% on average since the latest earnings results.

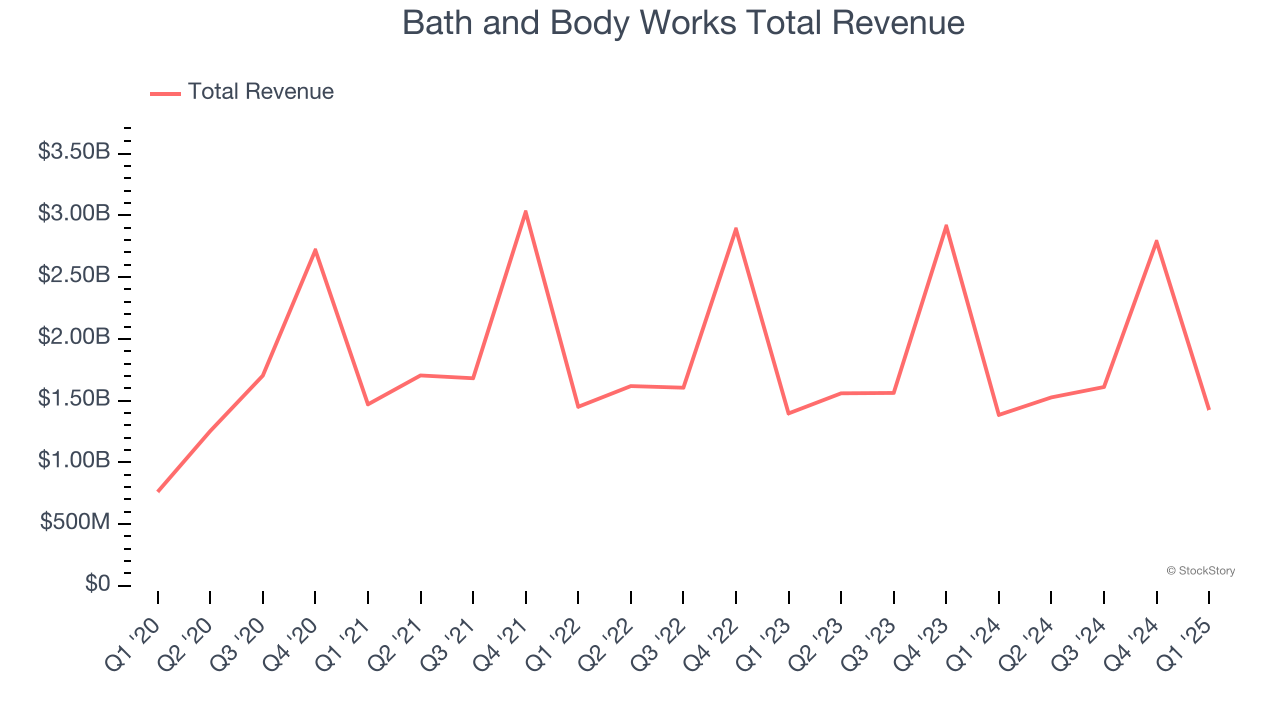

Weakest Q1: Bath and Body Works (NYSE: BBWI)

Spun off from L Brands in 2020, Bath & Body Works (NYSE: BBWI) is a personal care and home fragrance retailer where consumers can find specialty shower gels, scented candles for the home, and lotions.

Bath and Body Works reported revenues of $1.42 billion, up 2.9% year on year. This print was in line with analysts’ expectations, but overall, it was a slower quarter for the company with EPS guidance for next quarter missing analysts’ expectations.

Daniel Heaf, CEO of Bath & Body Works, commented, “I’m honored to join this iconic brand with a deep sense of purpose and a powerful foundation. I have already had the privilege of meeting many associates across the company, and I’m incredibly impressed by the passion, dedication, and talent across our teams. I believe we’re incredibly well positioned to define and lead the home fragrance and beauty categories globally and accelerate growth.”

Interestingly, the stock is up 8.8% since reporting and currently trades at $33.14.

Read our full report on Bath and Body Works here, it’s free.

