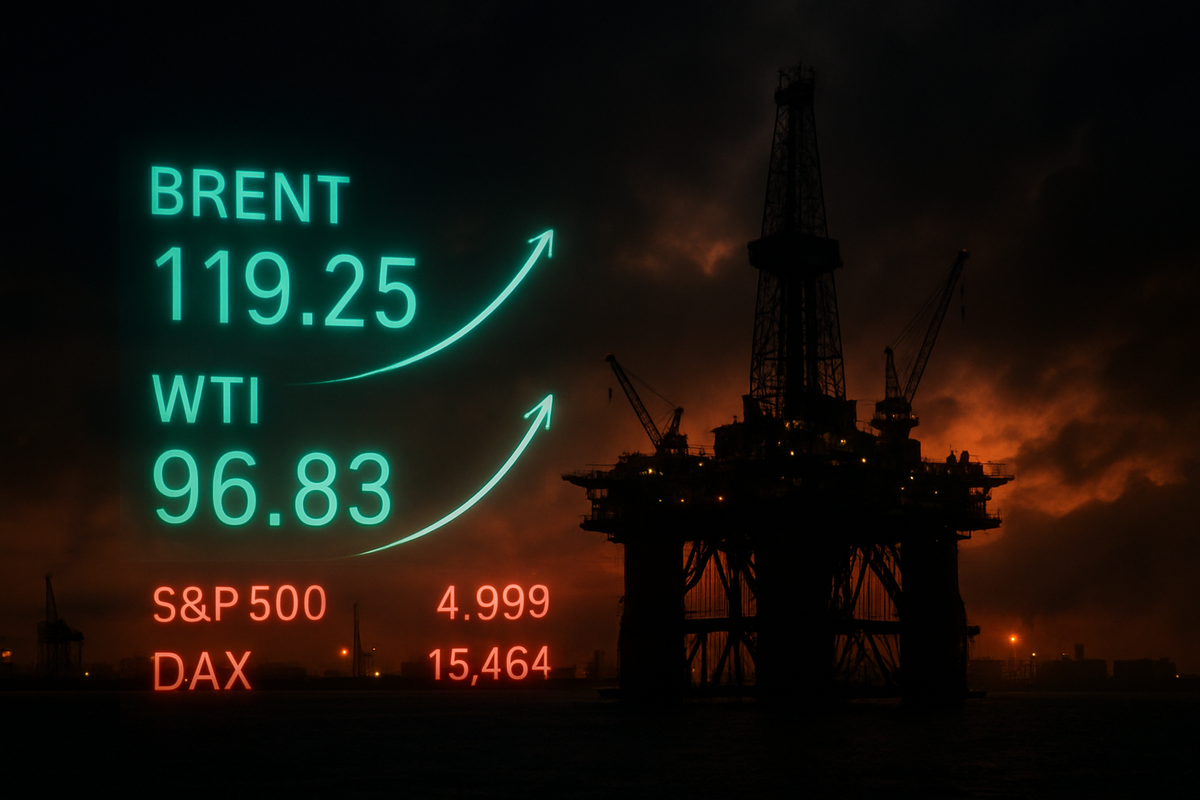

Global energy markets were thrust into a state of high-intensity volatility on March 19, 2026, as Brent crude surged briefly to $119 per barrel and West Texas Intermediate (WTI) climbed past the $96 mark. This dramatic price action follows a series of military escalations in the Middle East that have directly targeted critical oil and gas infrastructure in Iran and Qatar, sparking fears of a prolonged supply vacuum that could derail the global economic recovery.

The immediate implications are stark: the effective closure of the Strait of Hormuz and damage to Qatar’s primary liquefied natural gas (LNG) export facilities have removed a massive portion of the world’s energy supply overnight. As gas stations across Europe and North America report record-high prices and global stock indices experience a sharp "risk-off" rotation, the specter of "sticky" inflation has returned to haunt central banks, threatening to postpone long-awaited interest rate cuts.

