Palo Alto Networks (PANW) has built its name as a heavyweight in cybersecurity, sitting at the frontline of protecting enterprises as digital threats evolve, and now, as artificial intelligence (AI) systems grow more autonomous, the stakes around governance and security are rising just as fast. Autonomous AI agents are not just tools anymore, but they are decision-makers, operating across systems, which makes visibility, control, and real-time protection absolutely critical.

Therefore, Palo Alto Networks’ latest move begins to make sense. The company has announced plans to acquire Portkey, a startup focused on building an AI gateway that acts like a centralized command center for managing and securing AI agent traffic. Portkey’s technology is designed to process large-scale AI workloads with low latency while giving enterprises tighter control over how these agents operate.

The plan is to integrate this into Palo Alto’s Prisma AIRS platform, allowing businesses to monitor, route, and secure AI-driven transactions with stronger governance, identity controls, and runtime threat prevention.

With the deal expected to close by fiscal Q4 2026, Palo Alto Networks is showing investors that this goes beyond a routine acquisition. It reflects a deliberate push into the emerging AI agent security space, one that could influence the way in which the market assesses PANW’s future growth trajectory and long-term valuation.

About Palo Alto Stock

Palo Alto Networks is one of those companies working quietly in the background, keeping the digital world from falling apart. Based in Santa Clara, California, the company has evolved into a leading force in global cybersecurity, with a market capitalization of about $150.13 billion.

The company now delivers an integrated platform that secures networks, cloud environments, and enterprise data through AI-led threat detection and real-time protection. Its ecosystem, supported by Unit 42 intelligence, serves a vast global customer base. By combining multiple security layers into a unified framework and advancing Zero Trust principles, Palo Alto continues to align its innovation with the growing complexity of modern digital infrastructure.

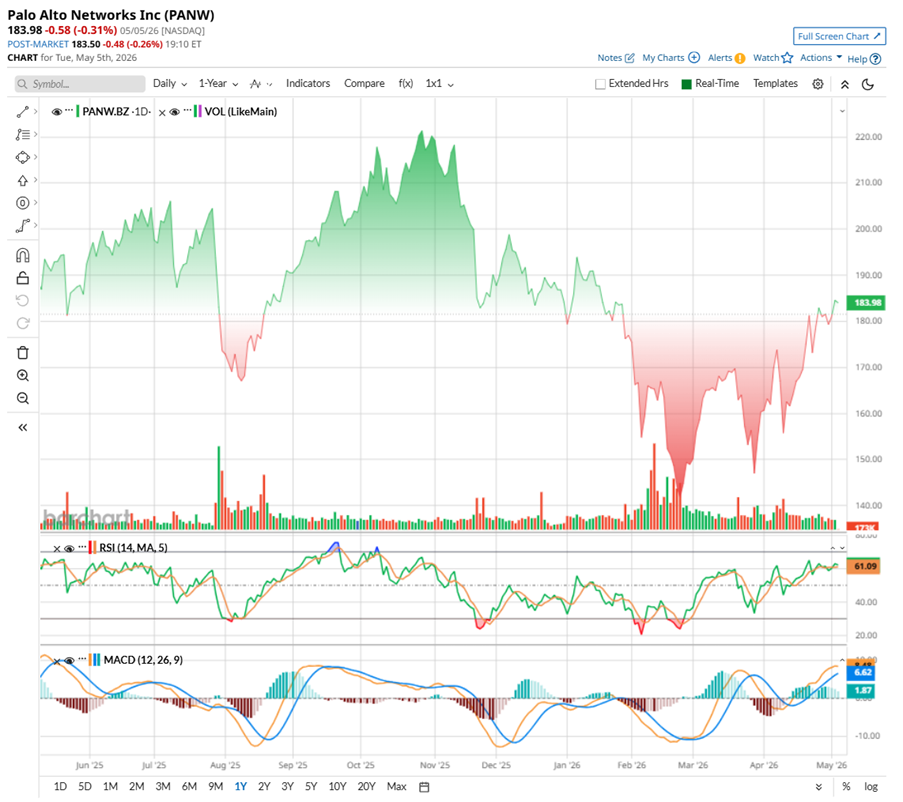

The recent journey of Palo Alto stock has reflected a market caught between optimism and caution. After touching a 52-week high of $223.61 in October, the stock saw a sharp pullback of nearly 17.7%, slipping to $139.57 in late February as sentiment around AI-driven disruption turned more measured.