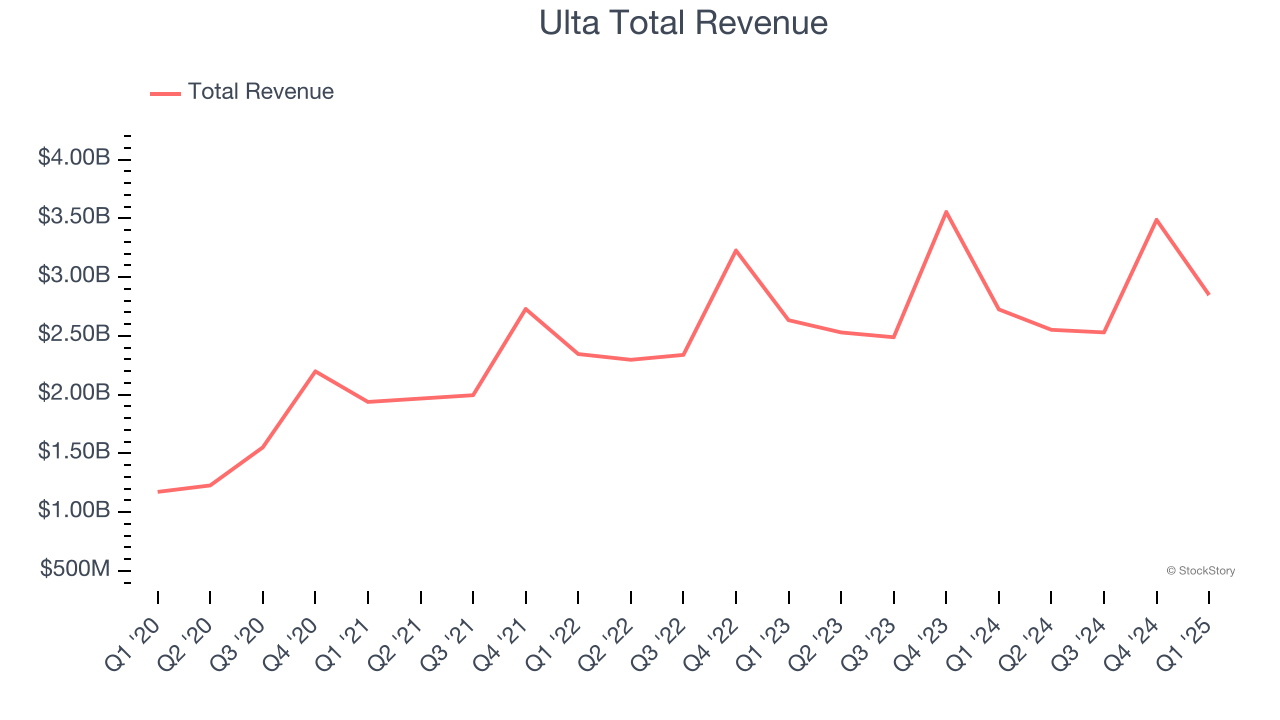

Best Q1: Ulta (NASDAQ: ULTA)

Offering high-end prestige brands as well as lower-priced, mass-market ones, Ulta Beauty (NASDAQ: ULTA) is an American retailer that sells makeup, skincare, haircare, and fragrance products.

Ulta reported revenues of $2.85 billion, up 4.5% year on year, outperforming analysts’ expectations by 1.9%. The business had a strong quarter with an impressive beat of analysts’ EBITDA estimates and a solid beat of analysts’ EPS estimates.

Ulta delivered the biggest analyst estimates beat and highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 13.3% since reporting. It currently trades at $478.34.

Is now the time to buy Ulta? Access our full analysis of the earnings results here, it’s free.

Sally Beauty (NYSE: SBH)

Catering to both everyday consumers as well as salon professionals, Sally Beauty (NYSE: SBH) is a retailer that sells salon-quality beauty products such as makeup and haircare products.

Sally Beauty reported revenues of $883.1 million, down 2.8% year on year, falling short of analysts’ expectations by 2%. It was a mixed quarter as it posted a narrow beat of analysts’ gross margin estimates.

Sally Beauty delivered the weakest performance against analyst estimates and slowest revenue growth in the group. Interestingly, the stock is up 25.7% since the results and currently trades at $10.28.

Read our full analysis of Sally Beauty’s results here.

Warby Parker (NYSE: WRBY)

Founded in 2010, Warby Parker (NYSE: WRBY) designs, manufactures, and sells eyewear, including prescription glasses, sunglasses, and contact lenses, through its e-commerce platform and physical retail locations.

Warby Parker reported revenues of $223.8 million, up 11.9% year on year. This number missed analysts’ expectations by 0.8%. More broadly, it was actually a strong quarter as it recorded a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Warby Parker scored the fastest revenue growth but had the weakest full-year guidance update among its peers. The stock is up 37.8% since reporting and currently trades at $22.24.

Read our full, actionable report on Warby Parker here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.