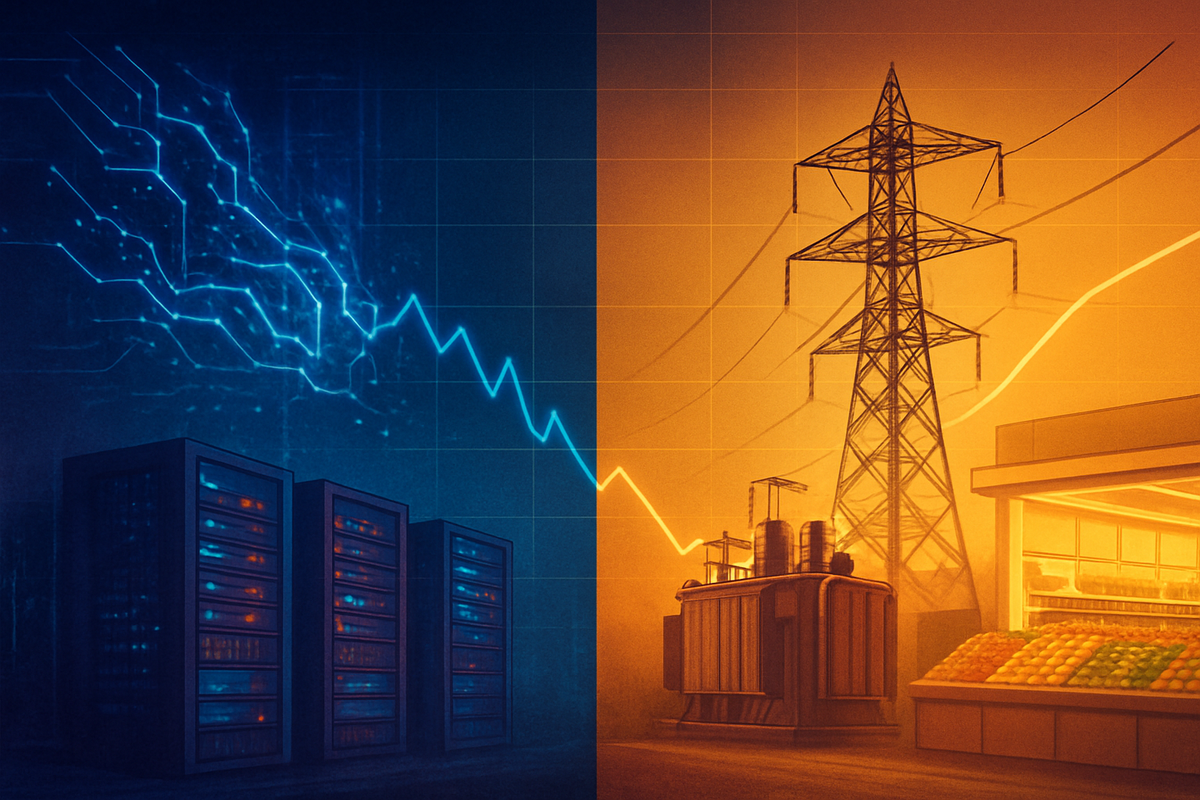

The high-octane artificial intelligence rally that defined the previous two years hit a significant roadblock in February 2026, as investors abruptly pivoted away from expensive growth stocks toward the stability of "old economy" sectors. While the tech-heavy Nasdaq reeled from a valuation reset, the Utilities Select Sector SPDR Fund (NYSE: XLU) recorded a steady 1.5% gain for the month, serving as a vital ballast for portfolios weathering the storm of AI-related uncertainty and rising infrastructure costs.

This rotation marks a dramatic shift in market leadership, signaling that the "AI at any price" era may be giving way to a more disciplined focus on cash flow and regulatory resilience. As software-as-a-service (SaaS) providers faced an existential threat from autonomous AI agents, the Consumer Staples Select Sector SPDR Fund (NYSE: XLP) also saw renewed interest, with investors seeking shelter in companies with predictable earnings and high dividend yields.

The "SaaS-pocalypse": A Month of Tech Turmoil

The catalyst for this defensive migration began in early February, when a series of advancements in autonomous coding and workflow automation triggered what traders have dubbed the "SaaS-pocalypse." On February 4 alone, the software sector lost nearly $300 billion in market value after updates from major AI labs suggested that traditional subscription software models could be rendered obsolete by AI agents capable of building and managing bespoke enterprise tools on the fly. This sparked a liquidity event that saw the iShares Expanded Tech-Software Sector ETF (BATS: IGV) plunge nearly 30% throughout the month.

The timeline of the sell-off was rapid. Following a disappointing earnings season where mega-cap tech firms reported "exploding capital expenditures" with diminishing marginal returns, institutional investors began offloading growth positions. By the second week of February, the narrative had shifted from AI optimism to "structural accountability." Concerns regarding the EU AI Act—set to become fully enforceable by August 2026—and new U.S. mandates on algorithmic safety created a regulatory friction that cooled the previous year's euphoria.