Since then, the recovery has been notable. The stock has rebounded to 31% from those lows, although on a broader view, it remains slightly down by 2.49% over the past year and marginally negative year-to-date (YTD).

Yet, a closer look at recent price action suggests momentum is quietly rebuilding for PANW stock. Over the past three months, it has climbed 15.48%, with gains of 13.61% over the past month, and a modest 1.35% gain over the past five days.

Technically, the indicators are beginning to align with this recovery. The 14-day RSI has moved back to 62.17, signaling improving strength without entering overbought territory. Plus, the MACD oscillator is flashing bullishness, with the MACD line moving above the signal line and the histogram printing positive bars.

This combination typically reflects strengthening momentum and suggests that the recent recovery may have more room to run in the near term, provided broader market sentiment remains supportive.

Valuation-wise, PANW carries a premium price tag, trading at 49.84 times forward adjusted earnings and 13.21 times forward sales, higher than sector averages. This reflects solid investor confidence driven by consistent growth and ongoing acquisitions, but also leaves limited room for error if execution or growth momentum begins to slow.

A Snapshot of Palo Alto Networks’ Q2 Numbers

Palo Alto Networks released its fiscal second-quarter results on Feb. 17, and the numbers show a company steadily delivering today while building for something bigger ahead. Revenue rose 15% year-over-year (YOY) to $2.6 billion, ahead of expectations, and a large part of this growth was driven by its subscription and services segment, which continues to anchor its platform-focused strategy.

Profitability also looked solid. Non-GAAP operating margins improved to 30.3% from 28.4% a year ago, while non-GAAP EPS surged over 27% annually to $1.03, comfortably beating the Street’s estimates.

Its next-generation security ARR climbed 33% to $6.3 billion, and remaining performance obligations increased 23% to $16 billion, both pointing to a strong pipeline of future revenue. Financially, the company remains on firm ground, with $4.54 billion in cash and investments as of Jan. 31, 2026 and $3.75 billion in adjusted free cash flow.

Alongside this, Palo Alto is investing aggressively, expanding into identity security with its Cyberark acquisition and planning to acquire Koi, as it positions itself for a future shaped by AI-driven security risks.

Looking ahead, the management sounds quite confident about the future direction of PANW. For Q3, revenue is anticipated to land between $2.941 billion and $2.945 billion, which points to a solid 28% to 29% annual growth. Non-GAAP EPS is expected to come in between $0.78 and $0.80. One of the standout areas continues to be its next-gen security business, with ARR for the quarter projected at roughly $7.94 billion to $7.96 billion, up a sharp 56% YOY.

For fiscal 2026, the growth story stays strong as next-gen security ARR is expected to cross $8.5 billion, growing at over 50% annually. Total revenue is projected to be between $11.28 billion and $11.31 billion, while RPO is seen climbing past $20 billion.

Even so, there’s a bit of a trade-off here. All this aggressive growth and expansion is coming with higher costs, and that’s showing up in the bottom line. The company has trimmed its full-year EPS outlook slightly, now expecting it to be in the $3.65 to $3.70 range.

The company is expected to release its Q3 report on Tuesday, June 2, after the market closes.

Analysts tracking the company project its EPS to be around $0.43 in Q3, while revenue is expected to be $2.94 billion. For fiscal 2026, analysts expect EPS around $2.14, up 30.5% YOY, and then rise by another 6.1% annually to $2.27 in fiscal 2027.

What Do Analysts Expect for Palo Alto Networks Stock?