A Targeted Campaign: Operation Epic Fury and the Retaliatory Strike

The current crisis traces back to early March 2026, with the launch of "Operation Epic Fury," a combined military campaign led by Israel with tactical support from Western allies. The operation initially targeted Iranian military command centers and suspected nuclear research facilities. However, by mid-March, the theater of war expanded significantly. While Kharg Island—the "beating heart" of Iranian oil exports handling over 90% of the nation's crude—remains physically intact but heavily blockaded, the Abadan Refinery and several Tehran-based processing plants were reported hit by precision strikes on March 15.

The situation escalated further on March 18 and 19, when Iran launched a massive retaliatory drone and missile swarm against Qatar’s Ras Laffan Industrial City. QatarEnergy, the state-owned giant, was forced to declare force majeure after reports confirmed extensive damage to several LNG "trains" and the Pearl Gas-to-Liquids (GTL) facility. This event alone has wiped out approximately 19% of the global LNG supply, sending the Dutch TTF benchmark soaring by 24% and causing a liquidity vacuum in the European heating and power sectors.

The timeline leading to this moment has been one of deteriorating diplomacy and "shadow war" tactics throughout late 2025. By the time the Strait of Hormuz was officially declared a high-risk zone on March 9, Brent crude had already breached $100. The market panic intensified this week as it became clear that alternative pipelines in Saudi Arabia and the UAE lack the capacity to compensate for the 20 million barrels per day (bpd) typically flowing through the Strait.

Initial market reactions have been characterized by a flight to safety and a surge in energy-linked commodities. Traders are currently pricing in a "war premium" that analysts at major investment banks suggest could keep Brent above $110 for the remainder of the quarter, provided the blockade of the Strait persists.

The Market Divide: Winners and Losers in the Energy Crisis

In the wake of the price surge, a clear divide has emerged between industries. The primary beneficiaries are global integrated oil majors and defense contractors. Exxon Mobil Corporation (NYSE: XOM) and Chevron Corporation (NYSE: CVX) have seen their shares rally as higher spot prices for crude and natural gas bolster their upstream earnings. Similarly, European giants like Shell plc (NYSE: SHEL) and BP p.l.c. (NYSE: BP) are benefiting from the LNG price spike, though their proximity to the European energy crisis adds a layer of complexity to their regional operations.

Defense stocks have also outperformed the broader market significantly. Lockheed Martin Corporation (NYSE: LMT), Northrop Grumman Corporation (NYSE: NOC), and RTX Corporation (NYSE: RTX) have seen increased demand as Western nations and Middle Eastern allies scramble to bolster missile defense systems and replace munitions used in "Operation Epic Fury." These companies are viewed as hedges against continued geopolitical instability, with many reporting record-high backlogs in their Q1 2026 preliminary updates.

Conversely, the "losers" of this energy shock are numerous and widespread. The airline industry has been hit hardest by the spike in jet fuel costs. Delta Air Lines, Inc. (NYSE: DAL) and United Airlines Holdings, Inc. (NASDAQ: UAL) saw their share prices tumble as investors factored in the massive hit to operating margins and the potential for a pullback in consumer travel demand. Furthermore, the automotive sector, including Ford Motor Company (NYSE: F) and General Motors Company (NYSE: GM), is facing renewed pressure as high gasoline prices dampen the enthusiasm for internal combustion engine vehicles, while the high cost of electricity in Europe slows the adoption of electric vehicles produced by Tesla, Inc. (NASDAQ: TSLA).

Retail and consumer discretionary sectors are also feeling the pinch. As household budgets are diverted to heating and transportation, large-cap retailers are seeing a slowdown in non-essential spending. The global stock markets reflect this pain; the S&P 500 fell to a 2026 low of 6,663 on March 9, and the German DAX has slipped below the 23,000-point threshold, signaling deep concern over a potential Eurozone recession.