Initially, the Utilities sector faced a minor dip on February 2nd as Treasury yields spiked, but the narrative quickly flipped. As the Nasdaq fell 5% in a single week, capital flooded into XLU and XLP. By mid-month, Utilities had not only recovered but were outperforming the broader S&P 500 by a wide margin, as the market began to price in the sector's unique role as the "power provider" for the very AI data centers that were causing so much volatility elsewhere.

Winners in the Shadows and the Giants Under Pressure

The biggest losers of the February rotation were the former darlings of the AI boom. Microsoft Corp. (NASDAQ: MSFT) saw its market capitalization retreat by approximately $1 trillion since its late 2025 highs, as investors questioned its heavy reliance on partner models and its massive Azure infrastructure spend. IBM (NYSE: IBM) also faced its steepest monthly decline since 2000, dropping 27% following the launch of disruptive AI tools that automate legacy code modernization—a core part of Big Blue’s consulting business. Other high-growth names like Atlassian (NASDAQ: TEAM) and Intuit (NASDAQ: INTU) suffered one-day drops exceeding 30% as the market re-evaluated their subscription-based moats.

Conversely, the "safe haven" play breathed new life into traditional powerhouses. NextEra Energy (NYSE: NEE) and Duke Energy (NYSE: DUK) became standout performers, with Duke raising its five-year infrastructure spending plan to $103 billion to meet the insatiable electricity demands of generative AI. Vistra Corp. (NYSE: VST) also saw significant gains as it leveraged its nuclear and gas-fired capacity to secure long-term contracts with data center operators who are increasingly desperate for reliable, 24/7 power.

In the consumer space, the rotation was equally evident. Coca-Cola Co. (NYSE: KO) experienced a technical breakout as institutional inflows reached a two-year high, while retail giants Walmart Inc. (NYSE: WMT) and Costco Wholesale Corp. (NASDAQ: COST) were favored for their recession-resistant business models. These companies offered a stark contrast to the volatility of Alphabet Inc. (NASDAQ: GOOGL) and Amazon.com Inc. (NASDAQ: AMZN), both of which saw their margins squeezed by the soaring costs of HBM (High Bandwidth Memory) chips and the energy required to train next-generation models.

A Structural Shift: Why Defensive is the New Offensive

The February rotation is more than just a momentary dip in tech; it represents a broader recognition of the physical constraints of the AI revolution. For the past two years, the market focused on the "brain" of AI (the models), but in 2026, the focus has shifted to the "body" (the power and the hardware). The 1.5% gain in Utilities during a month of tech carnage highlights a historical precedent: when a new technology enters its "deployment phase," the infrastructure providers often become more stable investments than the early-stage innovators who are currently cannibalizing each other's software models.

Furthermore, the macro environment has played a crucial role. With inflation remaining sticky at 2.9% in January 2026, the Federal Reserve has signaled that rate cuts are not imminent. This hawkish tilt has fundamentally hurt the discounted cash flow valuations of high-growth tech, while making the 3% to 4% dividend yields found in Utilities and Staples increasingly attractive to income-starved investors. The "yield-plus-growth" profile of modern utilities, driven by data center demand, has effectively rebranded the sector from a sleepy bond proxy to a core AI-infrastructure play.

The ripple effects are also being felt in the regulatory sphere. The EU AI Act’s impending enforcement has forced companies to allocate billions toward compliance, a cost that defensive sectors like Utilities—already heavily regulated and accustomed to complex compliance frameworks—are much better positioned to handle. This has led to a "flight to quality" where quality is defined not by growth potential, but by regulatory certainty and balance sheet strength.

Looking Ahead: Is the Rotation a Temporary Hedge or a New Regime?

In the short term, the market is likely to remain bifurcated. We may see a "dead cat bounce" in software stocks as valuations reach levels not seen since the 2022 bear market, but the structural headwinds facing AI profitability remain. Analysts expect that the divergence between the "Power & Pipes" (Utilities) and the "Pixels & Programs" (SaaS) will continue until there is a clear roadmap for how AI software will generate sustainable enterprise value without being commoditized by open-source agents.

Strategically, investors are expected to maintain an overweight position in defensive sectors through the first half of 2026. The next major catalyst will be the Q1 earnings reports in April, which will reveal if the massive Capex spending from firms like Amazon and Alphabet is beginning to yield the promised productivity gains. If those gains fail to materialize, the rotation into XLU and XLP could accelerate, turning a monthly trend into a multi-year regime change.

Conclusion: The Market’s Search for Certainty

February 2026 will be remembered as the moment the AI narrative matured. The 1.5% gain in Utilities against a backdrop of tech instability underscores a simple truth: in a world of high uncertainty and "AI fatigue," investors value tangible assets and reliable dividends over speculative future earnings. The "safe havens" of Utilities and Consumer Staples have proven their worth once again, not just as defensive hedges, but as fundamental components of a modern, infrastructure-focused portfolio.

Moving forward, the market’s gaze will remain fixed on two variables: the cost of power and the cost of capital. For investors, the takeaway is clear: the AI boom is not over, but its beneficiaries have changed. Watching the performance of the XLU relative to the Nasdaq will be the primary signal for the remainder of the year. As we move into the spring, the question is no longer who can build the smartest AI, but who can keep the lights on while it runs.

This content is intended for informational purposes only and is not financial advice.