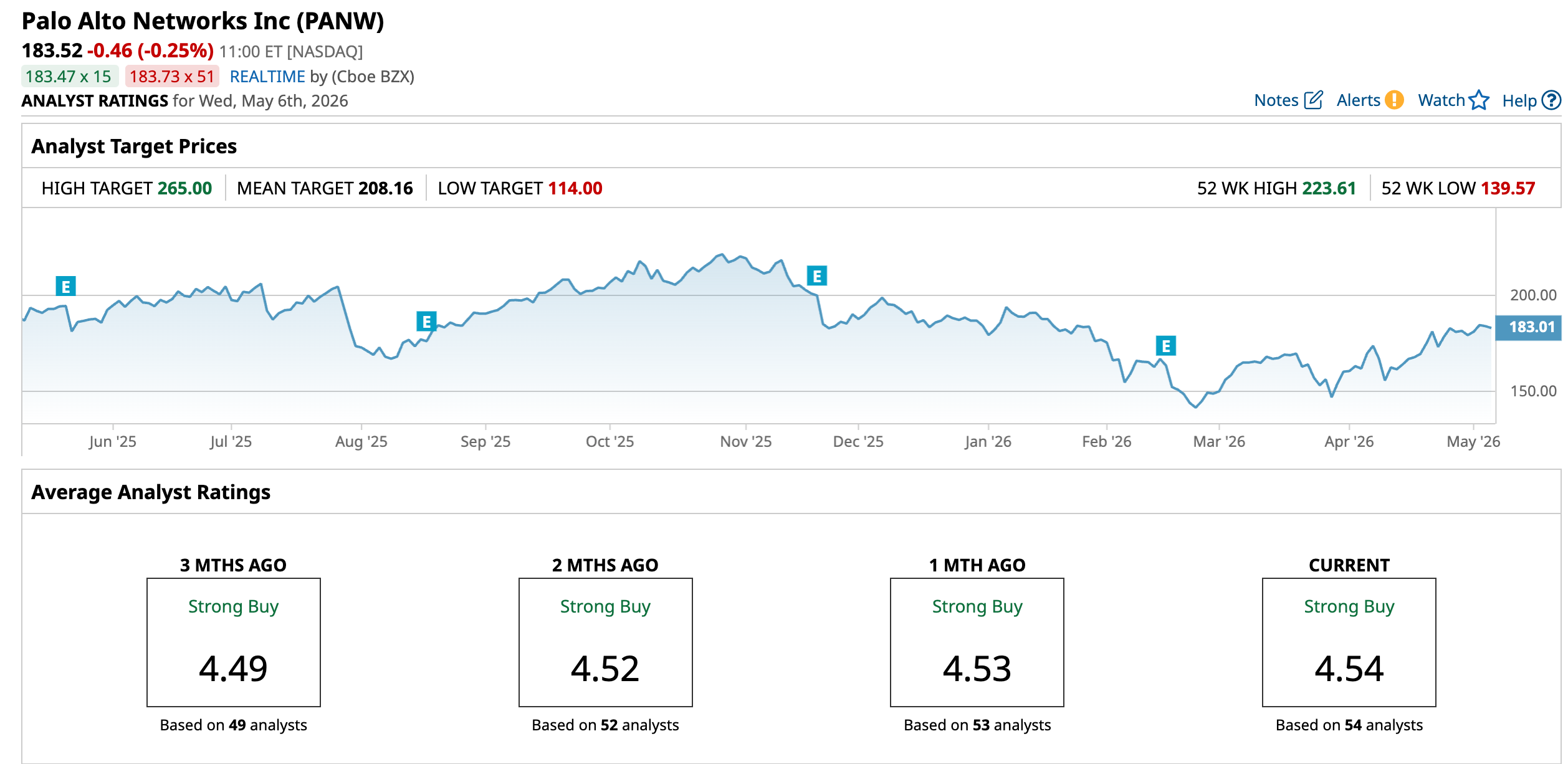

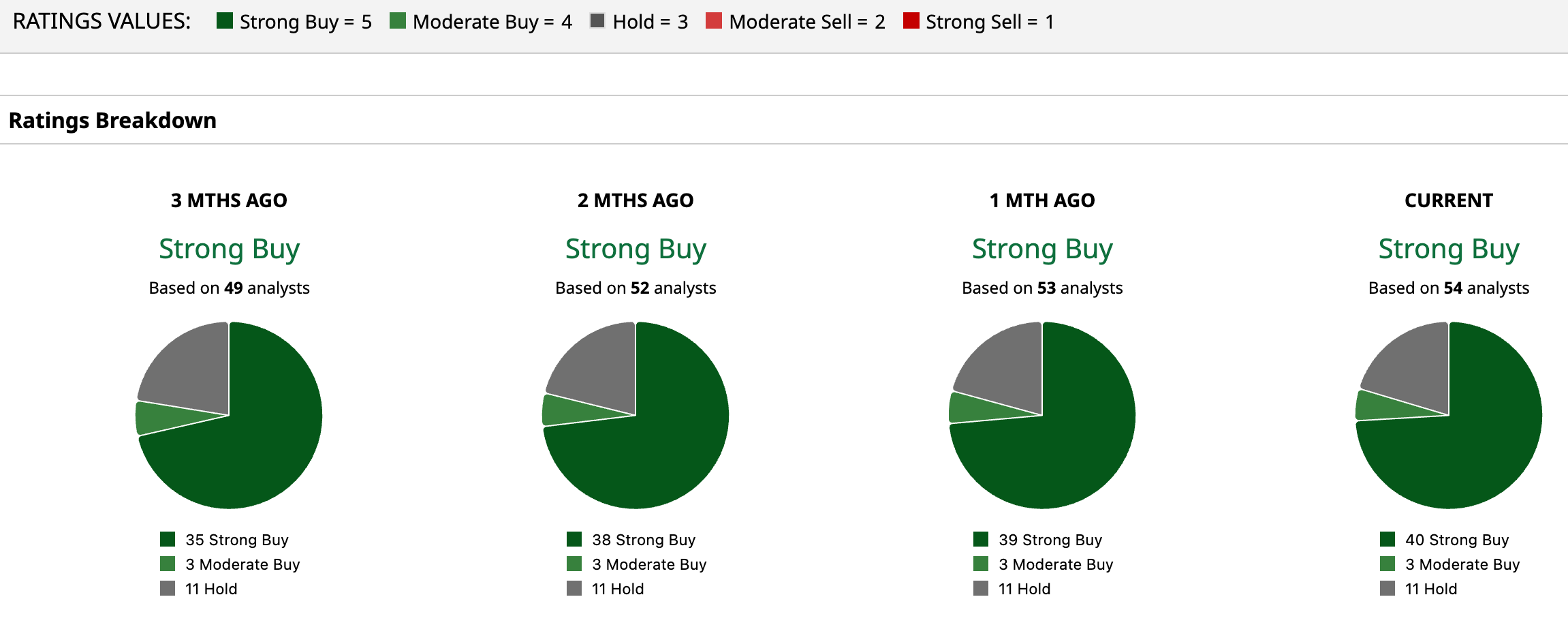

Overall, sentiment on PANW remains firmly bullish, with the stock’s consensus rating at “Strong Buy.” Out of 54 analysts, 40 recommend a “Strong Buy,” three have a “Moderate Buy,” and the remaining 11 are giving it a “Hold” rating.

Its average price target of $208.16 implies upside potential of 13.43%. Meanwhile, the Street-high target of $265 suggests PANW stock could rise as much as 44.4% from the current price levels.

Final Thoughts on PANW Stock

As the AI stack becomes more layered, Palo Alto Networks is positioning itself to own a larger slice of the security spend. The Portkey deal strengthens its foothold in AI agent security, a space that could unlock new growth and support premium valuations if adoption scales.

But the story is not without friction. Investors are still weighing execution risks, especially with multiple integrations underway, including CyberArk. The broader “platformization” push could drive durable growth, yet it also adds complexity and cost pressures.

So while the AI security opportunity looks real, the stock may hinge less on vision and more on delivery, making this both an exciting and carefully watched bet.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- With Earnings Ahead, Wait for a Dip Before You Buy CoreWeave Stock

- Sandisk Stock Is up Nearly 500% in 2026. Q3 Results Show Its Data Center Business Is Still Growing.

- The Biggest Catalyst for OKLO Stock May Not Be Earnings, But a Brewing Short Squeeze

- 7 Stocks Worth Buying the Dip in Now... Or At Least Adding to Your Watchlist