As of March 30, 2026, the technology sector finds itself at a critical crossroads, and no company embodies this tension more than Meta Platforms, Inc. (NASDAQ: META). After a period of breakneck growth fueled by the artificial intelligence (AI) gold rush of 2024 and 2025, the market has entered a significant correction phase. Meta, once the darling of the "Year of Efficiency," is now navigating a complex landscape defined by massive infrastructure spending, regulatory hurdles, and a landmark partnership with Entergy Corporation (NYSE: ETR) that signals a new era of "Energy-First" tech strategy. This article explores Meta’s transition from a social media titan to an industrial AI powerhouse and its resilience amidst a cooling tech market.

Historical Background

Meta’s journey from a Harvard dorm room to a global conglomerate is well-documented, but its recent history is perhaps more transformative. Following the 2021 rebrand from Facebook to Meta, the company weathered a "lost year" in 2022 as it over-invested in the Metaverse. However, the 2023 "Year of Efficiency" led by CEO Mark Zuckerberg pivoted the company toward fiscal discipline and AI integration. By 2024, Meta had reclaimed its position as a high-growth leader, utilizing its open-source Llama models to dominate the developer ecosystem. By early 2026, the company has completed its pivot into the "AI Factory" era, focusing less on social networking features and more on the physical and computational infrastructure required to power the next generation of digital intelligence.

Business Model

Meta’s business model remains anchored by its Family of Apps (FoA)—Facebook, Instagram, Messenger, and WhatsApp—which collectively serve over 4 billion monthly active users. Revenue is predominantly derived from highly targeted digital advertising, increasingly optimized by the company’s "Advantage+" AI suite.

However, a secondary model is emerging: AI Infrastructure and Compute. Through its massive investments in data centers and proprietary silicon (MTIA), Meta is positioning itself not just as a consumer app company, but as a foundational layer for AI. Its "Open Source AI" strategy serves to commoditize the models of its rivals while ensuring that Meta remains the most efficient platform for running those models at scale.

Stock Performance Overview

Over the last decade, META has been one of the market's most volatile yet rewarding performers.

- 10-Year View: The stock has seen a nearly 600% increase, surviving the 2022 "Metaverse Crash" to reach new all-time highs in late 2025.

- 5-Year View: Investors have seen a 180% return, largely driven by the AI pivot and the successful monetization of Instagram Reels.

- 1-Year View: The picture is more nuanced. After peaking at approximately $796 in August 2025, the stock has entered a 20-23% pullback as of March 2026. This correction mirrors a broader 10% drop in the Nasdaq Composite, as investors grapple with "CapEx fatigue" and rising interest rates.

Financial Performance

Meta’s financials in early 2026 reflect a "high-stakes reinvention."

- Revenue: For the full year 2025, Meta crossed the historic $200 billion mark, ending at $200.97 billion. Q4 2025 alone saw $59.89 billion in revenue, up 24% year-over-year.

- Margins: Operating margins have seen compression, dropping from 48% in 2024 to 41% in early 2026. This is a direct result of the astronomical depreciation costs associated with AI data centers.

- Capital Expenditure (CapEx): In a move that startled many analysts, Meta guided 2026 CapEx between $115 billion and $135 billion, nearly double its 2025 spend. This capital is being deployed into "Hyperion" class data centers and massive chip orders from NVIDIA (NASDAQ: NVDA) and Advanced Micro Devices (NASDAQ: AMD).

Leadership and Management

Mark Zuckerberg continues to exert absolute control over the company through his dual-class share structure. His leadership style has evolved into what insiders call "Lean and Lethal." In early 2026, Meta began utilizing internal AI agents to handle middle-management and project-tracking tasks, allowing for a 20% reduction in non-technical headcount without sacrificing output. Zuckerberg’s strategy is clear: he wants Meta to be the most "compute-per-employee" efficient company in the world.