Broader Significance: A Shift in the Global Energy Order

This conflict fits into a broader trend of "energy weaponization" that has defined the mid-2020s. The strikes on Qatari LNG infrastructure are particularly significant because they represent a shift away from traditional oil-centric warfare toward the targeting of the natural gas supply chain. This move directly undermines Europe's efforts to diversify away from Russian gas, proving that no energy source is truly immune to geopolitical risk.

The ripple effects extend to global trade partners, most notably China. As the primary buyer of Iranian "dark fleet" oil, China now faces a severe supply disruption that could stall its industrial output. This has led to speculation that Beijing may take a more active role in mediating the conflict, potentially exerting pressure on Tehran to reopen the Strait of Hormuz in exchange for security guarantees.

From a regulatory standpoint, the crisis is likely to trigger a massive release from the Strategic Petroleum Reserve (SPR) in the United States. However, with the SPR already at historically low levels following the drawdowns of 2022 and 2024, the efficacy of this move is being questioned. The precedent set by the 2022 energy crisis following the invasion of Ukraine suggests that while SPR releases can provide short-term relief, they cannot solve the structural deficit caused by the loss of 20% of global transit capacity.

Moreover, the events of March 2026 are forcing a re-evaluation of the global energy transition. While the surge in oil prices traditionally accelerates interest in renewables, the immediate need for energy security is driving a short-term resurgence in coal and nuclear power across the G7 nations. The "green vs. secure" debate has reached a fever pitch, with policy implications that could last for decades.

The Road Ahead: Potential Scenarios and Strategic Pivots

In the short term, the market is bracing for "Scenario A": a prolonged blockade of the Strait of Hormuz lasting into the summer of 2026. Under this scenario, Brent could feasibly test the $150 mark, and WTI could sustain prices well above $120. This would almost certainly trigger a global recession, characterized by "stagflation"—high inflation coupled with stagnant growth. Central banks would be forced into an impossible choice: raise rates to fight energy-led inflation or lower them to support a failing economy.

Alternatively, "Scenario B" involves a rapid de-escalation brokered by international intermediaries. If Qatar can repair its LNG trains within six months and the blockade is lifted, prices could retract as quickly as they rose. However, the physical damage to the Ras Laffan facility and the North Field expansion project—originally intended to raise Qatar's capacity to 126 million tons per annum by late 2026—means that the gas market will likely remain tight for years regardless of the diplomatic outcome.

Market participants will need to adapt by prioritizing "energy-efficient" portfolios and looking for opportunities in domestic North American energy production. Companies with high exposure to the Permian Basin or Canadian oil sands are likely to become the new "safe havens" for energy investors. We may also see a pivot toward intensified investment in hydrogen and advanced nuclear technologies as Western nations seek to insulate their power grids from Middle Eastern volatility once and for all.

Conclusion: A Turning Point for Investors

The surge in energy prices on March 19, 2026, marks a definitive turning point for the global markets. The "Operation Epic Fury" campaign and the subsequent strikes on Qatari and Iranian infrastructure have demonstrated that the world's energy pulse remains vulnerable to the ancient fault lines of Middle Eastern geopolitics. The jump in Brent to $119 is not just a number; it is a signal of a world realigning its priorities toward security and resilience.

Moving forward, the market is likely to remain in a high-volatility regime. Investors should watch for three key indicators: the status of the Strait of Hormuz, the speed of repairs at the Ras Laffan LNG facility, and the rhetoric from the U.S. Federal Reserve regarding "energy-driven" inflation. While the immediate outlook is clouded by the smoke of conflict, the long-term impact will be a permanent shift in how energy is valued, traded, and secured.

For the months ahead, the focus must remain on diversification and the monitoring of supply-side constraints. The events of this week have proven that in the 2026 economy, energy is the ultimate currency, and those who control the infrastructure control the market's destiny.

This content is intended for informational purposes only and is not financial advice