As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the industrial distributors industry, including GMS (NYSE: GMS) and its peers.

Supply chain and inventory management are themes that grew in focus after COVID wreaked havoc on the global movement of raw materials and components. Distributors that boast a reliable selection of products–everything from hardhats and fasteners for jet engines to ceiling systems–and quickly deliver goods to customers can benefit from this theme. While e-commerce hasn’t disrupted industrial distribution as much as consumer retail, it is still a real threat, forcing investment in omnichannel capabilities to better interact with customers. Additionally, distributors are at the whim of economic cycles that impact the capital spending and construction projects that can juice demand.

The 29 industrial distributors stocks we track reported a slower Q3. As a group, revenues beat analysts’ consensus estimates by 0.6%.

Thankfully, share prices of the companies have been resilient as they are up 8.3% on average since the latest earnings results.

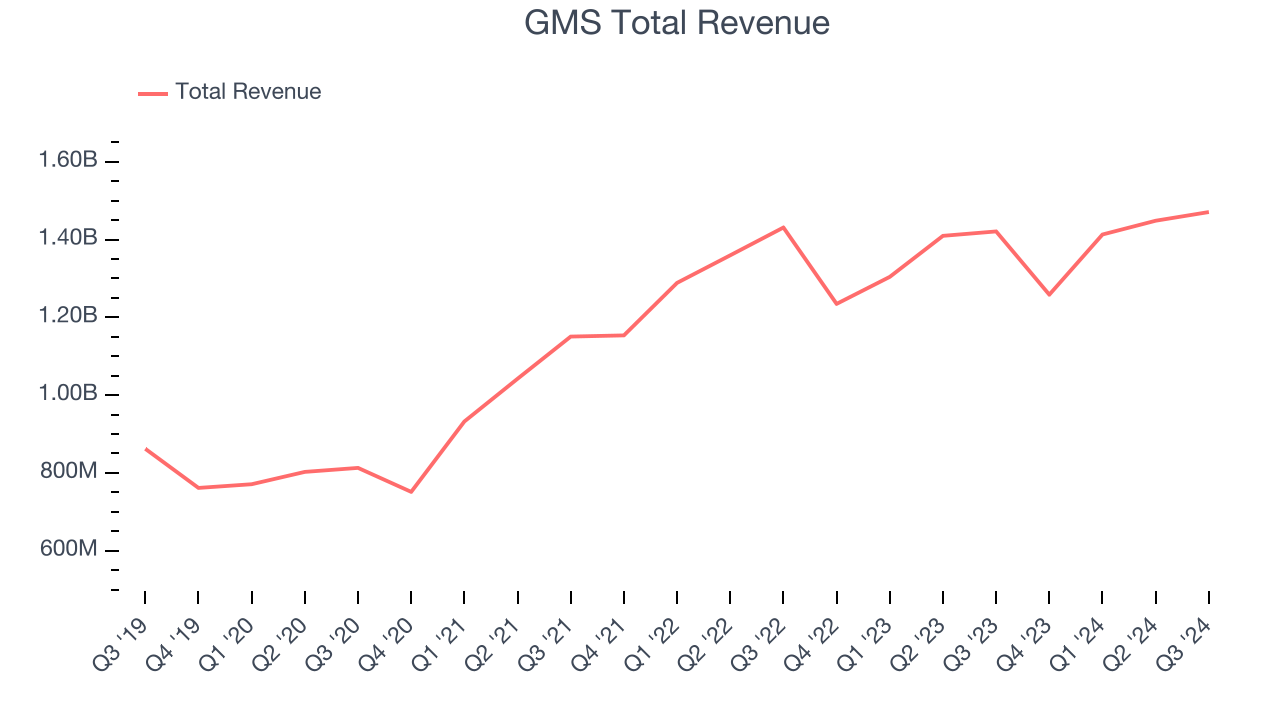

GMS (NYSE: GMS)

Founded in 1971, GMS (NYSE: GMS) distributes specialty building materials including wallboard, ceilings, and insulation products, to the construction industry.

GMS reported revenues of $1.47 billion, up 3.5% year on year. This print exceeded analysts’ expectations by 0.5%. Despite the top-line beat, it was still a slower quarter for the company with a significant miss of analysts’ EBITDA and EPS estimates.

“During our second quarter of fiscal 2025, the GMS team delivered net sales of $1.5 billion, net income of $53.5 million and Adjusted EBITDA of $152.2 million, reflecting the team’s continued ability to effectively navigate a challenging and dynamic operating environment,” said John C. Turner, Jr., President and CEO of GMS.

Unsurprisingly, the stock is down 3.9% since reporting and currently trades at $98.22.

Read our full report on GMS here, it’s free.