Products, Services, and Innovations

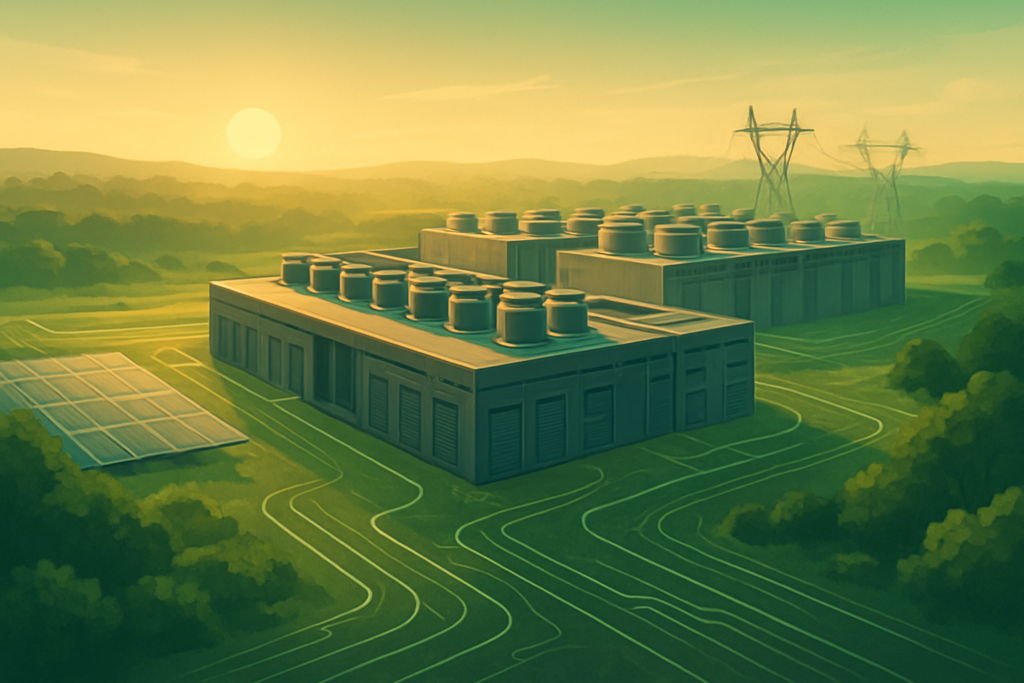

The crown jewel of Meta’s 2026 roadmap is the Hyperion Data Center in Richland Parish, Louisiana. This facility is the centerpiece of the Entergy partnership and is designed to house hundreds of thousands of next-gen GPUs.

- Llama & "Avocado": While the Llama 4 series was a success, Meta faced a setback in early 2026 with the delay of its next-gen "Avocado" model, intended to provide "Personal Superintelligence." The delay to May 2026 contributed to the recent stock pullback.

- Hardware: Reality Labs, though still loss-making, has found a niche with the "Orion" AR glasses, which began shipping in limited quantities in late 2025.

Competitive Landscape

Meta competes on two fronts:

- Attention: Against ByteDance (TikTok) and Alphabet (NASDAQ: GOOGL). In this arena, Meta has gained ground, with Instagram Reels watch time surging 30% thanks to AI-driven recommendation engines.

- Intelligence: Against Microsoft (NASDAQ: MSFT) and OpenAI. Meta’s strategy of open-sourcing its models has put pressure on the proprietary "closed" models of its rivals, forcing a price war in AI tokens that Meta is well-positioned to win due to its lower cost of compute.

Industry and Market Trends

The dominant trend of 2026 is the "Energy Era" of Big Tech. Electricity, not just silicon, has become the primary constraint for AI growth. This has led to a vertical integration strategy where tech companies act more like utilities. Meta’s move to fund its own power plants through Entergy reflects a industry-wide pivot toward securing 24/7 carbon-free power, including small modular reactors (SMRs) and massive solar arrays.

Risks and Challenges

Meta faces significant headwinds that have fueled the 2026 correction:

- Regulatory Verdicts: In March 2026, a major court ruling held Meta liable for social media addiction in minors. This has led to fears of a structural overhaul of its advertising algorithms and multi-billion dollar payouts.

- Model Performance: The delay of the "Avocado" model has raised questions about whether Meta can keep pace with Google and OpenAI in the foundational model race.

- Macro Pressures: Persistent high interest rates and global trade tensions have made Meta’s $115B+ CapEx plan a "show-me" story for skeptical investors.

Opportunities and Catalysts

The Entergy Partnership is a significant catalyst. By funding 7.5 gigawatts (GW) of power—including seven natural gas plants and 2.5 GW of solar—Meta is effectively bypassing the strained public grid.

- Ratepayer Protection: The "Fair Share Plus" pledge helps insulate Meta from public backlash by delivering $2 billion in savings to local Louisiana residents, creating a blueprint for how Big Tech can expand without alienating local communities.

- Reels Monetization: The continued growth of Reels ads remains a massive tailwind, with AI-generated creative tools lowering the barrier for small business advertisers.

Investor Sentiment and Analyst Coverage

Wall Street remains cautiously bullish on META, maintaining a "Strong Buy" consensus despite price target trims. Firms like Morgan Stanley and Wedbush have lowered targets from $900 to $775, reflecting a more conservative valuation multiple in a high-rate environment. Institutional investors are watching Meta’s "Compute Moat" closely; the belief is that once the current CapEx cycle peaks, Meta will emerge with an unassailable advantage in AI delivery costs.

Regulatory, Policy, and Geopolitical Factors

The geopolitical landscape of 2026 is dominated by the "AI Arms Race." Meta’s open-source strategy is viewed as a strategic asset by the U.S. government, helping to export American AI standards globally. However, domestic policy remains a challenge. New privacy laws and the recent minor safety ruling represent a shift toward more aggressive oversight of data-driven business models. Furthermore, Meta’s reliance on Entergy's natural gas plants has drawn scrutiny from environmental groups, forcing the company to accelerate its nuclear and solar commitments.

Conclusion

Meta Platforms enters the second quarter of 2026 as a company in the midst of a radical metamorphosis. The partnership with Entergy highlights a future where Meta is as much an energy and infrastructure company as it is a social network. While the current tech correction has erased some of its 2025 gains, the company’s "Lean and Lethal" strategy and its massive investment in AI "Factories" suggest a long-term vision that few competitors can match. Investors should watch the May 2026 launch of the "Avocado" model and the progress of the Richland Parish data center as key indicators of whether Meta’s high-stakes bet will pay off.

This content is intended for informational purposes only and is not financial advice.