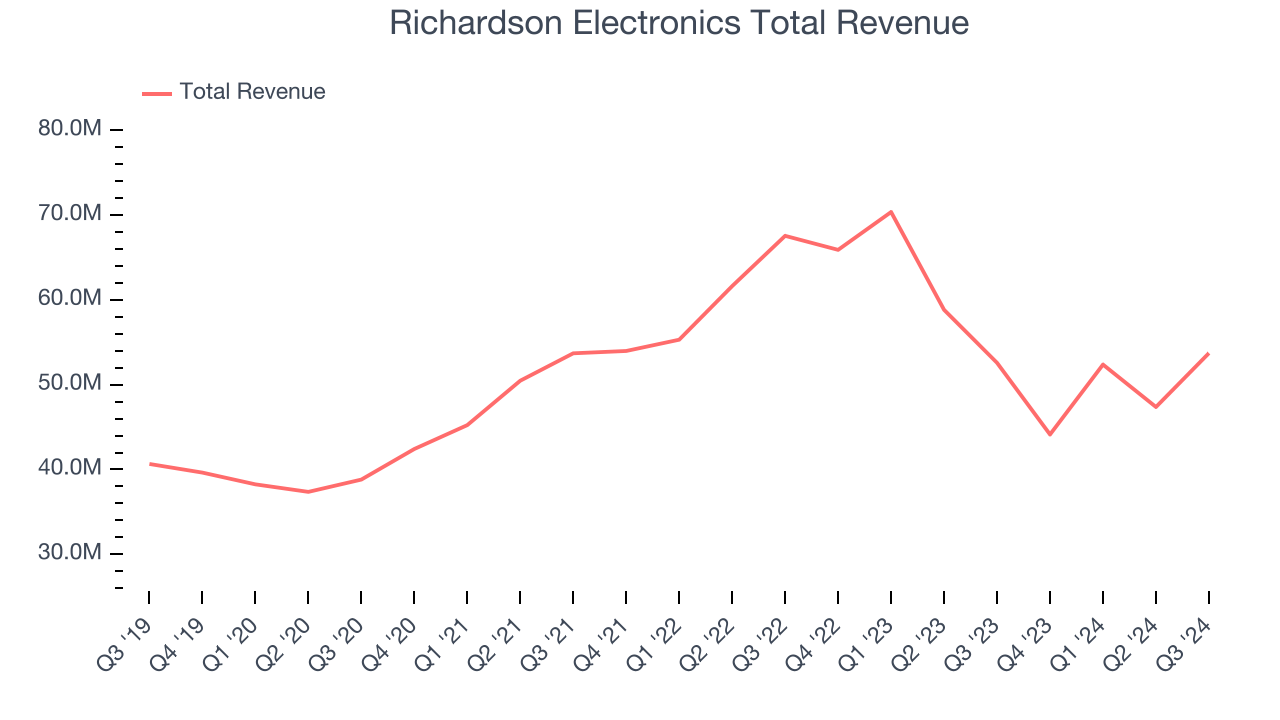

Best Q3: Richardson Electronics (NASDAQ: RELL)

Founded in 1947, Richardson Electronics (NASDAQ: RELL) is a distributor of power grid and microwave tubes as well as consumables related to those products.

Richardson Electronics reported revenues of $53.73 million, up 2.2% year on year, outperforming analysts’ expectations by 8.7%. The business had an incredible quarter with a solid beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 10.8% since reporting. It currently trades at $14.28.

Is now the time to buy Richardson Electronics? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Alta (NYSE: ALTG)

Founded in 1984, Alta Equipment Group (NYSE: ALTG) is a provider of industrial and construction equipment and services across the Midwest and Northeast United States.

Alta reported revenues of $448.8 million, down 3.7% year on year, falling short of analysts’ expectations by 6.5%. It was a disappointing quarter as it posted and a significant miss of analysts’ adjusted operating income estimates.

Alta delivered the weakest performance against analyst estimates in the group. The stock is flat since the results and currently trades at $8.02.

Read our full analysis of Alta’s results here.

Boise Cascade (NYSE: BCC)

Formed through the merger of two lumber companies, Boise Cascade Company (NYSE: BCC) manufactures and distributes wood products and other building materials.

Boise Cascade reported revenues of $1.71 billion, down 6.6% year on year. This number was in line with analysts’ expectations. More broadly, it was a mixed quarter as it also produced a narrow beat of analysts’ EBITDA estimates but a miss of analysts’ Building Material Distribution revenue estimates.

The stock is up 9.1% since reporting and currently trades at $146.20.

Read our full, actionable report on Boise Cascade here, it’s free.

FTAI Aviation (NASDAQ: FTAI)

With a focus on the CFM56 engine that powers Boeing and Airbus’s planes, FTAI Aviation (NASDAQ: FTAI) sells, leases, maintains, and repairs aircraft engines.

FTAI Aviation reported revenues of $465.8 million, up 60% year on year. This print topped analysts’ expectations by 10.8%. Overall, it was a very strong quarter as it also produced a solid beat of analysts’ EBITDA estimates and a decent beat of analysts’ EPS estimates.

FTAI Aviation delivered the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is up 3% since reporting and currently trades at $149.30.

Read our full, actionable report on FTAI Aviation here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September, a quarter in November) have kept 2024 stock markets frothy, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there's still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.